Economy 2026: What Slower Inflation and Modest Growth Mean for Fleets

The forces that disrupted growth in 2025 are beginning to settle. Entering 2026, fleets should expect gradual improvement, not a return to pre-volatility conditions.

by By Stephen Latin-Kasper

January 22, 2026

After a volatile 2025, the U.S. economy is expected to stabilize in 2026 with modest GDP growth, slowing but persistent inflation, cautious consumer spending, a tight labor market, and a gradual recovery in business investment.

Image: Automotive Fleet

5 min to read

Stephen Latin-Kasper, economist & CEO of Coherent Market Planning and Forecasting, sets the stage for the U.S. economy in 2026 and its implications for fleets.

The U.S. economy is likely to perform slightly better in 2026 than it did in 2025. To explain why, a summary of economic conditions in 2025 will be helpful.

2025: How Tariff, Inflation Expectations Swung GDP

GDP growth was slightly negative in the first quarter of 2025 due to expectations of rising prices following the imposition of import tariffs. Inflation was already higher than desired, and businesses pulled forward demand to the extent they could to avoid even higher input prices.

Because imports are counted as negative in the calculation of GDP, the massive increase in imports caused first-quarter GDP to decline 0.6%. Personal consumption expenditures (PCE) rose just 0.6% as consumers adopted a wait-and-see attitude.

Imports fell almost as much in the second quarter as they rose in the first. In addition, consumers reacted to tariff announcements by pulling their demand forward. PCE grew 2.5%, which contributed to a 3.8% GDP increase.

In the third quarter, imports fell again, exports rose significantly, and consumers pulled demand forward again in response to headlines indicating that inflation was trending up. PCE grew 3.5% as debt levels rose and savings, as a percentage of income, fell.

Fourth-quarter data won’t be released until the end of January (assuming there isn’t another government shutdown), but most consensus forecasts predict slow growth of about 1%.

Some economists are predicting a slight decline in fourth-quarter GDP; the primary reason is the likelihood that consumer spending growth slowed in response to rising prices and debt levels.

Outlook for 2026: Mild GDP Growth, Slowing Inflation

Imports will likely be a factor as well, since businesses have mostly adjusted to higher tariffs and need to restock their inventories. To be clear, their adjustment to higher tariffs was primarily achieved by raising product prices, which contributed to the acceleration of inflation in the third quarter.

A further, possibly final, price adjustment could occur in January because, while tariffs are expected to stabilize in 2026, in our current political environment, we can’t be certain about that.

Despite the volatility of the past year, forecasts for 2026 are pretty consistent. Consensus panels and investment banks' econometric models mostly project growth of about 2%.

The cautiously optimistic forecast leans heavily on the expectation that PCE growth will continue growing slowly and might even accelerate a bit. The primary factors driving the expectation are income rising faster than inflation and many state/local governments (about half of them) implementing minimum wage increases in 2026.

Minimum wage has been $7.25 for more than 16 years. That is the longest period since WWII that Congress hasn’t increased it.

The rate of inflation will likely slow in 2026, but not enough to reach the Federal Reserve’s 2% target by year-end. The unemployment rate is likely to peak below 5%, indicating we will remain near full employment in 2026.

That said, the labor market remains too tight, posing a risk to growth in 2026. The current immigration policy had a negative impact on food production and construction activity in 2025, contributing to inflation, and this could get worse in 2026.

If it gets bad enough to bankrupt farms and significantly limit the supply of new homes and commercial structures, there will be additional upward pressure on inflation, which could reintroduce pressure on interest rates.

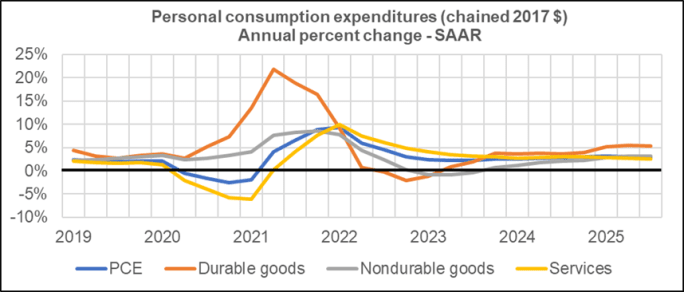

Personal consumption expenditures fluctuated sharply in the pandemic years, but spending patterns suggest a shift toward slower, more stable growth heading into 2026.

Graph: Stephen Latin-Kasper

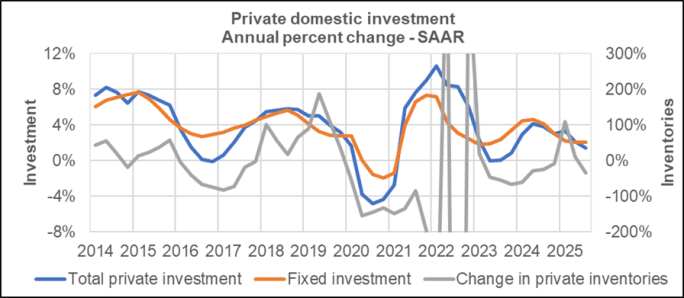

PDI: Wild Swings and AI Data Centers

Figure 2 shows the connection between the two components of private domestic (business) investment (PDI), one of which is change in private inventories (CIPI). The axis for CIPI is truncated because supply chain issues from the second half of 2021 through the first half of 2023 caused wild quarter-to-quarter swings.

The graph shows clearly that after increasing equipment expenditures by 21.4% in the first quarter to avoid tariffs, businesses cut back sharply on capital expenditures while waiting for trade policy to stabilize.

The one market segment that continued to attract capital was artificial intelligence, in the form of data centers and software. In total, on a quarter-to-quarter basis, PDI fell from 23.3% growth in the first quarter to -0.3% in the third, although, as shown in the graph, PDI continued to grow on an annual percent change basis in the third quarter.

CIPI fell almost 2,700% in third-quarter 2022. That was sandwiched between quarterly increases of about 600%. Thankfully, the recent decline in CIPI growth was relatively normal. As of the fourth quarter, CIPI is probably too low. What that means is that investment expenditures are likely to increase in 2026 along with PCE, which means GDP growth will likely accelerate, and that is why most forecasts for 2026 call for growth of about 2%.

Volatility in private domestic investment, driven largely by swings in inventories, moderated by 2024–2025 as fixed investment stabilized, pointing to more predictable capital spending conditions heading into 2026.

Graph: Stephen Latin-Kasper

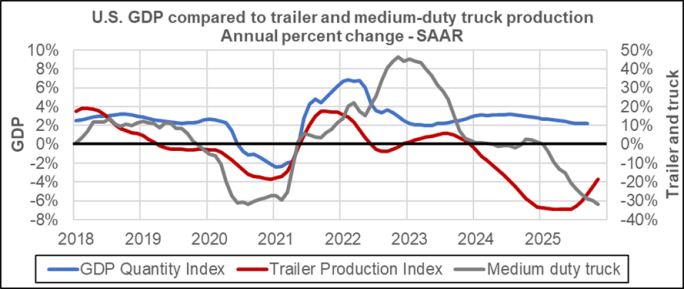

GDP and Commercial Trailer and Truck Markets

Commercial trailer and truck production have historically moved in the same general direction as GDP over the course of an economic cycle. In this cycle, trailer production in particular suggests that GDP growth is at or near a trough, rather than entering a period of contraction.

Interest rates support that interpretation. The relationship between trailer production and the prime rate indicates that the current cycle is still in its early recovery phase, with the next cyclical peak unlikely to occur before late 2026 or early 2027. The same pattern generally applies to commercial truck production, especially in the heavy-duty segment.

Commercial trailer and medium-duty truck production often move in the same direction as GDP over an economic cycle. In the current cycle, trailer production suggests GDP growth is near a trough rather than entering contraction.

Graph: Stephen Latin-Kasper

2026 Levers: Freight Growth and Interest Rates

The primary factors influencing trailer and truck production in 2026 are freight growth and interest rates. Freight tonnage has been flat to slightly declining since late 2023, reducing the need for fleet expansion and extending replacement cycles.

With interest rates leveling off but remaining elevated, expectations are for production growth in 2026 to taper and remain roughly in line with 2025 levels. More meaningful improvement in trailer and tractor production is not expected until 2027.

Subscribe to Our Newsletter

More State of the Fleet Industry

‘Mike Just Gives Cars to People’ — And Other Misconceptions Fleet Managers Need to Fix

Most organizations misunderstand fleet. The best managers make sure that doesn’t happen.

Read More →Sponsored•May 29, 2026

Are You Tracking Your Fleet's True Total Cost of Ownership?

Bobit Business Media surveyed 190 fleet professionals and found that while most fleets are tracking costs, fragmented systems and data gaps are keeping true TCO visibility out of reach. With rising pressure to control spend in an increasingly volatile environment, the gap between what fleets think they know and what the data actually shows is wider than you might expect. See how your peers are managing costs today and where the industry still has room to improve.

Read More →

Why Union Leasing Rebranded to Moventum Fleet Management

Mark Hogland discusses Union Leasing’s transition to Moventum Fleet Management and how the rebrand reflects the company’s growing focus on strategic fleet management and lifecycle support.

Read More →

Sponsored•May 13, 2026

Why Fleet Managers Are Replacing Departmental Vehicles with Shared Motor Pools

Departmentally assigned vehicles often create hidden costs through underutilization, poor visibility, and increased administrative burden. This white paper explores how shared motor pool strategies help fleets reduce costs, improve accountability, and optimize vehicle utilization.

Read More →

From Storm Response to Data Strategy: Fleet Trends to Watch | AF News Recap

In this AF news recap, host Faith Howell covers this week's most pressing industry updates.

Read More →

Report: 36% of Fleet Managers Are Delaying Replacements

Element’s 2026 Market Pulse Report finds fleets are slowing replacement cycles amid tariffs, economic uncertainty, and rising costs.

Read More →

California Adopts Sweeping New Autonomous Vehicle Regulations

Updated DMV rules open the door for heavy-duty AV testing and deployment while strengthening safety standards, emergency response coordination, and manufacturer accountability.

Read More →

Sponsored•May 6, 2026

Fleet Costs Are Rising: Here’s How Leaders Are Responding

Fleet leaders are under pressure to reduce costs, adapt to economic uncertainty, and make smarter decisions. See how peers across North America are responding with real data, proven strategies, and forward-looking insights. Download the 2026 Market Pulse Report to benchmark your strategy and uncover where you can gain an edge.

Read More →

Stellantis Taps Hyundai Exec to Lead U.S. Sales

Effective April 22, Jeep maker Stellantis has named Michael Orange as vice president of U.S Sales.

Read More →