Related: The State of Remarketing in 2019

Used SUVs Reached Saturation Point in 2019

CUV/SUVs saw year-over-year declines to their wholesale values, but are still performing well due to continued demand for these segments and cheap gas prices, but an inflection point is approaching.

December 13, 2019

The strength of the used market in 2019 was fueled by multiple factors but one key factor was the waning new car market.

Photo via istockphoto.com/smodj

10 min to read

Depreciation rates through the 2019 calendar-year followed a mostly typical pattern, which was a departure from the year of abnormally strong values in 2018.

Several remarketing managers from companies such as ARI, Donlen, Emkay, Enterprise Fleet Management, Merchants Fleet, and Wheels Inc. described the resale market in 2019 as mostly healthy.

Brian Garner, manager, ARI Remarketing Solutions, described the resale market in 2019 as healthy, but with a slight caveat. Depreciation trends mostly followed typical patterns but on a flatter plane. This meant that the highs that came with the spring tax season were not as high and the lows that came at the end of the year were not as low as they have been in past years.

Highs and lows came when they were expected, for the most part, but not as severely.

Jeff Krogen, assistant vice president of fleet strategy for Enterprise Fleet Management, agreed that 2019 offered a healthy resale market especially for commercial lease returns.

The strength of the used market in 2019 was fueled by multiple factors but one that Krogen highlighted was the waning new car market.

While record-high new-car prices have led to weaker retail demand on the new-vehicle side, commercial demand has continued to hold strong, which has helped drive resale values for work trucks and cargo vans that are 4 to 5 years old.

How Popular Fleet Segments Performed

Photo by Eric Gandarilla.

Light-duty pickups and vans have historically performed well in the used market due to their wide application in the fleet markets.

Garner said that this trend remained true in 2019.

John Wuich, vice president strategic consulting services at Donlen, saw solid performance from pickups and vans relative to the overall market, but also noticed a slight uptick among the segments in his portfolio.

A vehicle segment where Wuich has noticed a larger uptick in depreciation is the SUV/crossover segment.

The SUV/crossover segment has seen increased demand from fleets in recent years, as OEMs have been releasing model after model of vehicles in this segment.

As crossovers/SUVs that were sold in the past three years begin to return to the used market, the wholesale market is beginning to face an issue of oversupply.

“[We’re] watching the SUV and crossover market,” said Wuich. “This segment has greatly increased in new-vehicle popularity, and it is possible that this market may become flooded on the used vehicle side.”

Garner said that he and his team saw a similar trend.

“There’s a saturation especially among full-size SUVs and crossovers. The market has just become so overwhelmed with the number of brands that offer a vehicle in this segment,” said Garner.

Garner saw greater declines in mid-size and full-size SUV and crossover resale values in 2019, those declines existed in 2018 but they were less severe than they were this year.

And, this oversupply of SUVs and crossovers isn’t exclusive to mid-size and full-size models. Manufacturers have been releasing new entries into the compact crossover/SUV segment and that is beginning to have its own adverse effect on the wholesale market.

Wuich said that he noticed a greater demand for smaller SUV/crossovers in 2019. As more remarketers sell these small SUV/crossovers — which command lower prices than their larger counterparts — the overall average for the segment begins to drop.

Still, even with these year-over-year declines SUVs/crossovers are still performing well due to continued demand for these segments and cheap gas prices, but an inflection point is approaching.

Similarly, compact and mid-size cars are reaching their own inflection points, but on a more positive side of the spectrum.

“I think what you’re finding is kind of a supply and demand equation that’s making some of the small and mid-size cars actually perk up for the first time in a while, simply because there’s just not enough of them on the marketplace to fill the demand,” said ARI’s Garner.

Overall Donlen resale/residual values were essentially flat, with a depreciation rate of .20% year-over-year due to a slight increase in depreciation across all segments except for compact and intermediate cars. Compact car depreciation was down slightly, and intermediate cars saw no change in value year-over-year.

Wuich also noted that a smaller supply of compact sedan segments in the used market resulted in a stronger than expected performance in 2019. The lower average price of compact cars also helped bump up sales volume for the segment.

Fleet buyers’ interest in purchasing vehicles that will soon be phased out by manufacturers and a fewer supply of those vehicles in the market was another beneficial factor, he noted.

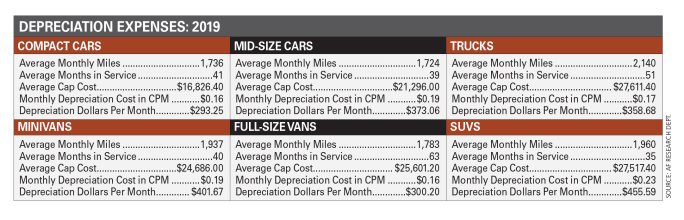

Analyzing FMC Remarketing Data

Full-size vans saw the biggest decline in average monthly depreciation cost, in 2019 this segment’s average depreciation cost was $300.20, which represented a roughly $85 decline in monthly cost over last year. Intermediate cars, light trucks, and SUVs also saw lower monthly depreciation costs.

Data aggregate via AF Research Dept.

Automotive Fleet worked with various fleet management companies who provided depreciation expense data to compile an aggregated look at fleet depreciation expenses in 2019.

To compile this data, we gathered data from each company and then found an overall average of each data point for six vehicle segments.

For the most part, the data reflected the same sentiment that the FMCs expressed, depreciation expenses were down in 2019 compared to 2018.

The biggest year-over-year difference in depreciation expenses came from the full-size van segment, according to the data. In 2019, the average cost of depreciation per month the full-size van segment was $300.20, which represented an $85 decline in monthly cost.

Three other vehicle segments, intermediate car, light truck, and SUV also saw an average monthly depreciation cost decline.

Only two segments saw higher monthly depreciation costs in 2019: compact cars and minivans.

The difference in cost for compact cars was small, roughly $1 more than in 2018. The difference within the minivan segment was more substantial at about $52.

But, even with these two segments posting higher monthly depreciation costs, the overall data shows that 2019 was a strong year for fleet remarketers.

Overall Market Depreciation in 2019

As of November, the 12-month depreciation rate is 14.9%, compared to the 12.7% depreciation rate at the same time last year, according to Anil Goyal, EVP, operations for Black Book.

Summer depreciation was particularly low this year due to strong demand in the wholesale market during the spring and summer season.

Then nearly as soon as the fall season began, average wholesale values saw an abrupt drop. It’s expected that values fall around the fall season but normally it’s a gradual drop. However, due to the strong performance in summer, the fall decline felt abrupt.

“Typically, used vehicles see higher depreciation in the fall relative to other times of the year, driven by softer used vehicle demand after the spring and early summer,” said Zo Rahim, manager, economics & industry insights, for Cox Automotive. “This year, the shift to higher depreciation feels abrupt due to lower depreciation than normal in the spring and summer and it has been a tough comparison to last year’s abnormal strength in summer and early fall.”

Last year’s abnormally strong values were driven by replacement activity caused by hurricanes in Texas and Florida.

Hurricanes this year did not cause the same amount of damage to their affected regions, so the used market did not see a similar type of surge in replacement activity.

Another area of interest in the used market this year is in the retail off-lease segment.

Rahim noted that it is important for remarketers to keep track of how the off-lease market will continue to affect the used-vehicle segment.

Rahim noted that the industry is seeing peak retail off-lease volumes return to market and that these typically strong valued vehicles are beginning to see prices wane.

Many of the retail off-lease vehicles that are returning to market were sold at higher discounts or were packed with incentives to help lower their monthly costs. Now that these vehicles are returning to market, they’re seeing the negative results of these higher discounts and incentives.

This is somewhat of a turn of events for the retail off-lease segment, as up until now, they have been able to secure some of the highest average sale prices.

However, the continued expected supply of retail off-lease vehicles and the robust demand in the used market should mean that off-lease values should still hold strong.

The fact that buyers are showing more interest in the certified pre-owned market means that the higher quality and younger vehicles — such as retail off-lease — returning to the used market next year should perform particularly well.

This bodes well for fleet remarketers, as more and more fleet trim vehicles are being built with the equipment and technology that these types of buyers are interested in, said Krogen of Enterprise Fleet Management.

“In addition, improved safety equipment is a factor we believe will continue to drive resale values,” he added.

Black Book is forecasting an overall depreciation rate of 16% in 2020, which would be higher than it has been in the last few years, but still within healthy market depreciate rates which hover between 16-18%.

Forecast for the Used Market

FMC remarketers have a generally positive outlook for the used market in 2020.

The industry has enjoyed a healthy used market for the past several years, and if the market remains mostly the same, then it should continue to enjoy that healthy market for another year.

“We feel the market will continue to be healthy,” said Garner. “We think there’s perhaps a slight and continuing downturn in 2020. The usual spring market upturn we’ve been used to will also be flatter and not as pronounced. Full-size SUVs and crossovers will continue to slide due to the saturation in the market. Large trucks, Class 7 and Class 8 will go in the gutter because there’s just a saturation of them and the market can’t keep up.”

One trend that will continue to gain prominence next year and in the following years is online remarketing, according to several FMC remarketers.

Wuich noted that online and direct dealer sales were a greater part of his company’s remarketing efforts in 2019. As online remarketing continues to grow in his efforts, and throughout the industry, he expects increasingly detailed condition reports and higher emphasis on vehicle imaging.

Krogen also saw the strength of online remarketing as a sales channel in 2019. One of the biggest benefits that online sales offer, he noted, is the ability to reach buyers outside of traditional office hours.

Another trend in the used market in the coming years will be safety features in vehicles such as advanced driver assistance systems becoming a bigger priority for buyers and sellers.

It will be integral for remarketers to ensure that the safety features in the vehicles equipped with them are operable and that they do their part to identify the features in the vehicles they are selling, noted Wuich.

Electric vehicles are also poised to become a larger part of the auto business, so Wuich and his team will be watching how well EVs hold their residual values.

“With EVs, depreciation expense is a larger share of the total cost pie,” said Wuich. “It will be interesting to see if EVs continue to close the gap on residual percentage.”

If the resale market continues to be as healthy has it has been in the last several years, Wuich expects that customers will continue to cycle their vehicles earlier, in particular, light-duty pickups. The strong resale market combined with the increased cost of new vehicles has made cycling earlier more attractive for fleets, he added.

And, looking ahead more broadly, Garner said that there are many factors down in the near future that can affect the used market, and the overall auto market.

There’s a general skittishness from buyers due to socioeconomic factors.

It’s been 11 years since the last recession, he noted, and everyone is waiting to see what might happen.

Many economists say that a recession is typically followed by another recession after nine years, so some feel the economy is a little past due, he added.

“I think everyone has been holding their breath about the marketplace and about the economy in general,” said Garner. “There was a downturn at the end of 2019, but I think we expected it to be worse than what it was. I think the market has once again come to an end with pretty much flying colors. It was down at the end of the year, but not by much. Historically there should be a breaking point, but so far it hasn’t come, and the market continues to prove us all wrong, at least in the short-term basis, by staying robust.”

Subscribe to Our Newsletter

More Remarketing

Manheim Index Shows Used-Vehicle Wholesale Prices Up 2.1% in June

The market is seeing stronger appreciation in older used vehicles this year, and the most affordable segments have been among the year’s best performers.

Read More →

Commercial Fleet Sales Contribute To June, YTD Gains

The fleet sector has boosted its vehicle purchases at a reliable pace in the first half of this year compared with 1H 2025.

Read More →

Used Vehicle Prices Climb Higher As Sales Pace Slows

The higher prices at used retail reflect strong wholesale values earlier in the spring, particularly for older, more affordable vehicles.

Read More →

Wholesale Used Vehicle Market Sustains Moderate Rise In Values, Prices

Trends continue to normalize after a strong start to the year, as consumers contend with higher gas prices in the coming summer months.

Read More →

Commercial Fleet Sales Still Lead Sectors Despite May Mini Dip

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

How Connected Vehicle Data Is Lifting Fleet Resale Values

A vehicle health score could improve the value of fleet vehicles at remarketing. The path to a universal standard is forming, and fleets that understand the process early will be better positioned when it arrives.

Read More →

Wholesale Used Vehicle Prices Slightly Up In April

The Iranian conflict and rising gas prices inject much uncertainty into the future wholesale used vehicle markets, as higher gas prices soak up spendable income from vehicle buyers.

Read More →

CAR2026: James McKinley Wins Value Champion of the Year

James McKinley of City Rent a Truck was named the inaugural Fleet Value Champion at the CAR Conference for his data-driven approach to fleet lifecycle management and vehicle remarketing.

Read More →

CAR2026: Eric Autenrieth Wins Remarketer of the Year

Eric Autenrieth was recognized at this year's CAR Conference as the Remarketer of the Year.

Read More →

CAR2026: Lawrence Knapp Wins Consignor of the Year

Lawrence Knapp won the Cosigner of the Year award at this year's CAR Conference.

Read More →