Related: Stable Fuel Spend Keeps Lid on Overall Operating Costs

Fuel Prices Increase Fleet Operating Costs

Higher fuel pricing has been the No. 1 factor contributing to higher operating costs in calendar-year 2018. Since fuel makes up the largest portion of fleet operating costs, it has strongly contributed to the increase in total fleet spend.

November 30, 2018

Gasoline and diesel fuel prices have been gradually, but steadily increasing over the past 12 months and have been the No. 1 factor contributing to the increase in total fleet operating costs in calendar-year 2018.

Photo courtesy of Virojt via iStockphoto.

7 min to read

Editors note: This article is part of a seven-part package dealing with operating costs in 2018. Read related articles that offer and in depth look at tire prices, fleet maintenance, warranty recovery, preventive maintenance, fuel spend, and an overview of operating costs.

Gasoline and diesel fuel prices have been gradually, but steadily increasing over the past 12 months and have been the No. 1 factor contributing to the increase in total fleet operating costs in calendar-year 2018.

“The fuel price increase is being driven by record high consumer demand, market uncertainty, sanctions, and a year-over-year decline in oil inventories,” said Kelley Hatlee, CAFS, national service department technical support supervisor for Enterprise Fleet Management.

Crude oil prices increased from an average of $52.51 per barrel in 2017 to a current average of $69.02 so far in 2018. Gasoline and diesel prices started to increase in 2016 and have continued through 2017 into calendar-year 2018.

“The average price of gasoline paid to date in 2018 of $2.79 is about 15% above the average gas price paid in 2017 of $2.42,” said John Wuich, vice president of strategic consulting services for Donlen. “The average diesel price paid to date in 2018 of $3.10 is about 18% higher than the average diesel price paid in 2017 of $2.62.”

Since fuel costs make up the largest portion of fleet operating spend, rising fuel prices have resulted in higher overall fleet operating expense in 2018.

“Overall, fuel prices were up rather significantly this year compared to 2017. Monthly year-over-year fuel price increases ranged from as little as 11% to as much as 30%. As a result, most fleets incurred a considerable jump in operating costs in 2018. And, as is often the case when fuel costs climb, there’s been a renewed interest in strategies to improve fuel efficiency,” said Andy Hall, assistant manager, fuel & GMS for ARI.

Another factor that has put upward pressure on fuel prices in 2018 has been seasonal hurricane activity.

“There was additional consumption driven by Hurricane Florence that caused catastrophic damage in the Carolinas in September 2018. Fleets going to aid in recovery efforts consumed more fuel than was anticipated for the month of September. With many vehicles that fueled early prior to the storm, demand in the Southeast has been low compared to other regions and is only now starting to return to normal,” said George Albright, assistant director of maintenance for Merchants Fleet Management.

Another ongoing trend in 2018, which started to increase in intensity in 2016, has been an uptick in fuel card fraud.

“Credit card skimming has become an increasingly common form of fraud, especially at fuel stations. The most important fuel fraud strategy is to do everything possible to avoid it from happening in the first place,” said Natasha Gonsky, senior manager, fuel management for Wheels.

In the past two years, fleets have seen a rise in activity from fuel fraudsters. It’s critical that fleets monitor their fuel spend regularly and question anything that looks outside the norm. Having a fraud prevention strategy is critical, requires educating drivers so they are aware of the risks and vulnerabilities.

“Unfortunately, there is no fail-proof fraud prevention strategy, so it’s important to maintain constant vigilance for anomalies. Fleets risk losing millions every year from fraudulent card use,” said Gonsky of Wheels. “We work very closely with our vendor fraud departments. We proactively identify and attack fraud in addition to our vendor alerts. Every day we monitor for compromised cards and other fraud schemes. We report suspicious activity to fleets on a daily basis.”

Influence on Vehicle Selection

Fuel spend is one of the highest operating expenses for a fleet, and therefore, vehicle mpg is a large factor in the vehicle selection process.

It is well documented that fuel prices influence vehicle acquisition decisions. New- and used-vehicle markets tend to react to fluctuations in fuel prices. When prices are low, buyers may be more willing to consider larger, less fuel-efficient vehicles, but the converse is not currently happening.

“While prices have trended upward over the past two years, there have not been any noticeable shifts in segmentation or acquisition habits as a result,” said Wuich. “This is likely due to the upward trend being very gradual – slow and steady, while overall average price remains below $3.”

Nonetheless, the price of both unleaded gasoline and diesel No. 2 have been increasing incrementally since 2016. “As fuel prices continue to rise, we expect more fleets will consider alternative-fuel options and focus on reducing the number of miles driven. This can be accomplished through vehicle utilization analysis, which leverages telematics data and vehicle inventory management,” said Mark Lange, CAFM, managed maintenance consultant for Element Fleet Management.

In addition, as fuel prices rise, the resale values of less fuel-efficient vehicles will be impacted. As fuel prices begin to rise, the secondary used-vehicle markets will begin to adjust accordingly.

Fuel Price Forecast for 2019

Fuel prices are impossible to forecast with certainty due to being influenced by a number of variables and dynamics outside the control of fleets. As a result, most fleet management companies use the U.S. Energy Information Administration (EIA) forecasts for internal planning and fuel price forecasting.

“It is difficult to project fuel prices because there are simply too many external variable influences. We watch closely for EIA forecasts for both internal planning and external customer purposes. Currently, the EIA expects a gradual price increase to continue into 2019, with average gas price expected to increase by about $0.06 a gallon,” said Wuich of Donlen.

Although fuel prices are predicted to increase in calendar-year 2019, the forecast is for the increase to be stable.

“The EIA projects that average fuel expenses should remain relatively stable through the remainder of 2018 and into 2019 while following the normal seasonal trends. In turn, fleets will continue to emphasize appropriate driver behavior, implement telematics solutions, and choose strategic vehicle selections to mitigate these higher fuel costs,” said Mark Donahue, manager, fleet analytics & corporate communications for EMKAY.

Another indicator used to forecast future fuel prices is the oil futures market, where investors buy future oil contracts based on anticipated prices as a form of hedging or as an investment to sell at a future date if actual prices are higher. The oil futures market seems to reinforce the contention that oil prices will be higher in 2019. A key indicator is that the global inventory of oil continues to lag user demand.

Most forecasts predict moderate fuel prices for the next few years, with limited movement up or down.

The forecast of modestly rising fuel prices will be a factor influencing 2019 model-year acquisition decisions. Since fuel cost is still one of the top contributors to the overall operating cost per mile, fuel economy for internal combustion engine vehicles remains a top focus during the vehicle selection process.

The EIA estimates that U.S. crude oil production averaged 10.9 million barrels per day in August 2018, up by 120,000 barrels per day from June 2018. U.S. crude oil production will average 10.7 million barrels per day in 2018, up from 9.4 million barrels per day in 2017.

Furthermore, U.S. oil production averaged 10.7 million barrels per day, which is the highest annual average production in U.S. history, surpassing the previous record of 9.6 million barrels per day in 1970.

“Refineries have been running higher in 2018 compared to 2017, producing new run records. June 2018 was a record month for the demand of gasoline with high U.S. imports to match. Outside of the supplier and refinery space, Americans are continuing to hold onto vehicles longer which keeps demand level but are still looking for alternatives for maximum efficiency and cost for the future,” said Albright of Merchants Fleet Management. “Prices have been steady but are on the rise, reaching our highest annual average since 2014. Refineries are entering maintenance season causing a dip in new production and unknowns around downtime.”

While fuel prices are rising, pricing is not volatile as in the past, subject to sharp swings.

“Many analysts predict fuel prices to remain fairly high but stable. Economic factors such as greater GDP growth and lobbying efforts for 95 octane as the new standard could push fuel prices beyond forecasted levels,” said Hatlee of Enterprise Fleet Management.

In the final analysis, the price of fuel is governed by global supply and demand, which is especially true since the emergence of the mega-economies in China and India. The forecast is for global demand to likely continue to remain strong and possibly increase.

Sustainability Initiatives

Lower fuel prices have traditionally impacted the sales of hybrids and alternative-fueled vehicles. But, with the multitude announcements from OEMs about future hybrid and battery-electric vehicles, there has been an increased interest in these products by fleet managers

Sustainability initiatives at multinational companies also plays a factor in corporate fuel initiatives. Since higher fuel efficiency translates into lower emissions, sustainability mandates encourage acquisition decisions to focus on smaller displacement, more efficient engines.

“Some fleets are looking more seriously at electric vehicles for fuel cost reduction in addition to improving fuel economy as part of the model-year planning process. We’ve also observed increased interest in exploring gasoline engine alternatives to a diesel where the need for a diesel’s high torque output isn’t essential – especially true where trailer towing isn’t a requirement,” said Chad Christensen, strategic consultant for Element.

Subscribe to Our Newsletter

More Fuel

Turning Fleet Payment Data into Executive Insights

Ramel Lindsay of U.S. Bank Voyager discusses how fleets can transform payment and transaction data into actionable intelligence to reduce costs, improve oversight, and support executive decision-making.

Read More →

Why the IRS Raised Its Mileage Rate in the Middle of 2026

Fuel-price volatility drove the rare increase to 76 cents per mile, the fifth midyear adjustment since 2000.

Read More →

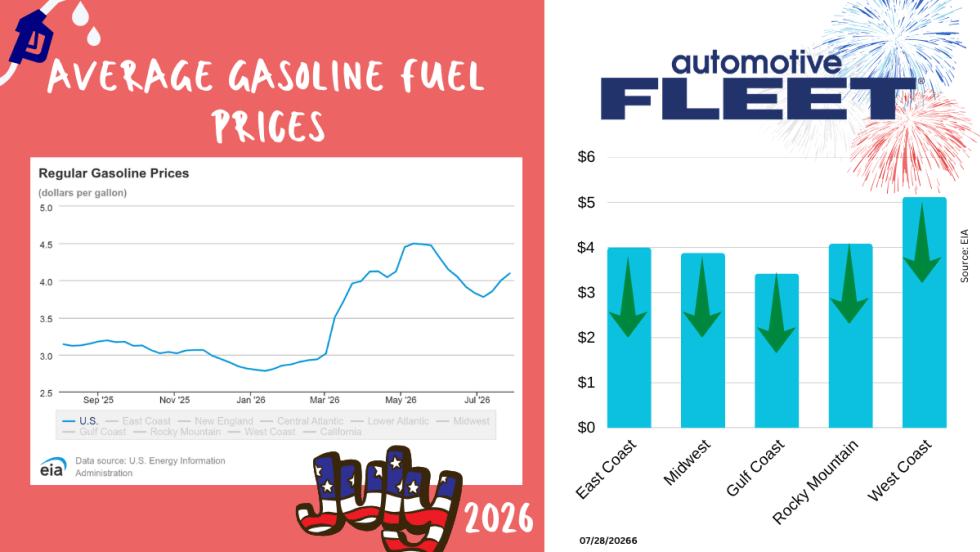

July Fuel Update: Prices Keep Rising in Light of More Conflict

Gas prices continue to rise as more and more conflicts do, too.

Read More →

Bob Adamsky on Fuel Volatility: "Don't Panic, Have a Plan."

When it comes to up and down fuel prices, Adamsky has a message for fleets: “Don’t panic.”

Read More →

How Fleets Can Gain Control of Non-Fuel Spend

Fuel often gets the spotlight, but non-fuel expenses can have a major impact on fleet costs. Ramel Lindsay of U.S. Bank Voyager discusses how fleets can gain better visibility and control over these often-overlooked expenditures.

Read More →

Fuel is Just the Start: How Middle East Tensions are Driving Up Fleet Maintenance Costs

The Middle East conflict is doing more than pushing up fuel prices. It’s also raising the cost of key maintenance products your fleet depends on, from motor oil to tires to windshield wipers. Here’s what you need to know about this budget-busting situation.

Read More →

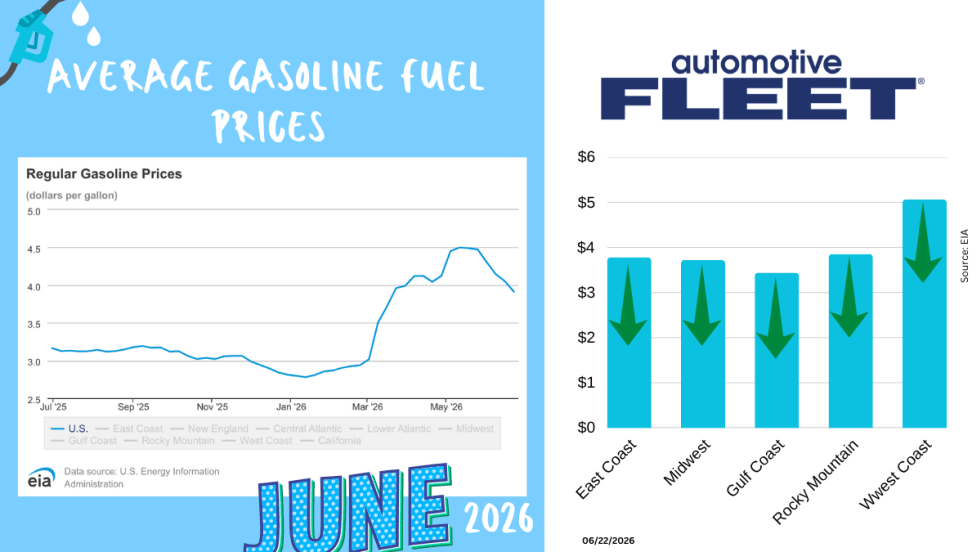

June Fuel Update: Prices Fall Below $4

Drivers are finally getting some relief at the pump. The national average gas price has dropped below $4 a gallon for the first time in months, with prices falling in 47 states as oil markets react to developments in U.S.-Iran negotiations.

Read More →

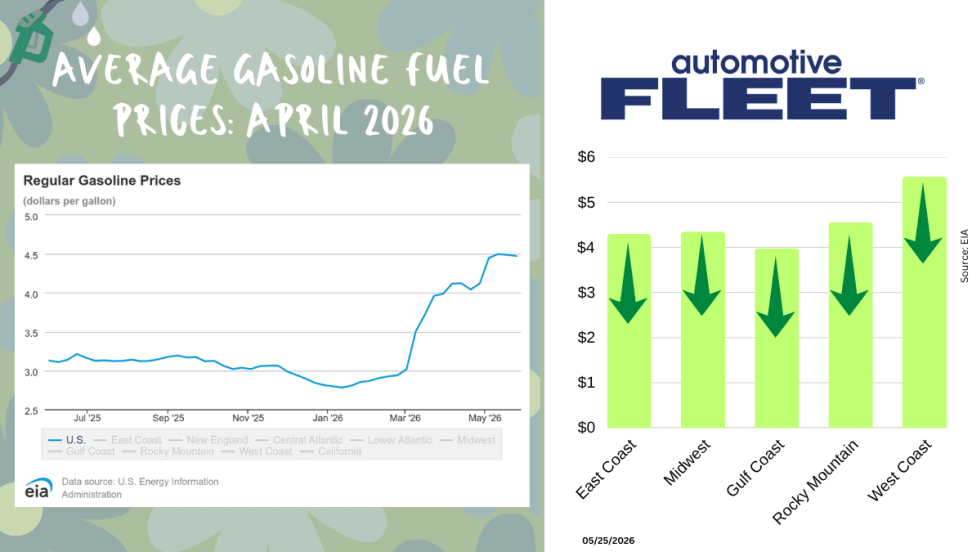

Study: How 2026's Gas Price Hikes Affect Different Vehicle Types

New data from iSeeCars reveals how rising fuel costs have affected different vehicle segments as gasoline prices climbed nearly 46% over the past four months.

Read More →Sponsored•May 29, 2026

Are You Tracking Your Fleet's True Total Cost of Ownership?

Bobit Business Media surveyed 190 fleet professionals and found that while most fleets are tracking costs, fragmented systems and data gaps are keeping true TCO visibility out of reach. With rising pressure to control spend in an increasingly volatile environment, the gap between what fleets think they know and what the data actually shows is wider than you might expect. See how your peers are managing costs today and where the industry still has room to improve.

Read More →

May Fuel Update: All Regions Experience Declines

Gas prices are finally easing in much of the country, but experts warn global tensions could quickly reverse the trend as the national average remains well above last month’s levels.

Read More →