Forecast of Operating Costs for CY-2015

If one word could describe the forecast for CY-2015 operating costs, it would be "flat." The upbeat forecast is for gasoline and diesel prices to slightly decrease, while maintenance and tire costs are predicted to remain stable.

Photo via Pixabay.

Photo via Pixabay.

If industry predictions hold true, the 2015 calendar-year could represent the third consecutive year that fleet operating costs will remain stable compared to the year prior.

Almost all subject-matter experts believe replacement tire expenses will remain flat, barring any disruption to world commodity prices or the price per barrel of crude oil. Similarly, industry cost projections about preventive maintenance and scheduled/unscheduled repair forecast fleet expenses to remain stable vis-à-vis those in 2014.

Below is a more detailed examination of these forecasts broken down by each operating cost category:

Fuel Costs Forecast to Decline

All fleet management companies based their fuel price forecasts on those projected by the U.S. Energy Information Administration (EIA).

“The U.S. EIA currently projects that U.S. pump prices will continue their multi-year decline into 2015. Its October 2014 short-term energy outlook includes forecasts for gasoline and diesel of $3.38 and $3.80 per gallon, respectively, for 2015,” said Bob Sandler, senior vice president, customer experience & enterprise consulting at Element Fleet Management. “The long-term decline in fuel prices is largely driven by falling global crude oil prices, and the expectation that this trend will continue in the face of weaker global demand and increasing crude oil supplies.”

As of press time, the U.S. surpassed Saudi Arabia as the No. 1 producer of crude oil, hitting a production rate of 12 million barrels per day. This milestone has been achieved with the U.S. only scratching its full potential as a re-energized oil-producing country, with the majority of oil shale deposit formation yet to be fully exploited.

“Both gasoline and diesel prices are expected to decline somewhat in 2015 as U.S. production of oil continues to increase and oil imports decrease,” said Amy Blaine, vice president, consulting, analytics, and sustainability at Donlen.

However, Blaine cautioned that fleets should still budget conservatively for 2015 fuel expenditures.

“While pricing has been more stable than in the previous three or four years, fuel prices are still high and volatile compared to long-term historical trends so we recommend that fleets budget conservatively,” she added.

Referencing U.S. government forecasts, the EIA pump price outlook is more than 10 cents per gallon below the 2013 averages for both fuels, and recognizes that normal price variability can be expected during the year ahead.

“Of course, fuel prices can be highly volatile depending on weather, the economy, and geopolitical events related to the supply and demand of petroleum-based products,” said Sandler of Element Fleet Management. “So, barring the unforeseen, fleets should experience an improving cost-per-mile environment for fuel, as pump prices are expected to continue their recent decline, and as overall fleet fuel economy continues to improve.”

Similarly, GE Capital Fleet Services cited the EIA for its forecast of fuel prices in the 2015 calendar-year.

“The EIA forecast for 2015 expects gasoline prices to decline 5.2 cents from 2014 and 4.8 cents for diesel. If these declines are realized, fleets can expect a 1.24- to 1.50-percent decline in fuel costs due to prices,” said Jayme Schnedeker, fuel product manager at GE Capital Fleet Services.

Likewise, LeasePlan USA cited reliance on the EIA as its forecasting source for future fuel prices.

“Due to the inherent volatility and uncertain supply and demand variables impacting the price of fuel, LeasePlan relies heavily on established government/industry forecasts (mainly U.S. EIA) for internal planning and external fuel price forecasting. Currently, the EIA is forecasting average retail pump prices to be $3.18 per gallon in December 2014, with an average of $3.46 per gallon for 2014 and $3.41 for 2015,” said Paul Fortin, economist and vice president of strategic modeling and analytics research team at LeasePlan USA.

If all of the fuel forecasts could be summarized, it would be under the heading of stability as illustrated by the below observation from Tony Piscopo, director, fleet management services at ARI.

“We expect to see continued stability in pricing at the pump, understanding that the market can change dramatically overnight due to global events. Basic supply and demand economics for gasoline and diesel products suggests a relatively flat market for the foreseeable future,” said Piscopo.

However, some believe it is impossible to accurately predict the future price of fuel.

“There are too many variables to make a reliable prediction,” said John Bauer, manager, fleet analytics at Wheels Inc.

PM and Maintenance Forecast

As with fuel, the interviewed subject-matter experts forecast flat prices for preventive maintenance and scheduled/unscheduled repairs in 2015 when compared to 2014.

“We expect PM pricing to either remain flat or decrease somewhat. Continued stability related to the cost of oil, along with increasing drain intervals and increasing acceptance of synthetics should have a favorable impact on PM costs. Additionally, more OEMs are offering free services, which will lower perceived costs in this area,” said Piscopo of ARI.

In addition, the trend of downsizing to smaller displacement engines will result in fewer quarts of oil consumed during an oil change, since these engines have smaller capacity oil crankcases.

“We expect to see oil crankcase capacities decrease as engine sizes are trending smaller. This should reduce the amount of oil needed for an oil change, resulting in lower costs,” said Chad Christensen, strategic consultant at GE Capital Fleet Services.

Also, more new models have oil-life monitoring systems, which allow for longer intervals between oil drains.

“More new vehicles will have oil life monitoring systems and extended drain intervals, which should help lower a fleet’s overall oil change costs. Commercial fleets’ transition to these newer vehicles should plateau soon,” said Christensen of GE Capital Fleet Services.

Although more expensive per quart, more OEMs are recommending the use of synthetic oils, which have a longer oil drain interval.

“Unit costs for oil will continue to increase, but oil change intervals will increase as well. Fleet maintenance costs will rise, but not at the same rate as the cost of oil. Taking advantage of both the extended intervals and the manufacturers’ service programs will offset some of the increased costs,” said Dale Jewell, manager, U.S. maintenance center operations at Emkay.

One strategy to mitigate the higher cost of synthetic oils is to switch to less expensive synthetic blends.

“Fleets are mitigating the increased cost of synthetic oils by opting for synthetic blends as opposed to pure synthetic oils,” said Megan McMillan, client consultant at Donlen.

One future trend that will put downward pressure on maintenance costs is accelerated replacement programs to compensate for the deferred replacements that occurred during the recession.

“Many fleets, particularly truck fleets, kept vehicles longer during the recent economic downturn, but, since the recovery, they are now refreshing their fleets and cycling those vehicles out, so we are seeing lower maintenance expenses as a result,” said McMillan.

Another maintenance trend that will gain greater importance in the future is driver downtime.

“Downtime versus cost continues to be a hot topic among many commercial fleets. As fleets become leaner with less spare units, downtime becomes more critical. This is exacerbated in certain areas where good shops and availability of technicians is limited,” said Piscopo. “Many of the newer technologies from the past few years have proven to be comparatively trouble free and not a significant driver of maintenance/repair expenses as in past years.”

The overall forecast for fleet maintenance trends is that they will remain flat in 2015.

“Our data indicates that maintenance and repair costs remained flat in 2014,” said Sandler of Element Fleet Management.

Replacement Tire Price Forecast

The industry consensus is that, barring any disruptions in commodity prices and the price of oil, the prices for replacement tires should remain flat in the 2015 calendar-year.

“We anticipate tire pricing to stay flat in 2015, the exception being any new larger/unique tire sizes introduced to the market by the OEM. Those tires are typically initially more expensive until competition increases bringing costs down,” said Robert Cascarano, manager, fleet management services at Donlen.

Also expected to impact future replacement tire prices are the OEM strategies to meet the stricter CAFE requirements.

“In an effort to conform to CAFE standards, manufacturers are replacing spare tires with OE tire fitments of run flat technology or cans of ‘fix-a-flat.’ This eliminates the extra weight of a spare tire and jack, thus giving the vehicle better gas mileage. Many fleets are then forced into using retrofitted spares for their vehicles, as they do not want their fleet drivers dealing with self-administered flat repairs,” said David Jankiewicz, director, maintenance and repair management at LeasePlan USA.

Similarly, with the forecast of oil prices to remain stable, the feeling is that tire prices will likewise remain stable.

“We don’t think there will be significant changes given that oil prices are not expected to rise,” said Bauer of Wheels Inc.

There will still be a lag time in the aftermarket having replacement tires available for all-new, larger diameter tires.

“Manufacturers will continue to produce units with unique tire sizes, which are more costly. Unfortunately, the lead times for aftermarket alternatives is typically longer than the lifecycle of the average fleet vehicle’s first set of tires. Costs will remain high for current vehicles and drop incrementally for vehicles nearing the end of their lifecycle,” said Jewell of Emkay.

Related:

More Fuel

Turning Fleet Payment Data into Executive Insights

Ramel Lindsay of U.S. Bank Voyager discusses how fleets can transform payment and transaction data into actionable intelligence to reduce costs, improve oversight, and support executive decision-making.

Read More →

Why the IRS Raised Its Mileage Rate in the Middle of 2026

Fuel-price volatility drove the rare increase to 76 cents per mile, the fifth midyear adjustment since 2000.

Read More →

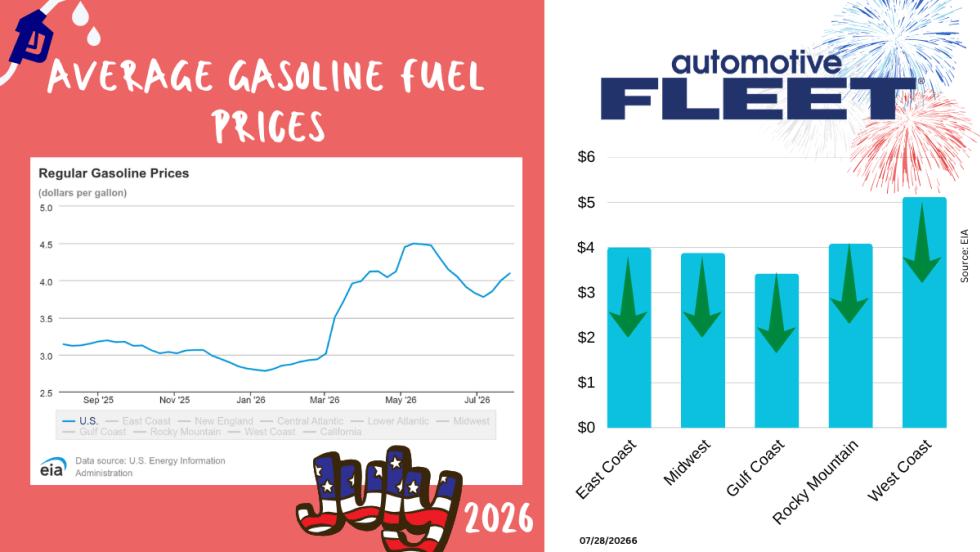

July Fuel Update: Prices Keep Rising in Light of More Conflict

Gas prices continue to rise as more and more conflicts do, too.

Read More →

Bob Adamsky on Fuel Volatility: "Don't Panic, Have a Plan."

When it comes to up and down fuel prices, Adamsky has a message for fleets: “Don’t panic.”

Read More →

How Fleets Can Gain Control of Non-Fuel Spend

Fuel often gets the spotlight, but non-fuel expenses can have a major impact on fleet costs. Ramel Lindsay of U.S. Bank Voyager discusses how fleets can gain better visibility and control over these often-overlooked expenditures.

Read More →

Fuel is Just the Start: How Middle East Tensions are Driving Up Fleet Maintenance Costs

The Middle East conflict is doing more than pushing up fuel prices. It’s also raising the cost of key maintenance products your fleet depends on, from motor oil to tires to windshield wipers. Here’s what you need to know about this budget-busting situation.

Read More →

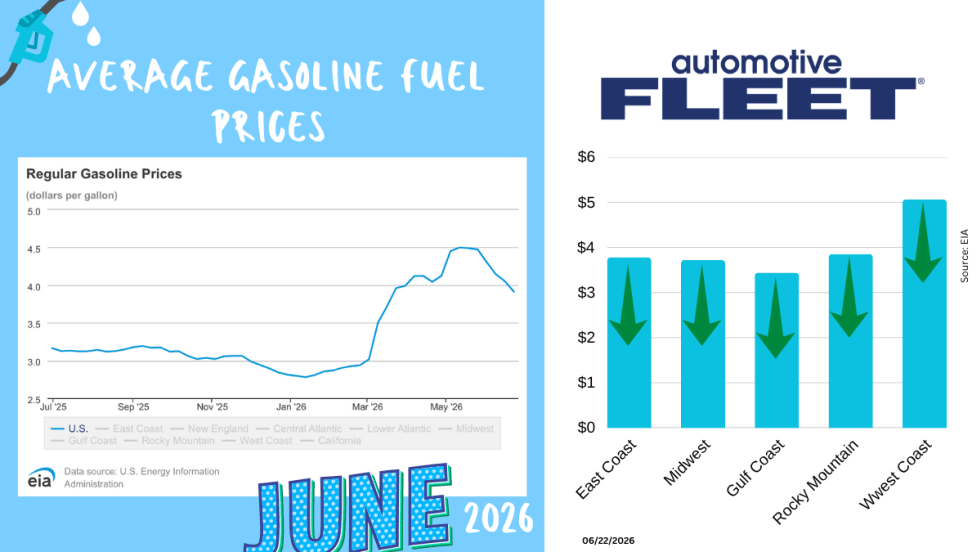

June Fuel Update: Prices Fall Below $4

Drivers are finally getting some relief at the pump. The national average gas price has dropped below $4 a gallon for the first time in months, with prices falling in 47 states as oil markets react to developments in U.S.-Iran negotiations.

Read More →

Study: How 2026's Gas Price Hikes Affect Different Vehicle Types

New data from iSeeCars reveals how rising fuel costs have affected different vehicle segments as gasoline prices climbed nearly 46% over the past four months.

Read More →Are You Tracking Your Fleet's True Total Cost of Ownership?

Bobit Business Media surveyed 190 fleet professionals and found that while most fleets are tracking costs, fragmented systems and data gaps are keeping true TCO visibility out of reach. With rising pressure to control spend in an increasingly volatile environment, the gap between what fleets think they know and what the data actually shows is wider than you might expect. See how your peers are managing costs today and where the industry still has room to improve.

Read More →

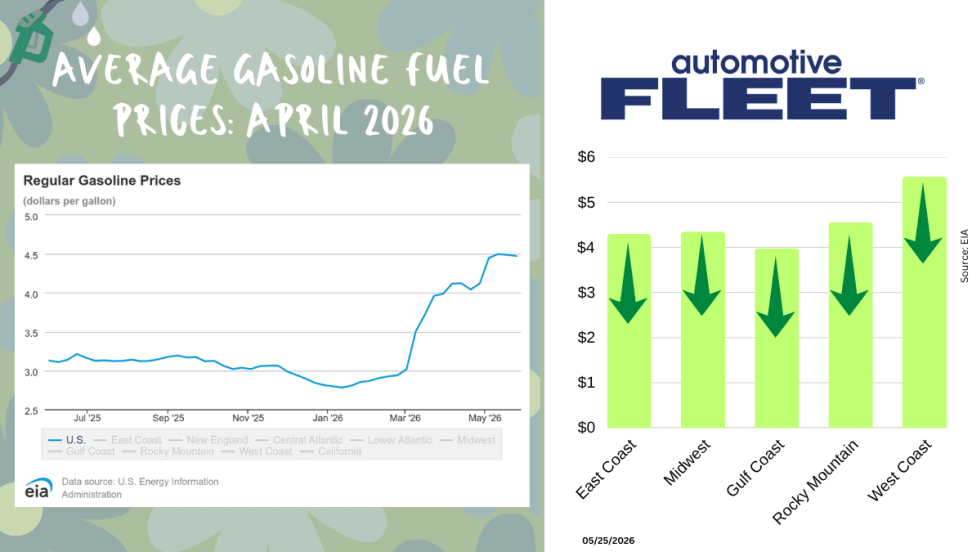

May Fuel Update: All Regions Experience Declines

Gas prices are finally easing in much of the country, but experts warn global tensions could quickly reverse the trend as the national average remains well above last month’s levels.

Read More →