Operating Costs Flat for Second Consecutive Year

Gasoline and diesel prices, on average, in 2014 are virtually the same as in 2013, with some variances depending on region. Similarly, PM costs are flat and stable commodity prices have contributed to less volatility in tire prices.

For the second consecutive year, overall operating costs have remained flat for commercial fleets compared to the prior year.

There are a variety of factors as to why operating costs for fuel, replacement tires, scheduled/unscheduled repairs, and preventive maintenance (PM) were flat in the 12 months ending August 2014 compared to the previous 12 months.

Since fuel is the largest operating cost, the flat pricing at the pump was the No. 1 contributor to stable fleet expenses. In addition, longer oil drain intervals and fewer unscheduled maintenance repairs helped keep a lid on operating costs in the 2014 calendar-year.

These findings and others are revealed in Automotive Fleet’s 23rd annual operating cost survey, based on data provided by seven survey partners:

ARI.

Donlen.

Element Fleet Management.

Emkay, Inc.

GE Capital Fleet Services.

LeasePlan USA.

Wheels Inc.

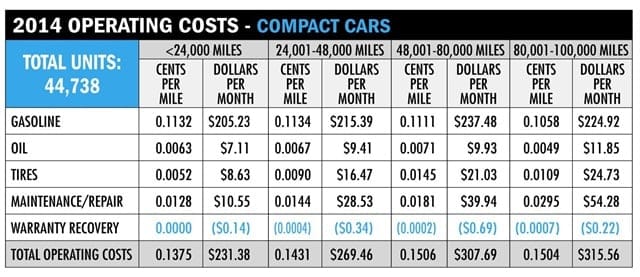

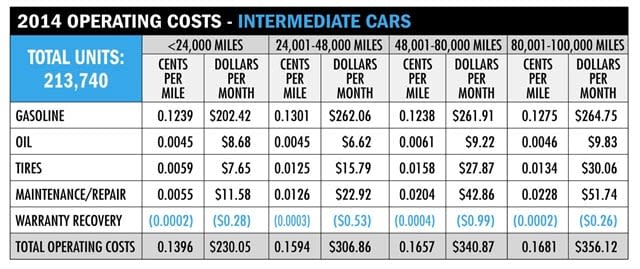

This year’s survey is based on analysis of actual operating costs incurred by 799,074 vehicles operated by commercial fleets, which are managed by these seven fleet management companies.

Price Stability at the Fuel Pump

While still the largest component of fleet operating costs, the price of fuel has remained stable during the past 12-month period, without the pricing volatility that often occurred in prior years.

“The change in national average gasoline prices from 2013 to 2014 is expected to be the closest to 0 percent in more than 15 years,” said Jayme Schnedeker, fuel product manager at GE Capital Fleet Services. “As a result, the impact in fuel costs were driven more by consumption, rather than price. For diesel, the annual change in the national average price has been the closest to 0 percent the past two years, providing price consistency for fleets; however, variances still remain between regions. The West Coast, in particular, is expected to be a full 30 cents above the national average in 2015.”

All of the participating fleet management companies cited the flat pricing of fuel as a key factor in this year’s survey. “Fuel prices did not change significantly year-over-year,” said John Bauer, manager, fleet analytics at Wheels Inc.

There continues to be the normal seasonal cyclicality in fuel prices in the fall and spring, but the key factor is that this pricing cyclicality does not have an upward trajectory and prices are behaving very similar to those in 2013. However, one factor with a growing impact on moderating fleet fuel spend is the overall increases in vehicle fuel economy.

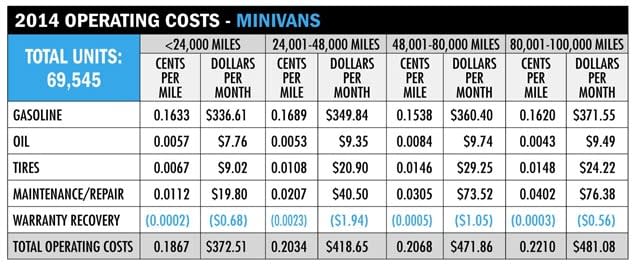

Chart by Armie Bautista.

“We observed gasoline/diesel prices remaining virtually the same in 2014 compared to 2013. We are also seeing fleets save on fuel costs due to the fact that the newer vehicles average better fuel economy. As fleets swap out older, less-efficient vehicles, they reduce their fuel spend,” said Bob Sandler, senior vice president, customer experience & enterprise consulting at Element Fleet Management.

For companies in industries that are growing, the overall number of gallons of fuel consumed is similarly increasing. However, effective fleet management strategies are helping curb increases in total fuel spend.

“Gallon consumptions have increased 63 percent for diesel and 2.98 percent for gasoline in the past 12 months,” said Mark Donahue, team lead, fleet analytics at Emkay. “We have experienced a rapid increase in diesel, light-duty truck utilization and portfolio growth. Current portfolio fleets have further utilized newer vehicle technologies, implemented appropriate driver behavior measures, and rightsized their fleets to help mitigate increases in fuel spend.”

The encouraging news is that fuel prices are forecast to decline in the 2015 calendar-year. (See page 40 in this issue for a more detailed forecast.)

“U.S. production of crude oil is approaching levels last seen at the peak of U.S. production in 1970. As a result, oil imports have declined and are now at levels last seen in the late 1960s. Increasing production in the U.S. has stabilized fuel pricing considerably. Next year, gasoline prices are expected to be approximately 5-cents-per-gallon lower than in 2014. Diesel prices are also expected to decline moderately in 2015,” said Amy Blaine, vice president of consulting, analytics, and sustainability at Donlen.

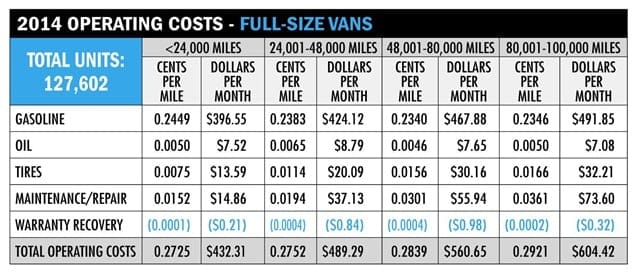

Chart by Armie Bautista.

One consequence of stable fuel pricing for gasoline and diesel is a corresponding decrease in fleet interest in alternative fuels.

“With pump prices currently averaging $3.28 per gallon, we have seen a lull in analytical requests and order activity for hybrids and other alternative-fuel vehicles in 2014,” said Becky Langmandel, director of strategic modeling and analytics research team at LeasePlan USA. “However, since fuel cost is still one of the top contributors to the overall operating cost per mile, fuel economy remains a top focus during the vehicle selection process.”

In addition to stable pricing, technological advances are making gasoline powertrains very fuel efficient and are dramatically reducing emissions.

“Hybrids and alt-fuel vehicles are still great options with an attractive ROI; however, the efficiency of many gasoline vehicles has improved, considerably narrowing the operating cost gap between the regular and alt-fuel versions of similar vehicles. The 2015 Ford F-150 with the new aluminum body is an example of one of the ways OEMs are using new technology to improve the fuel economy of the standard gasoline engine,” said Blaine of Donlen.

Stable Replacement Tire Prices

In 2014, the cost of replacement tires was flat, which was a welcome relief to past years of year-over-year price increases, primarily driven by higher commodity prices, the trend to larger diameter tires, and supply shortages of specific size tires in the aftermarket.

“Although tire costs in 2014 generally remained comparable to 2013, we have seen prices decreasing among some of our key suppliers,” said Sandler of Element Fleet Management. “Barring some extraordinary circumstances, we expect prices to remain at the same level for the remainder of 2014 and into 2015.”

Stability in oil prices, the key ingredient in tire manufacturing, helped rein in prices.

“New tire costs have stabilized as a result of less volatile and lower average oil prices. There have been instances of tire models being discontinued and replaced by higher-priced tires in a comparable design and size. We continue to see larger wheel diameters, but with greater availability of these replacement tires than years ago,” said Chad Christensen, strategic consultant at GE Capital Fleet Services.

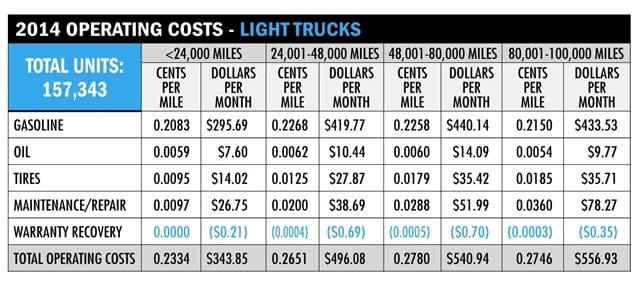

Chart by Armie Bautista.

While the availability of larger diameter replacement tires is improving, these tires are increasing overall costs for the simple reason that the larger the tire, the greater the cost.

“The continued trend toward larger diameter, lower-profile tires is driving costs up significantly. Several manufacturers use unique tire sizes that are not widely available, and this drives costs up as well,” said Dale Jewell, manager, U.S. maintenance center operations at Emkay.

In addition, tire expenses are being influenced by changing fleet applications for certain vehicles.

“Tire costs, year-over-year, were similar; some vehicle types were higher, while others were lower. There are a number of contributing factors, including more high-mileage compact vehicles than last year, which led to higher costs at high mileage. As more fleets use the Ram Cargo and Ford Transit Connect, fewer minivans are being used as service tech vehicles, which is reflected in the lower miles per month for minivans,” said Bauer of Wheels Inc.

Maintenance & Repair Trends

Ongoing improvements in vehicle quality and reliability, along with extension of OEM powertrain warranties, also help keep fleet maintenance costs stable.

“Today’s vehicles are built to last and are more reliable now than ever before,” said Sandler of Element Fleet Management. “Plus, we’re seeing a number of manufacturers covering maintenance costs, thus driving down the total cost of ownership. With manufacturers covering basic maintenance costs, such as tire rotations and oil changes for the first 25 months, fleets are saving money.”

With increased vehicle complexity resulting from the expanded use of electronics, infotainment systems, and accident avoidance technology, the conventional wisdom is that maintenance costs were destined to rise in the future; however, this is not the case.

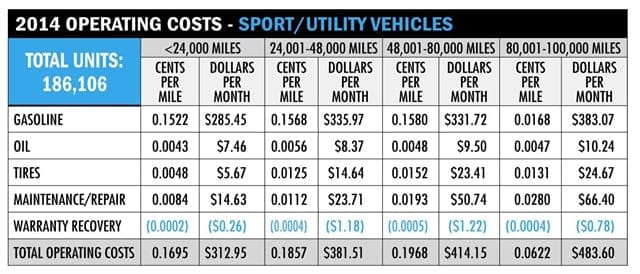

Chart by Armie Bautista.

“We keep expecting maintenance costs to increase, but they remain relatively flat. Although some repairs are more costly, the total number of component failures is declining. In a study of light-duty trucks kept in service over 125,000 miles, we experienced virtually no engine and transmission failures that could not be attributed to lack of recommended preventive maintenance,” said Bauer of Wheels Inc.

In fact, some maintenance costs are actually declining. “The overall cost of maintenance is decreasing slightly, due to extended service intervals and the manufacturers’ complimentary maintenance programs. Parts costs and labor rates are rising, but the rate of failure of most components is declining,” said Jewell of Emkay.

One unintended consequence of increased vehicle complexity is that manufacturer scheduled maintenance is being dictated by onboard monitoring devices.

“As manufacturers move from standard intervals for routine maintenance to sophisticated computer calculations, fleet vehicles are having fewer routine tire, brakes, and overall vehicle condition inspections. This is leading vehicles to have premature and more in-depth repairs, where, in the past, simple tire rotations, lubrications, and/or ‘hang and turns’ kept fleets from major replacements and repairs,” said David Jankiewicz, director, maintenance and repair management at LeasePlan USA.

The large number of OEM recalls has also impacted fleet costs.

“OEM recalls have impacted driver productivity and rental costs. Awareness of recall repairs not performed by individual fleet drivers is critical. There are also technology tools to identify vehicles with ‘open recalls.’ One option is automated e-mail alerts available from www.safercar.gov as it provides timely information on recent recalls by year-make-model,” said Eric Strom, maintenance & safety product manager at GE Capital Fleet Services.

Chart by Armie Bautista.

Preventive Maintenance Trends

Preventive maintenance cost trends have been flat for a number of years, primarily due to OEMs extending the mileage intervals between oil drains.

“Overall, PM costs remained relatively flat during the past year. This is mainly attributable to the stability in the cost of oil. An additional factor is the decreasing costs of synthetic oils and their increased usage in fleet applications,” said Tony Piscopo, director, fleet management services at ARI.

The use of synthetic oil, as recommended by an OEM, is increasing.

“More vehicles are requiring blended and/or synthetic motor oil, which costs more per quart, increasing the overall average price per oil change,” said Strom of GE Capital Fleet Services. “However, extended oil change intervals have helped offset the rising cost per change, keeping overall costs fairly stable.”

Extended oil drain intervals due to synthetic oil use was cited by others as helping offset the increased per-quart cost. “The continued switch to synthetic and synthetic blends will keep transaction prices higher; however, some of the increase is being mitigated by extended maintenance intervals,” said Megan McMillan, client consultant at Donlen.

This observation was echoed by Mike Crumlett, manager, North America truck services at Emkay. “Manufacturers have adopted more stringent oil requirements, increasing the cost of each maintenance service significantly; however, the intervals required have grown longer, mitigating some of the cost,” he said.

Discussions between fleet management companies and their national account partners have reinforced this trend.

“While we’ve seen an increased cost-per-quart of oil, the intervals between oil changes are extended, resulting in little to no financial impact. One of our suppliers believes this trend will remain as more fleets are moving toward synthetic oils. Based on various conversations with our suppliers, we believe this trend will continue into 2015,” said Sandler of Element Fleet Management.

Another trend impacting fleet preventive maintenance costs has been dealers offering free scheduled maintenance coverage, such as oil changes and tire rotation, during the initial one or two years of ownership; however, this is not translating into the anticipated cost savings.

“There’s one key difference we haven’t observed: Oil costs have not gone down as we would have expected as free preventive maintenance and extended service intervals become more common. It’s our feeling that the anticipated reduction has been offset by requirements for synthetic oil and drivers electing to use quick change franchises instead of returning to dealers for free service,” said Bauer of Wheels Inc.

Chart by Armie Bautista.

Warranty Recovery Trends

The ongoing trend for a number of years has been the declining amount of warranty recovery monies being made available to fleet customers.

“We didn’t witness any big jumps regarding warranty recovery in 2014. Overall, it remained flat,” said Sandler of Element Fleet Management.

One factor causing flat or declining warranty recovery monies is that manufacturers have extended powertrain warranties to 100,000 miles. “Manufacturers have been reducing their participation in goodwill adjustments based on the extension of their warranties. As the quality of new vehicles continues to improve, there are fewer opportunities to go back to the OEM for goodwill,” said Robert Cascarano, manager, fleet management services at Donlen.

This observation was seconded by Jewell of Emkay. “Most of the warranty recovery is occurring during the term of the new vehicle’s warranty. Longer base and powertrain warranties have led to a reduction in post-warranty recovery,” he said.

Another factor is a trend by OEM franchised dealers to attract more fleet maintenance business.

“Warranty recovery, from an FMC standpoint, continues to decrease slightly. The main factor is due to the better quality of vehicles being produced. Additionally, the OEMs’ desire to direct more business toward their franchised dealers fuels a reluctance to support fleets in a post-warranty or policy environment,” said Piscopo of ARI.

Most post-warranty policies by OEMs have remained unchanged from 2013 to 2014. “There have been no significant changes in the OEM post-warranty policy adjustment claim policies or recoveries in the past year,” said Strom of GE Capital Fleet Services.

Bauer of Wheels agrees: “We saw no significant change in warranty recovery,” he said.

While policies have not changed, fleets need to be vigilant that they scrupulously follow these policies. “Fleets need to ensure OEM service requirements are followed and maintenance histories maintained, or policy adjustment claims may be denied,” said Strom of GE Capital Fleet Services.

This was seconded by Christensen of GE Capital Fleet Services: “Driver education and awareness of key preventive maintenance items due will be critical as OEMs may require maintenance history documentation on major repairs,” he said.

Where this becomes complicated is with the increased number of specialized services required by manufacturers. “It is very important that drivers adhere to their maintenance schedules. Manufacturers are dissecting maintenance histories to ensure units are strictly adhering to maintenance intervals before offering any assistance on repairs,” said Tony Blezien, vice president, operations at LeasePlan USA.

Related:

More Fuel

Turning Fleet Payment Data into Executive Insights

Ramel Lindsay of U.S. Bank Voyager discusses how fleets can transform payment and transaction data into actionable intelligence to reduce costs, improve oversight, and support executive decision-making.

Read More →

Why the IRS Raised Its Mileage Rate in the Middle of 2026

Fuel-price volatility drove the rare increase to 76 cents per mile, the fifth midyear adjustment since 2000.

Read More →

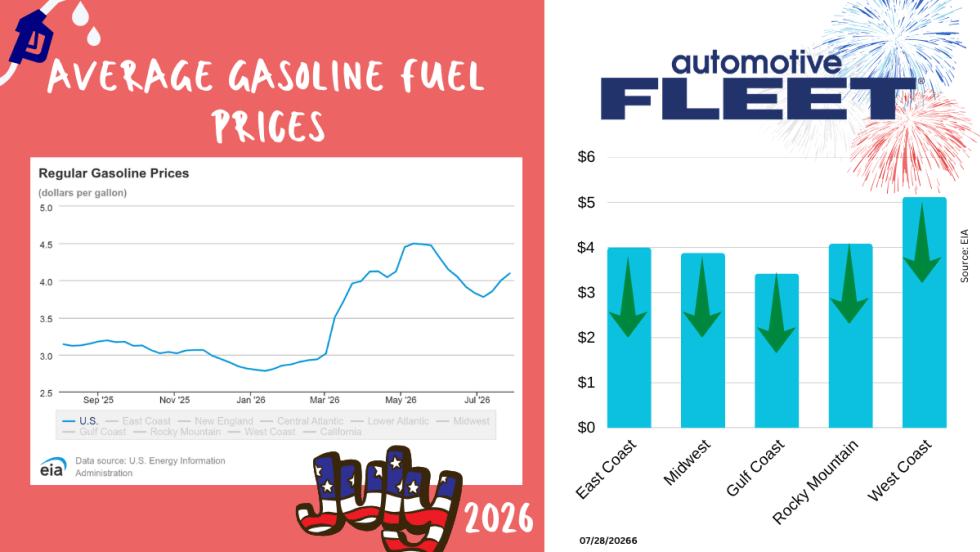

July Fuel Update: Prices Keep Rising in Light of More Conflict

Gas prices continue to rise as more and more conflicts do, too.

Read More →

Bob Adamsky on Fuel Volatility: "Don't Panic, Have a Plan."

When it comes to up and down fuel prices, Adamsky has a message for fleets: “Don’t panic.”

Read More →

How Fleets Can Gain Control of Non-Fuel Spend

Fuel often gets the spotlight, but non-fuel expenses can have a major impact on fleet costs. Ramel Lindsay of U.S. Bank Voyager discusses how fleets can gain better visibility and control over these often-overlooked expenditures.

Read More →

Fuel is Just the Start: How Middle East Tensions are Driving Up Fleet Maintenance Costs

The Middle East conflict is doing more than pushing up fuel prices. It’s also raising the cost of key maintenance products your fleet depends on, from motor oil to tires to windshield wipers. Here’s what you need to know about this budget-busting situation.

Read More →

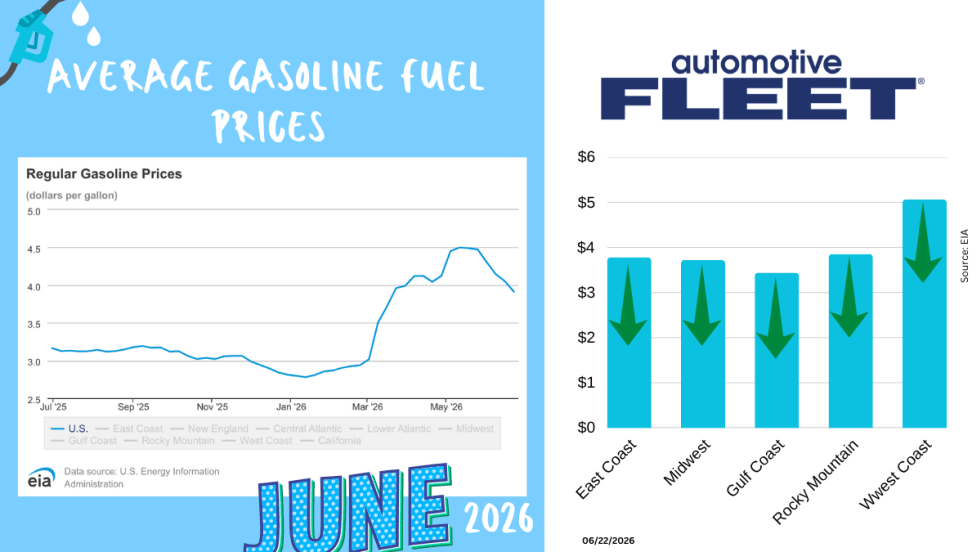

June Fuel Update: Prices Fall Below $4

Drivers are finally getting some relief at the pump. The national average gas price has dropped below $4 a gallon for the first time in months, with prices falling in 47 states as oil markets react to developments in U.S.-Iran negotiations.

Read More →

Study: How 2026's Gas Price Hikes Affect Different Vehicle Types

New data from iSeeCars reveals how rising fuel costs have affected different vehicle segments as gasoline prices climbed nearly 46% over the past four months.

Read More →Are You Tracking Your Fleet's True Total Cost of Ownership?

Bobit Business Media surveyed 190 fleet professionals and found that while most fleets are tracking costs, fragmented systems and data gaps are keeping true TCO visibility out of reach. With rising pressure to control spend in an increasingly volatile environment, the gap between what fleets think they know and what the data actually shows is wider than you might expect. See how your peers are managing costs today and where the industry still has room to improve.

Read More →

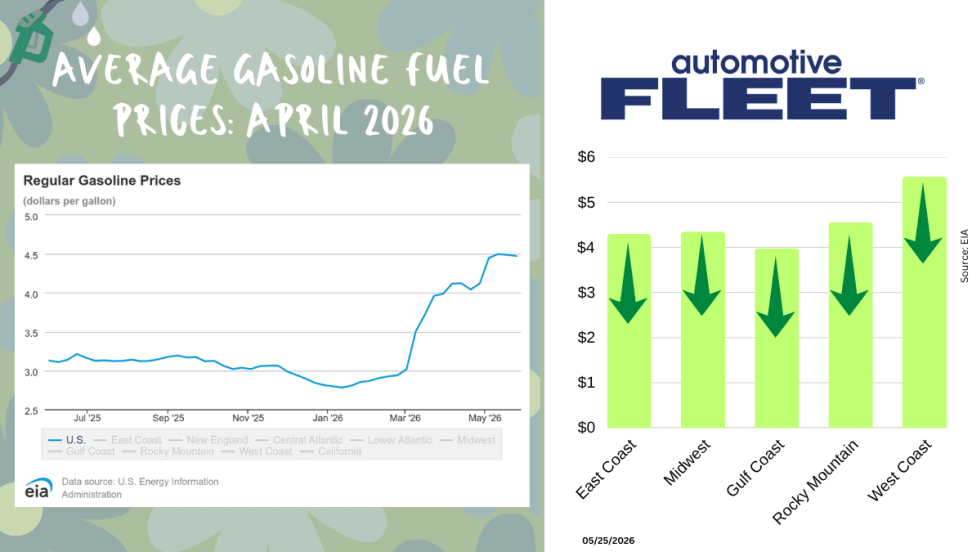

May Fuel Update: All Regions Experience Declines

Gas prices are finally easing in much of the country, but experts warn global tensions could quickly reverse the trend as the national average remains well above last month’s levels.

Read More →