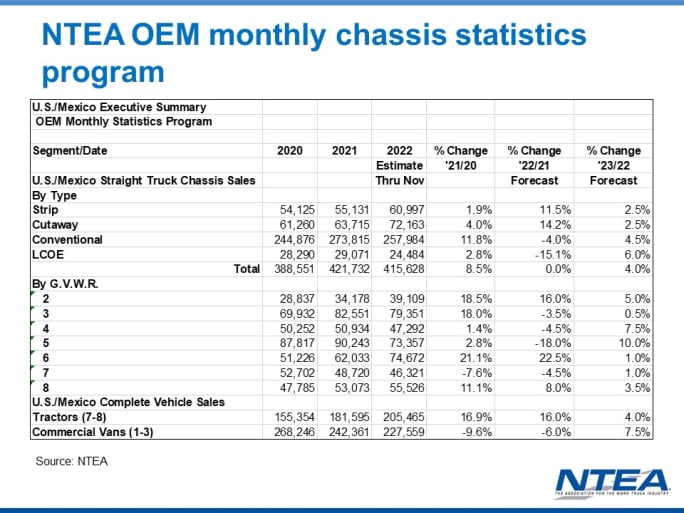

NTEA’s OEM monthly chassis sales outlook is currently expecting 2022 to be flat overall compared to 2021. The forecast for 2023 calls for sales to grow by roughly 4% overall, with slow growth through 2026.

Photo: Canva

7 min to read

Leading indicators around GDP, residential investment, unemployment rate, personal expenditures, and the consumer price index are pointing to a recession in the U.S. this year — but how severe and long-lasting will it be? And how will these factors affect the commercial truck and equipment industry market?

A discussion of these issues formed the basis of the webinar “Understanding Market Dynamics Influencing the Work Truck Industry in 2023,” presented by NTEA’s economist Steve Latin-Kasper on Jan. 11.

Ad Loading...

Here are the key takeaways.

GDP Will Go Negative, But When?

Last year was characterized by unexpectedly strong GDP growth in the third quarter. The fourth quarter of 2022 is expected to show slower GDP growth, said Latin-Kasper, senior director of market data and research for NTEA, the association for the work truck industry.

Moving into 2023, there is consensus that at some point GDP will go flat to slightly negative versus 2022, though the timing is in question — some say the first two quarters, while others are pushing the recession further out.

Nonetheless, growth is expected in the other quarters, so that for 2023 overall, GDP will be on par or slightly above 2022 numbers.

Labor Market Will Remain Tight

Latin-Kasper made the point that the U.S. was already heading into a recession in Q4 2019 before the pandemic hit. He referenced how unemployment insurance claims data fluctuated in tandem in both Q4 2019 and Q4 2022.

Ad Loading...

“(This) tells us that from a labor market perspective, we’re back to what we were feeling in the fourth quarter of 2019,” he said. “Pre-pandemic, we were already experiencing the problems that are associated with a tight labor market.”

Unemployment claims stand at about 3.7%, as of the webinar date. That’s at, or actually below the full employment rate, he said. Claims are expected to rise, but not by much.

Inflation Softening, But Interest Rates Stay High

The unemployment rate has an inverse effect on inflation: When unemployment goes up, inflation goes down and vice versa.

The rate of inflation peaked at just over 9% near the end of Q2 2022 and has been falling since. (The inflation rate fell for the sixth straight month in December to 6.5% on an annual basis.)

This is good news, but not yet good enough to move the needle on interest rates. The Federal Reserve won’t back off potential interest rate increases until inflation decreases to the Fed’s target rate of 2% to 3%. This likely won’t happen until at least halfway through 2023 or into the third quarter, Latin-Kasper said.

Ad Loading...

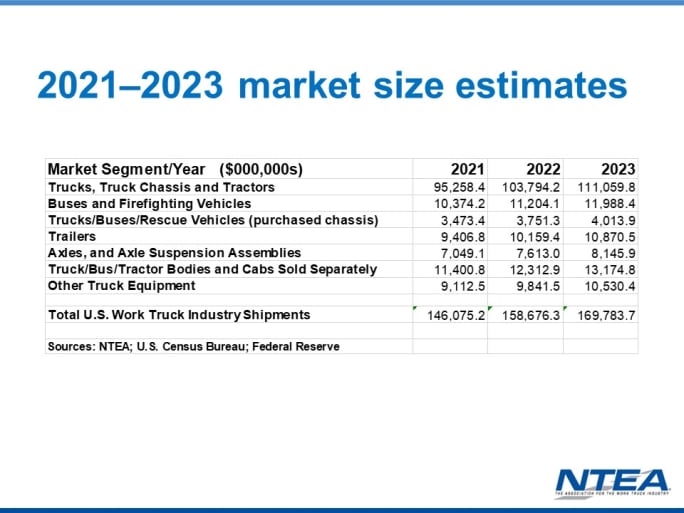

In financial terms, and not adjusted for inflation, the U.S. work truck industry is expected to add another $10 billion to the market in 2023. However, only about 4% of that will be unit growth, with the rest due to inflation.

Image: NTEA

Truck Market Grew, but Inflation Drove Gains

Looking at the commercial truck and equipment industry market valuation in terms of dollars, Latin-Kasper showed that the market increased from $146 billion in shipments in 2021 to about $158.6 billion in 2022 and is expected to increase to almost $170 billion for 2023. This growth is predominantly based on higher vehicle prices driven by inflation, however.

On a unit basis, 2022 is expected to end the year flat compared to 2021. While 2023 will add another $10 billion to the market, only about 4% of that will be unit growth, with the rest due to inflation.

Truck Sales Trending Up, Vans Lagging

Monthly OEM sales and shipment data show positive recent trends, though it varies by class groups.

Class 2 to Class 5 experienced yo-yo swings before the pandemic, and then the pandemic produced even greater troughs and peaks. Shipments in 2 to 5 have been trending positive since Q1 2022. Looking at the annual percentage change baseline, Latin-Kasper expects 2 to 5 sales and shipments to cross into positive territory in Q2 2023.

Sales data for Class 6 to Class 8 shows a similar slide pre-pandemic, but a more dramatic drop in 2020 and a more immediate recovery. When supply chain disruptions kicked in, Classes 6 to 8 never dipped below the baseline. Latin-Kasper expects 2022 to end essentially flat relative to 2021 with continued growth in this segment through 2023, followed by a tapering off of sales and shipments.

Ad Loading...

The commercial van segment was more acutely affected by the lack of availability of semiconductors and parts, as the situation forced OEMs to park tens of thousands of vans. As parts became available, shipments came out in chunks.

Van sales and shipments have been trending up since the beginning of 2022, but the key trend is that demand is still well ahead of supply. Therefore, the van segment isn’t expected to reach the pre-pandemic sales baseline of 30,000 units per month for a few years.

Regarding sales and shipments overall, “The good news is that we’re coming off the bottom,” Latin-Kasper said. “Sales and shipments are headed back up in the right direction.”

Commodities Prices a Mixed Bag

Latin-Kasper demonstrated price movements of various commodities, including diesel, steel, and housing.

Diesel prices spiked dramatically in 2022 and have only recently tapered slightly. The price increases for freight have not kept up with diesel, which have squeezed carriers’ profit margins.

Ad Loading...

This squeeze normally would make carriers think twice about buying new tractors, but demand is so far ahead of supply — and will remain so through 2023 — that this dynamic isn’t as impactful as it would be otherwise.

Steel prices — a good indicator of how consumer prices are likely to move — have been on a downward trend, though with an upward blip due to the Russian-Ukrainian war. Prices are expected to dip to 2018-2019 averages by mid-2023.

Housing starts have already fallen steeply and will trough in 2023 as rising interest rates dampen first-time homebuyer’s ability to get into the market. Recovery will happen toward the end of the year.

However, the multifamily unit market is holding up fairly well, as those structures are needed for the underserved rental market, Latin-Kasper said.

NTEA is predicting a slight increase in chassis sales for the 2023 calendar year, with the commercial van, low cab forward, and conventional segments experiencing the most growth over 2022. However, the van segment isn’t expected to return to pre-pandemic sales numbers for a few years.

Image: NTEA

Minor Growth in Chassis Sales for 2023

NTEA’s OEM monthly chassis sales outlook is currently expecting 2022 to be flat overall compared to 2021. Looking at sales by chassis segment, the big growth winners in 2022 were strip and cutaway chassis (11.5% and 14.2% vs. 2021), along with Class 8 tractors (11.1%). Commercial vans (-9.6%) were particularly negatively affected.

Ad Loading...

The forecast for 2023 calls for sales to grow by roughly 4% overall. Growth is expected to slow to 2.5% and 4.5% in the strip and cutaway segments, while the conventional and cabover segments (6% and 4%) will pick up the pace.

Supply chain improvements will have an outsized positive effect on the commercial van segment in 2023, with 7.5% growth expected. (Noting again that van sales will take much longer to normalize.) The fastest growing weight class segments for 2023 will be Classes 4 and 5, followed by Classes 2 and then 8.

In terms of a longer view of new commercial truck registrations, expect slow growth through 2026.

High Demand Outweighs the Negatives

Latin-Kasper presented how consensus outlooks on leading indicators have changed from six months ago. Updated forecasts from various sources such as the National Association for Business Economics (NABE) have trended negative since then.

For instance, NABE’s outlook in June 2022 predicted GDP growth of 2.1% in 2023. The updated forecast predicts 0.3% growth.

Ad Loading...

However, the sky isn’t falling, as the market is rife with mitigating factors: Inflation is past the peak and on a downward slope, though we expect to be in a rising interest rate environment through at least the third quarter of this year.

While the growth rates of consumer and capital expenditures are likely to slow, they won’t go negative.

Unemployment remains uncharacteristically low, which is a hedge against a full-blown recession. However, labor market imbalances remain a long-term problem as fewer people enter the workforce and Baby Boomers retire.

As China is a major OEM supplier, plant closures due to Covid could have a negative effect, but it’s a low probability right now. Political uncertainty with the Russia-Ukraine war is still a question mark.

Latin-Kasper concluded by reasserting that the coming recession will be shallow and short-lived. The growth quarters in 2023 will outweigh the negative quarters, which will produce a slightly positive comparison overall to 2022.

Ad Loading...

“(This is) hopefully the final part of the rebalancing act that we've been engaged in since the pandemic hit back in March 2020,” he said.

Most importantly, fleet demand is still well ahead of supply. Chassis availability is a negative, though recovering. “Supply chains are improving, but more slowly than any of us would like,” Latin-Kasper said.

Bobit Business Media surveyed 190 fleet professionals and found that while most fleets are tracking costs, fragmented systems and data gaps are keeping true TCO visibility out of reach. With rising pressure to control spend in an increasingly volatile environment, the gap between what fleets think they know and what the data actually shows is wider than you might expect. See how your peers are managing costs today and where the industry still has room to improve.

Mark Hogland discusses Union Leasing’s transition to Moventum Fleet Management and how the rebrand reflects the company’s growing focus on strategic fleet management and lifecycle support.

Departmentally assigned vehicles often create hidden costs through underutilization, poor visibility, and increased administrative burden. This white paper explores how shared motor pool strategies help fleets reduce costs, improve accountability, and optimize vehicle utilization.

Updated DMV rules open the door for heavy-duty AV testing and deployment while strengthening safety standards, emergency response coordination, and manufacturer accountability.

Fleet leaders are under pressure to reduce costs, adapt to economic uncertainty, and make smarter decisions. See how peers across North America are responding with real data, proven strategies, and forward-looking insights. Download the 2026 Market Pulse Report to benchmark your strategy and uncover where you can gain an edge.