History of Fleet Leasing

Open-end (or finance) leasing was developed in 1951. Fleets wanted to lease units with off-balance sheet reporting. In 1981, the landmark Swift Dodge vs. IRS court decision legitimized the use of open-end TRAC leases.

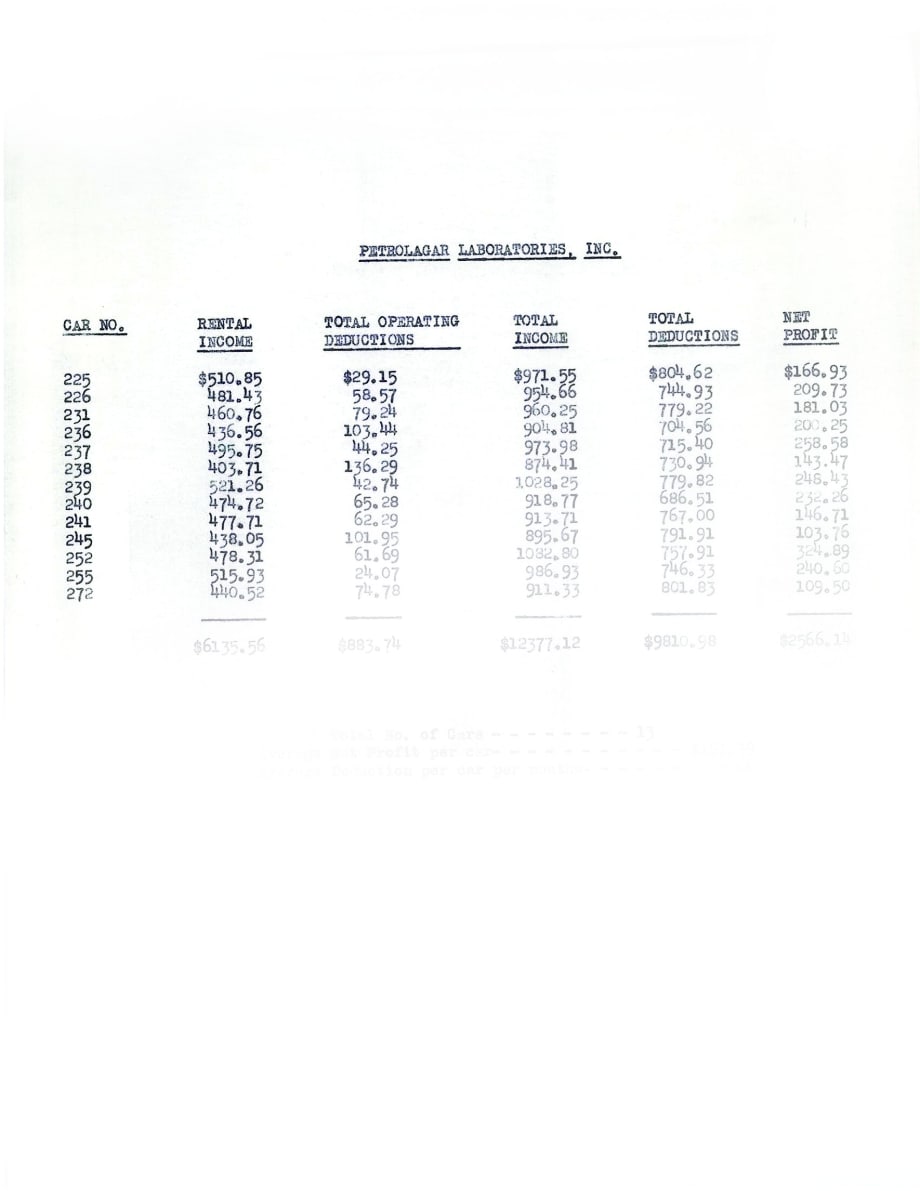

Pictured (to the left) is a reproduction of an actual billing document, circa 1941, for Wheels’ first client, Petrolager, which was ultimately purchased by Wyeth, then Pfizer, and is still its client today. The leases of 1941 were closed-end, full maintenance for 12-month terms. Note, the average rental was just over $40 per month.

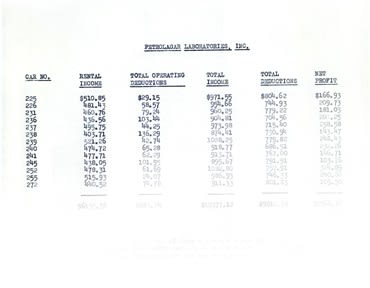

Pictured (to the left) is a reproduction of an actual billing document, circa 1941, for Wheels’ first client, Petrolager, which was ultimately purchased by Wyeth, then Pfizer, and is still its client today. The leases of 1941 were closed-end, full maintenance for 12-month terms. Note, the average rental was just over $40 per month.

Fleet leasing as a way to fund company vehicles originated in the late 1930s. Early lessors offering full maintenance closed-end leases were R.A. Company, established by David, Harry, and Nathan Robinson; and Four Wheels, founded by Zollie Frank and Armund Schoen in 1938. At that time, Frank commenced long-term fleet leasing of automobiles and is generally credited with being the originator of fleet leasing. However, it wasn’t until the late 1940s that significant automobile leasing began on both an individual and fleet basis. During this period, fleets funded vehicles using a closed-end lease, which ran for a fixed term, with the residual risk assumed by the lessor.

Changing conditions in the 1950s led to the development of open-end (or finance) leasing, which PHH offered in 1951. Fleets wanted the ability to replace units after a 12-month period with off-balance sheet reporting.

Changing Business Conditions

In 1954, U.S. Leasing Corp. was the first company to offer general equipment leasing. The leases were net leases, in which the lessee paid all the expenses of maintenance, insurance, and taxes associated with equipment ownership. U.S. Leasing Corp., along with Boothe Leasing, Chandler Leasing, GECC, Commercial Credit Corp., and National Equipment Leasing Corp. were the pioneers in equipment leasing.

A major milestone in the history of leasing occurred in the late 1960s with the development of modern leveraged lease structures, where the lessor provides a portion of the purchase price of the asset and the remainder is borrowed from institutional lenders on a non-recourse basis. The lessor would claim the Investment Tax Credit (ITC) and depreciation tax benefits on 100 percent of the purchase price of the leased equipment, with the lessee benefiting in the form of a lower monthly lease payment reflecting the economic tax benefits claimed by the lessor. Tax-oriented leasing suffered some setbacks in the 1960s when the U.S. Congress first suspended the ITC in 1966, then reinstated it in 1967, and again repealed it in 1969, before reenacting it in 1971, and repealing it in 1986.

Until the 1970s, leasing remained something of a novelty, since most non-transportation companies still did not utilize leasing, except for short-term operating leases of computers and office copiers. Since leasing competed with conventional sources of financing, such as loans offered by banks and insurance companies, those financial institutions often discouraged their non-transportation customers from using leases. At this time, equipment leasing was still regarded as “last resort financing.” In the 1980s, the leasing industry was subjected to numerous tax, legal, and regulatory changes.

IRS Loses Swift Dodge Case

One of the most significant developments in the history of fleet leasing was the creation of the open-end lease using the Terminal Rental Adjustment Clause (TRAC).

However, the IRS contended that under an open-end TRAC lease, some of the risks and benefits of ownership were transferred to the lessee, since the lessee was responsible, in part, for the residual balance on the unit at term’s end. Because of this, the IRS said an open-end contract was not a true lease, but rather a conditional sales contract disguised as a lease. The IRS concluded that, since it was a conditional sales contract, the lessor was not entitled to the ITC on the transaction.

But, the IRS lost the landmark court case in 1981, known as Swift Dodge vs. IRS, in which the court legitimized the use of the open-end TRAC lease.

Using precedents established in two other cases (Northwest Acceptance and Lockhart Leasing), the IRS agreed with Swift Dodge’s contention that the agreements were leases and that they were entitled to ITC, and were not conditional sales contracts.

More Leasing

Mike Albert Fleet Solutions Names Marty Kuhn CEO, First from Outside the Family

Kuhn has a theory of what sets the company apart from larger FMCs: depth of partnership over breadth of volume.

Read More →

Union Leasing Rebrands as Moventum Fleet Management

The name Moventum reflects the company’s position at the intersection of movement and momentum, with the guiding principle "Keep Work Moving."

Read More →

How Does a Mid-Major FMC Compete? Ask BBL Fleet

This Pittsburgh-based FMC built a technology-first culture, sustained double-digit organic growth, and expanded its Midwest footprint through a recent acquisition. How did it happen?

Read More →

What’s Really Happening in Fleet Supply Right Now

Fleet supply has improved, but not everywhere. Merchants Fleet’s Charles Matthew explains where constraints still exist, what risks are emerging, and why fleets shouldn’t wait to place orders.

Read More →

These Edges Are Measured in Inches — Matt Dyer on Fleet’s New Normal

The Merchants Fleet CEO contends that fleets that drive the business win the inches. In 2026, every one of them counts.

Read More →

Who Gets a Company Car? (In 2026 and Beyond)

As costs rise and scrutiny increases, fleets are refining criteria that govern eligibility for company-owned vehicles.

Read More →

DriveItAway Holdings, Free2move Launch Operations In Nine Cities

The co-branded program with Stellantis’ mobility division scales up leasing and financing options nationwide with more cities to come online in 2026.

Read More →

AFLA 2025 Conference in Pictures

Drawing over 640 attendees, the 2025 AFLA Annual Conference was held Sept. 14-17 at the JW Marriott Marco Island Beach Resort in Florida.

Read More →

DriveItAway, Free2move Partner to Expand Vehicle Access for Dealers

The arrangement enables franchise dealers to offer flexible lease-to-own programs with no credit checks, no down payments, and no long-term commitments.

Read More →

New Survey: How Well Are FMCs Serving Fleets? We Want Your Input

Fleet managers: Share your experience to help benchmark fleet management companies’ service, strategy, and support.

Read More →