More News: Used Vehicle Sales, Inventory Climb

Wholesale Used Vehicle Prices Ease Down

Wholesale values remain elevated against normal depreciation trends, even with declines in September, and right as tax incentives on EVs end.

October 7, 2025

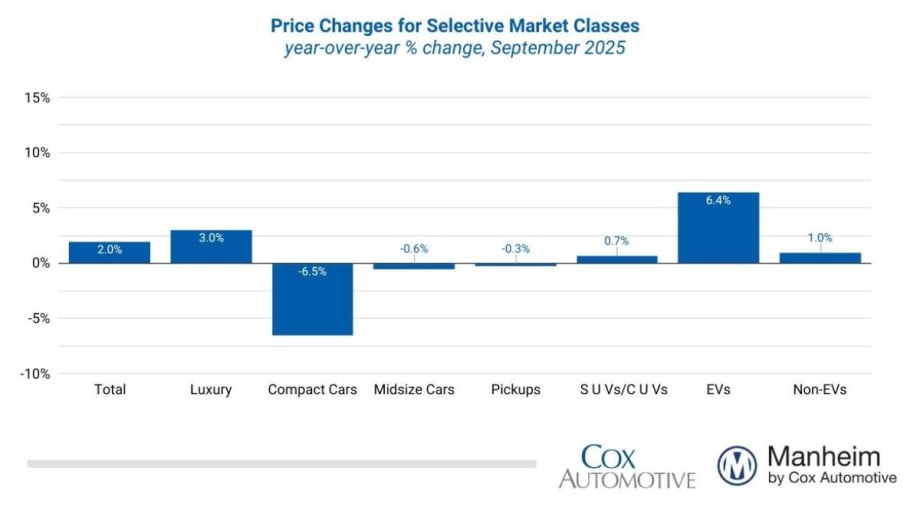

Major market segments remain mixed for seasonally adjusted prices year-over-year in September.

Graphic: Cox Automotive

6 min to read

Wholesale used-vehicle prices (on a mix, mileage, and seasonally adjusted basis) were down slightly in September compared to August, according to the latest Manheim Used Vehicle Value Index (MUVVI) numbers released Oct. 7.

The index declined to 207, 0.2% lower than August levels but showing a 2% increase from a year ago. The seasonal adjustment caused the index to decrease for the month, as non-seasonally adjusted values moved slightly higher in September. The non-adjusted price in September increased just 0.1% compared to August, moving the unadjusted average price higher by 2.1% year over year. The long-term trend, on average, for non-seasonally adjusted values is a decline of 0.3% per month, demonstrating that the unadjusted depreciation trends in September were less pronounced than normally seen.

“As we close the books on Q3, we’ve continued to see wholesale values remain elevated against normal depreciation trends, even with declines in September and right as tax incentives on EVs come to an end,” said Jeremy Robb, deputy chief economist for Cox Automotive, in a news release. “Both new and used retail sales were fairly elevated over most of Q3, but we started to see some declines in the last few weeks of September. Simultaneously, we observed that weekly wholesale valuations declined a bit more than earlier in the month, as the relationship between supply on dealer lots and wholesale values remains strongly intertwined.”

In September, Manheim Market Report (MMR) values declined in September, with smaller declines early in the month and a larger drop in the final week. Over the last four weeks, the Three-Year-Old Index decreased by an aggregate of 1.6%, which is slightly more than the usual decline. Those same weeks delivered an average decrease of 1.5% between 2014 and 2019, indicating depreciation trends were just one-tenth of a point higher than the historical average for the month. Depreciation trends for 3-year-old MMR values were higher than last year as well, with a decline of 1.1% observed in September 2024, following a stronger Q3 and off-lease maturities that fell sharply.

Throughout the month, the daily MMR Retention, which represents the average difference in price relative to the current MMR, averaged 99%. This indicates that market prices moved further below MMR values and were 0.8% lower than August levels. Compared to last year, valuation models were down 0.3% for MMR retention and were lower than in other years for the month, except in 2022.

The average daily sales conversion rate also declined to 58.3%, a 2.7 percentage point decrease from last month, but is generally higher than typically seen at this time of year. For comparison, the daily sales conversion rate averaged 57% in September over the last two years, indicating stronger-than-average sales conversion for this time of year and suggesting a more favorable market for sellers.

Luxury Vehicle, EV Sales Strongest

Major market segments remain mixed for seasonally adjusted prices year-over-year in September. Compared to the same month last year, the luxury segment continues to be up the most, as it is influenced by trends in the electric vehicle (EV) segment, and it was higher by 2.3%, with SUVs increasing by 0.7% over the last year, though below the industry average seasonally adjusted price change of 2%. Also falling below the industry average, trucks were down by just 0.3%, while mid-size sedans declined 0.6%, and compact cars fell the most, down 6.5% compared to last year.

Major market segments were also mixed compared to the previous month, with mid-sized sedans showing the only gain month over month, higher by 0.2%. The luxury segment was down by 0.3%, pickups fell by 0.5%, and SUVs declined by 0.9%. The compact car segment declined the most, down 2% compared to August.

Examining the market by powertrain, electric vehicle values continue to show larger gains against last year's levels than the market overall, as EV sales remained elevated over the quarter, driven by the impending expiration of tax credits, which has led to higher levels of consumer demand.

Robb noted, “Consumers kept the pace of new and used EV purchases high over the quarter, prior to the expiration of the tax incentive. This heightened demand pushed EV wholesale values higher again this month, making EVs the strongest-performing segment in year-over-year value appreciation.”

EV values have shown higher year-over-year appreciation trends for six consecutive months and were 6.4% higher than the same month in 2024, while non-EVs rose by 1%. For September results against the prior month, EV values rose by 0.8% month over month, while non-EVs declined by 1%.

Retail Used-Vehicle Sales Were Down in September

Assessing retail vehicle sales based on observed changes in units tracked by vAuto, initial estimates of retail used-vehicle sales in September were down 3.9% compared to August and down by 2% year over year. The average retail listing price for a used vehicle increased 1.5% over the last four weeks.

Using estimates of retail used days’ supply based on vAuto data, an initial assessment indicates that September ended at a 46-day supply, up two days from 44 days at the end of August and up one day from September 2024, at 43 days.

New-vehicle sales in September increased 6.7% from the same period last year, but volume decreased from August, dropping 14.2%. However, this decline was offset by a continued strong pace of new-vehicle sales. The September sales pace, or seasonally adjusted annual rate (SAAR), came in at 16.4 million, up 600,000 from last year’s pace and even with the very strong 16.4 million level in August.

Combined sales into large rental, commercial, and government fleets rose again, up nearly 12% year over year in September, led by gains in the rental and government sectors. Including an estimate for fleet deliveries into dealer and manufacturer channels, the remaining retail sales were estimated to be up 6.8% from last year, leading to an estimated retail SAAR of 13.4 million, up slightly from 13.4 million last September but down from August’s estimated 13.7 million level. Fleet share in September was estimated to be 15.5%, unchanged from last year.

Rental Risk Price and Mileage Results Are Mixed Against Last September

The average price for rental risk units sold at auction in September increased by 2% year-over-year. However, rental risk prices were down by 2.7% compared to August. Average mileage for rental risk units in September (at 47,100 miles) declined by 10.5% for the month against last year’s level and was also lower against the August comparison, falling by 4.5% over the month.

All Measures of Consumer Confidence Declined in September

The Conference Board Consumer Confidence Index decreased 3.7% in September and was worse than expected. Consumers’ views of both the present and the future declined, but the present situation declined the most. Consumer confidence was down 5% year over year. Plans to purchase a vehicle within the next six months decreased and were lower year-over-year.

The University of Michigan's sentiment index decreased 5.3% in September to 55.1, which was slightly lower than expected and marked a decrease from the earlier reading at the beginning of the month. The index was down 21.4% year-over-year. The underlying views of both current conditions and future expectations declined, with future expectations falling the most. Expectations for inflation over the next year decreased to 4.7% from 4.8%, but expectations for inflation over the next five years increased to 3.7% from 3.5%. Consumers’ views of buying conditions for vehicles declined slightly to the lowest level in four months as views of prices deteriorated.

The daily index of consumer sentiment from Morning Consult decreased 3.3% in September, resulting in a modest year-over-year increase of 0.4%.

According to AAA, the national average price for unleaded gas decreased 3 cents in September from the end of August to $3.16 per gallon, which was down 1% year over year but up 3.2% year to date.

More Remarketing

Manheim Index Shows Used-Vehicle Wholesale Prices Up 2.1% in June

The market is seeing stronger appreciation in older used vehicles this year, and the most affordable segments have been among the year’s best performers.

Read More →

Commercial Fleet Sales Contribute To June, YTD Gains

The fleet sector has boosted its vehicle purchases at a reliable pace in the first half of this year compared with 1H 2025.

Read More →

Used Vehicle Prices Climb Higher As Sales Pace Slows

The higher prices at used retail reflect strong wholesale values earlier in the spring, particularly for older, more affordable vehicles.

Read More →

Wholesale Used Vehicle Market Sustains Moderate Rise In Values, Prices

Trends continue to normalize after a strong start to the year, as consumers contend with higher gas prices in the coming summer months.

Read More →

Commercial Fleet Sales Still Lead Sectors Despite May Mini Dip

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

How Connected Vehicle Data Is Lifting Fleet Resale Values

A vehicle health score could improve the value of fleet vehicles at remarketing. The path to a universal standard is forming, and fleets that understand the process early will be better positioned when it arrives.

Read More →

Wholesale Used Vehicle Prices Slightly Up In April

The Iranian conflict and rising gas prices inject much uncertainty into the future wholesale used vehicle markets, as higher gas prices soak up spendable income from vehicle buyers.

Read More →

CAR2026: James McKinley Wins Value Champion of the Year

James McKinley of City Rent a Truck was named the inaugural Fleet Value Champion at the CAR Conference for his data-driven approach to fleet lifecycle management and vehicle remarketing.

Read More →

CAR2026: Eric Autenrieth Wins Remarketer of the Year

Eric Autenrieth was recognized at this year's CAR Conference as the Remarketer of the Year.

Read More →

CAR2026: Lawrence Knapp Wins Consignor of the Year

Lawrence Knapp won the Cosigner of the Year award at this year's CAR Conference.

Read More →