High-Mileage Used Fleet Vehicles Create Difficulties Financing 'C' and 'D' Paper Buyers

Fleet managers are manufacturers of used vehicles. Many of the buyers of used fleet vehicles are C and D paper buyers. One unintended consequence to companies extending the service lives of fleet vehicles is that it is more difficult for used-vehicle dealers to finance C and D paper buyers in the secondary funding market. The issue, from the perspective of the finance company, is the remaining life of higher-mileage vehicles.

Fleet managers are manufacturers of used vehicles. Many of the buyers of used fleet vehicles are C and D paper buyers. One unintended consequence to companies extending the service lives of fleet vehicles is that it is more difficult for used-vehicle dealers to finance C and D paper buyers in the secondary funding market. The issue is not interest rates. Whether these buyers purchase an identical vehicle with 60,000 or 120,000 miles, they will pay the same interest rate. The issue, from the perspective of the finance company, is the remaining life of higher-mileage vehicles.

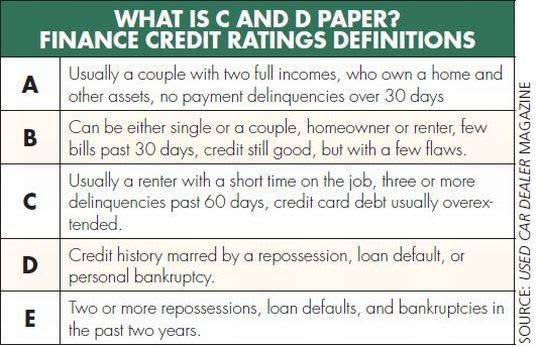

Consumers are ranked as either A, B, C, D, or E paper buyers. Consumers who have either A or B credit ratings typically do not have difficulty getting a loan. “The reason someone is in a C or D paper category is because they probably haven’t paid their bills on time or have a personal bankruptcy,” said Kevin McGrath, president of Fleet Street Remarketing, a remarketing company headquartered in Largo, Fla. “When a finance company assesses a vehicle these buyers want to purchase, they determine the vehicle’s remaining life. The reason this is important is because when a vehicle stops running, experience shows these buyers typically stop paying. The finance company only wants to fund a vehicle that will last the length of the loan or at least 80 percent of the loan length, because this is typically the length of time needed to get its money back in profit.”

A typical loan is three years for a C or D paper buyer, typically at 20 percent plus interest. If a driver averages 12,000 miles per year, the finance company wants the vehicle to be able to run at least an additional 28,000 miles, or 80 percent of the loan period. However, this rule of thumb will vary by vehicle make and model. Often, secondary finance companies are a little more flexible in funding import-badged models.

“There are some makes and models these secondary funding companies will not fund, such as those with a reputation of being prone to maintenance issues at higher miles,” said McGrath. “I am getting turned down by banks saying they’re not going to fund a car with this much mileage.’”

Secondary finance companies are funded by other financial institutions, such as GE or Chase, using credit lines. These financial institutions have become more restrictive in the credit lines they provide secondary finance companies. During the recent recession, many secondary funders had their credit lines pulled and went out of business, especially those carrying a high volume of bad loans. This decreased pool of secondary funders also contributes to the difficulty in funding C and D paper buyers.

Not only do high-mileage vehicles limit the number of retail buyers, they also shrink the pool of dealer buyers at the auction.

“Once a sedan gets over 100,000 miles, it limits the number of buyers to whom you can sell the vehicle. At this point, the vehicle is primarily of interest to buy-here, pay-here dealers who aren’t as willing to buy as much at auction,” said McGrath.

The negative impact of high-mileage vehicles is especially pronounced with commercial vehicles, such as work trucks and cargo vans. “I get cars from fleet managers who are running their cars to 125,000-130,000. Vans go up to 200,000 miles. These aren’t small fleets either. These are big-time, well-recognized fleets,” said McGrath.

Finance companies are especially tight-fisted when it comes to funding work truck fleets for C and D paper buyers. “The only buyers they are funding are A and B paper customers. C and D paper customers will have to pay cash for these vehicles,” said McGrath.

Tradesmen, who want to buy a used van that may be newer than what they are driving, are having a difficult time securing funding to acquire these vehicles. “It is very difficult for these buyers. If you are a C or D paper customer looking to buy 2005 or 2006 model vans with 135,000 miles, then you will most likely be forced to pay cash,” said McGrath.

In a soft economy, senior management demands expense reductions and institutes limits on capital expenditures. As a result, there is pressure to defer vehicle replacements. As seen, extending fleet vehicle replacement parameters can prove to be counterproductive to the intended goal, especially with resale value. One unintended consequence to remarketing higher mileage vehicles is “manufacturing” a product that is difficult to finance.

Let me know what you think.

mike.antich@bobit.com

More Blog Posts

Fleets Want Trust Restored with Suppliers

During this period of ongoing supply constraints, the trust that fleet managers had with OEMs, upfitters, and dealers has been strained. Fleet managers say they have had too many experiences over the past three years coping with erroneous information, adjusting to multiple price increases, and feeling betrayed by inadequate transparency from suppliers.

Read More →

Scheduled Replacement Cycles Are Becoming a Distant Memory

The ongoing difficulty in sourcing replacement vehicles is forcing companies to extend the service lives of vehicles that are unable to be replaced, which, inevitably, increases unscheduled maintenance expenses.

Read More →

Fleet Simplification is the Antidote to Asset Variability

Fleet simplification identifies asset functions to uncover commonality among the equipment and assets. Simplification increases operational efficiency as end-users become accustomed to the controls, displays, and operation of less diverse units.

Read More →

The Dangers of Static Fleet Policies

A fleet policy is a living document, flexible enough to adapt to evolving business priorities, developing industry trends, and changing industry best practices and standards.

Read More →

Short-Term vs. Long-Term Cost Reductions

Corporate procurement staff are often driven by short-term, immediate cost reductions. However, a longer perspective to soft cost savings is critical because fixating on short-term results will hurt a company in the long run.

Read More →

Uptick in Unscheduled Maintenance Increasing Vehicle Downtime

Fleet data analysis can identify recurring downtime issues. It’s important to determine the root causes of downtime so procedures can be developed to minimize such problems.

Read More →

Eliminate Needless Curb Weight to Maximize ICE & EV Efficiencies

Vehicle weight relates directly to fuel economy. In today’s era of electrification, there is also a direct correlation between vehicle weight and battery range.

Read More →

Tech Dependence Risks Dumbing Down Fleet Manager Expertise

The line between creative thinking and problem solving and doing what the data indicates is thin. To lead in fleet management, you need to balance understanding the fundamentals and embracing what smart technology offers.

Read More →

Leverage the Synergy of Safe Driving to Achieve Sustainability and Cost Goals

Safe driving, emission reductions, and cost containment can all be achieved at the same time.

Read More →

The Playbook for Fleet Manager Success

There are many paths to success — most of them involve being flexible, open-minded, and willing to learn.

Read More →