Depreciation Decreases in 2011

Depreciation expenses decreased in 2011 versus prior years due to such factors as higher vehicle resale values and the ongoing shortage of available used vehicles.

In comparing depreciation by vehicle segment in 2011 versus 2010, the overall consensus is that resale values are up.

“In 2011, we are seeing the overall vehicle segment is up year-over-year roughly 10 percent,” said Steve Jastrow, strategic consulting services manager for GE Capital Fleet Services. “Compact cars and intermediate cars lead the way with roughly 20 percent and approximately 15-percent respective inflation factor over last year. Minivans rose at just under 9 percent and full-size vans at just under 10 percent over 2010. SUVs saw a 7.5-percent increase; however, there is a split between small SUVs at 10 percent and mid-size SUVs at 5 percent. Light trucks are nearly flat at a 1-percent inflation increase over last year.”

Bob Graham, vice president, vehicle remarketing for Automotive Resources International (ARI), agrees. “Overall, we’ve seen clients recently getting better value for their vehicles on average. Our records show depreciation rates have come down an average of 0.36 percent,” he said.

Reasons behind the increases in vehicle values include the shortage of used vehicles and Japanese imports in the market.

“For the past two years, prices have been supported by a shortage of available used vehicles (low new-vehicle sales and trade-ins) and shortage of Japanese imports due to the March 2011 earthquake. As fuel prices rose to the $4 level earlier this year, small-engine cars drastically inflated in price, but fell back again in the third quarter as fuel prices declined again,” Jastrow said.

The Impact of Replacement Cycling

Short cycling has been one of the “buzz words” of 2011. However, replacement cycling in 2011 did not change appreciably.

“Although LeasePlan USA has observed select cases in 2011 where fleets have shortened cycles (either to capitalize on the current secondary market levels or to return to more ‘acceptable’ terms that were inflated during the recession), the average 2011 cycling duration has only decreased slightly from CY 2009 and 2010 levels,” said Paul Fortin, vice president, asset risk management & analytics for LeasePlan USA.

Graham of ARI noted the economic environment as one factor.

“We’ve not seen a major change from the current rates (average 49 months/94,000 miles) through these three years. Consistently from 2009 through today, companies have held their vehicles longer, in part due to the manufacturer bankruptcies and the poor economic period,” he said.

GE Capital Fleet Services did see a slight adjustment to replacement parameters in 2011.

“We have seen average replacement parameters improve roughly 20 percent over the past year, versus the height of the economic crash in fourth quarter of 2008 through 2009, indicating more vehicles are hitting the secondary market,” said Jastrow of GE Capital Fleet Services. “While these vehicles are seeing very strong resale dollars helping to lower effective depreciation (cap cost less resale price), it is increasing the volume in the secondary market which will ultimately start to lower resale dollars, although we have not seen this increased volume impact the resale dollars to date.”

Strong Resale Market Reduces Depreciation

“The strong resale market has reduced the average depreciation rate — from 1.52 to 1.16, based on our experience,” said Graham of ARI.

Jastrow of GE Capital Fleet Services agreed. “The robust resale market has helped lower effective depreciation,” he said.

One segment impacted by the decline in depreciation costs is the smaller vehicle segment.

“With the market reaching new highs in 2011, depreciation costs have measurably declined. The smaller, more fuel-efficient segments have experienced the greatest depreciation cost decline (all other factors being equal) due to the increased demand in the market due to higher fuel prices,” said Fortin of LeasePlan USA. “But, in general, all segments have experienced a decrease in depreciation due to the improved secondary market demand in conjunction with lower secondary market supply.”

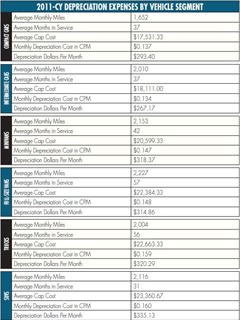

Fleets are consistently keeping vehicles in service longer, across all vehicle segments. SUVs show the highest monthly depreciation dollars per month, consistent year-over-year, and the lowest average months in service.

Acquisition Costs Decrease

For the past three years, there has been a decrease in overall acquisition costs. “For the most part, we attribute the decrease to the current trend for fleets to drive down costs by moving to more fuel-efficient engines (i.e., from six cylinders to four) or model types (from sedan to compact),” said Graham of ARI.

LeasePlan USA has seen an uptick in new-vehicle pricing, which will impact future used-vehicle pricing. “All factors being equal, as new-vehicle pricing increases, used-vehicle pricing will also increase because the retail price that a consumer is willing to pay on a used vehicle is dependent upon new-vehicle pricing at the time of sale,” said Fortin of LeasePlan USA. “On the fleet side, acquisition costs also impact current used-vehicle pricing because fleets tend to migrate toward vehicles with the lowest transaction prices, which will result in more auction supply (and lower prices) at end of term. Generally, both consumer and fleet transaction prices are increasing and subsequently, this trend has a positive impact on current market values, which result in lower depreciation costs.”

As far as capitalized costs are concerned, Jastrow of GE Capital Fleet Services noted, “Increasing cap costs will lower effective depreciation, all things considered.”

Forecasting the Future

Automotive Fleet asked experts to “peer into their crystal balls” and share what they see as future trends in vehicle depreciation.

“Because the secondary market is currently experiencing a supply shortage in many vehicle segments, resulting in historically high pricing levels, it would be safe to assume that when this phenomenon normalizes, the markets will move lower to historical price ranges,” said Fortin of LeasePlan USA. “During the majority of 2011, the secondary market was at historically high levels; as it migrates toward more normalized levels in the near future, depreciation costs will increase in comparison to 2011.”

Graham of ARI is forecasting “more of the same.” He shared, “Looking ahead, we forecast a stronger used-vehicle market, a move to more fuel-efficient vehicles, and low depreciation. We foresee a small rise in depreciation in early 2013 as companies return to more traditional replacement cycles. In 2014, we feel the deprecation percentage will increase when the undersupply of vehicles in the market will be gone. This is when we feel used-vehicle prices will normalize (go down).”

Jastrow of GE Capital Services agreed with Graham. “We anticipate the resale market to continue at near its current level with a tendency for prices to decline slightly. The new-vehicle production 10-year average up to 2007 was roughly 15 million units, in 2009 that dipped to 8.6 million, and to date volume is roughly 13 million. This production dip will keep the number of vehicles in the secondary market depressed, helping support the resale market. Also, there are no leading indications that the U.S. economy will attain strong growth in the next couple of years, thereby reversing the current weak demand for new vehicles,” he predicted.

More Operations

The Top 300 Commercial Fleets

The Top 300 Commercial Fleets: See the List

Read More →

Your Local Dealer Knows More Than You Think

Your local dealer can provide an information advantage that extends well beyond courtesy deliveries.

Read More →

Fleet Meets: Austin Schutte

Here are some industry insights, personal touches, and words of advice from the CEO and Founder of Anew Solutions.

Read More →

Soap Box Derby Challenge: What’s Powering Team Brown

The car is coming together, the students are solving real build problems, and the fleet industry is helping push Team Brown toward the starting line.

Read More →

Commercial Fleet Sales Contribute To June, YTD Gains

The fleet sector has boosted its vehicle purchases at a reliable pace in the first half of this year compared with 1H 2025.

Read More →

What Fleet Managers Really Want From Vendors

From customer service frustrations and technology breakdowns to RFQs, change management, and the growing impact of turnover across the industry, this conversation pulls back the curtain on the real operational challenges fleet managers are navigating every day.

Read More →

Fleet Safety Masterclass: Industry Leaders on Storytelling, Strategy & Innovation

In this special masterclass episode, industry leaders break down what it really takes to build safer fleets in today’s increasingly distracted and data-driven world.

Read More →

Integrating Legacy Fleet Systems and Historical Data

In this episode, we bring together fleet and technology leaders to unpack the realities of data integration, system migrations, and the evolving role of AI in fleet management.

Read More →

From Resistance to Results: Change Management Strategies for Fleets

From new technologies and safety programs to evolving regulations, fleets are under constant pressure to adapt. But as Dr. Betz explains, success isn’t about the system you implement—it’s about whether your people actually use it.

Read More →