View Data Driven Fleet Experience Keynote:

State of the Commercial Telematics Market

What’s Driving Growth in the Commercial Telematics Market?

While the telematics market is still growing, increasing penetration is slowing growth. What sectors are still hot, and what new trends and services are providing value for fleets? Clem Driscoll shares insights from his latest Mobile Resource Management Systems Market Study.

May 24, 2021

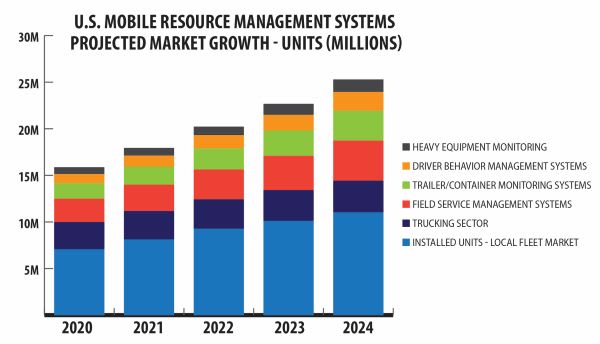

Over 16 million GPS devices are now used to monitor fleet vehicles, drivers, service workers, and assets. Compare this to 13 million in late 2018. By the end of 2022, we should see 20 million units in use.

Data courtesy of Clem Driscoll.

4 min to read

More telematics devices than ever are in use, and more growth is on the horizon — yet only in some sectors, while others are seeing slower growth. Where is this technology’s momentum and how can fleets be prepared?

Telematics expert Clem Driscoll, founder and president of C.J. Driscoll & Associates, discussed this in his keynote address at the Data-Driven Fleet Experience last month.

Expanding on Telematics Terminology

Referencing data from his 2021-22 U.S. Mobile Resource Management (MRM) Systems Market Study — a 300-page report that covers the national MRM market— Driscoll shared which sectors are seeing market penetration, how providers are positioned for growth, new service offerings and partnerships, and more.

First things first: Driscoll clarified that he finds the term “commercial telematics” too narrow. He prefers the term “mobile resource management” as it is broader and includes the management of mobile workers.

Report Highlights

Overall, the U.S. MRM market is still growing rapidly.

More than 700,000 companies are using MRM systems and services today.

Over 16 million GPS devices are now used to monitor fleet vehicles, drivers, service workers, and assets. Compare this to 13 million in late 2018. By the end of 2022, we should see 20 million units in use.

Revenues are projected to grow from $4.6 billion in 2018 to nearly $6.1 billion by 2022. Trucking revenues in particular have doubled over the last seven years due to the ELD mandate.

Telematics & Fleet Market Trends

Telematics market growth continues in most sectors, though increasing penetration is slowing growth. Several suppliers said their replacement sales now equal or exceed new buyer sales. Small and midsized TSPs continue to be acquisition targets for larger players.

Some TSPs, notably Geotab and Fleet Complete, reach customers primarily — or almost exclusively — through authorized resellers. Some resellers have as many as 50,000 to 100,000 units in service, more than many sizable TSPs.

The government fleet market, which has lagged behind other verticals, has become more active in adopting GPS management, though lowest-bid stipulations in RFP requirements are forcing vendor turnover every few years.

As this market matures, mergers and acquisitions are strong. Driscoll provided several examples of recent company acquisitions and partnerships, noting that more are coming.

He believes that as market penetration increases, the path to revenue growth will be through value-added services. Telematics solutions providers (TSPs) must add new features and functions to their systems on an ongoing basis to stay competitive. Some TSPs are developing their own value-added services. Others like Geotab have marketplaces where third-party developers connect their services as add-ons to Geotab’s platform. One company, Roadz, offers a suite of value-added solutions that connects to fleets and TSPs that don’t have their own marketplaces.

Automakers are now getting in on the action. Ford and GM have developed their own commercial telematics solutions, while working with TSP partners for customers who want more features.

Current Issues

While COVID-19 disrupted most everything, its impact was felt less than anticipated in the telematics market. Most TSPs reported that they retained the majority of subscribers. A few segments like public transit and rental cars seem to have been hit the hardest.

Another issue is cellular sunsets. Most GPS installations today operate on 4G LTE, though a few in the field remain on 3G and must be replaced soon. AT&T’s 3G units need to be replaced by February 2022, while Verizon just pushed back their shut down of 3G to January 1, 2023.

The computer chip shortage is also impacting telematics device availability. Driscoll says suppliers do not expect shortages to catch up until Q1 or Q2 in 2022. This was likely driven by COVID, as consumers purchased more electronics, driving up demand.

New Opportunities & Technologies

New features such as video and field service management represent opportunities for incremental revenues. “That’s something that this market has needed,” Driscoll said, “because most of the solution providers have a certain size, or they’re focused on the horizontal market, and there is a lot of overlap. What’s really needed is differentiation.”

The Power of Video & Data

Video has become one of the new ways to provide this difference, and Driscoll said it’s the biggest thing to come along in the local fleet telematics market in a long time.

Cameras have been already deployed in some fleets to determine accident liability where exposure is high: think school buses, police cars, and waste disposal trucks, and now it’s catching on across the board.

Today’s camera technology uses telematics, AI, and computer vision to identify risky behaviors and then collate them into leading indicators such as distracted driving habits that can be acted upon through coaching and real-time in-cab alerts. The goal is to mitigate crashes before they happen.

“Enhanced technology and video systems increases the need for data,” Driscoll commented, pivoting to notes on the use of AI, machine learning and edge computing — technologies that can quickly identify issues impacting driver performance. “These technologies give a richer, fuller picture of what a vehicle is doing,” he said. That’s their main advantage, and that’s why they’re being used.

Subscribe to Our Newsletter

More Fleet Forward

Is Your Grey Fleet Creating an Unmanaged Safety Risk?

NCR Atleos Fleet Manager Jose Rocha will join Cardata and SambaSafety experts at Fleet Forward Conference to examine how fleets can extend safety oversight to every employee who drives for business.

Read More →

Agentic AI Session at FFC Will Help Fleets Turn Data Into TCO Action

Mike Albert Fleet Solutions and Motorq will show how agentic AI can uncover maintenance, fuel, and utilization savings buried across disconnected fleet data.

Read More →

Voting Opens for 2026 Fleet Hall of Fame

See the nominations for the 2026 Hall of Fame and select your choice for this year's class!

Read More →

7 Fleet Professionals Named Finalists for the 2026 Fleet Visionary Award

Meet the 2026 nominees for the Fleet Visionary Award.

Read More →

9 Fleet Leaders Nominated for the 2026 Fleet Manager of the Year Award

Meet the nine finalists for the 2026 Fleet Manager of the Year Award.

Read More →

Fleet Forward Conference to Debut First Registration-Based Analysis of Largest Commercial Fleets

The session will deliver an exclusive first look at registration data covering more than 1.5 million commercial vehicles, offering one of the industry's most detailed views of the private fleet market.

Read More →

Registration Opens for 2026 Fleet Forward Conference

Held on the East Coast for the first time, the Washington, D.C.-area event features expert-led education, a new IIHS Crash Test Experience, and collocation with the NAFA’s Fleet Safety Symposium.

Read More →

Earley, Mossing Named to NAFA's 2026 Class of Fellows

The honor recognizes five outstanding professionals whose leadership, service and contributions have made a significant impact on NAFA and the fleet management profession.

Read More →

Fleet Forward Conference Adds IIHS Crash Test Experience for 2026 Attendees

Attendees will witness a live crash test, tour the IIHS Vehicle Research Center, and experience advanced crash-avoidance technologies firsthand.

Read More →