Truck, van, and utility vehicle segments are showing better retention values than cars, but will they hold through 2013?

by By Ricky Beggs, Black Book USA

March 1, 2013

Even though the first-of-the-year market activity and values have taken a slightly different turn than normally expected, there are plenty of reasons to feel good about 2013.

7 min to read

Even though the first-of-the-year market activity and values have taken a slightly different turn than normally expected, there are plenty of reasons to feel good about 2013.

Take a look in your side- and rear-view mirrors while driving some of the best equipped, comfortable, and fuel-efficient fleet vehicles today, and you get a clear and precise picture of where you have been and who is pushing you along.

You can click any of the photos in this article to see the full series of charts from Black Book.

Ad Loading...

Every day, as the Black Book editors and data analysts are dissecting the remarketing data they receive, they take a look at historical values — the metaphoric rear-view mirror of the industry. Mostly, this is only as far back as yesterday, but seeing value trends of weekly, monthly, quarterly, yearly, and even across multiple years allows them to relate to various market, industry, or world events that brought value reactions at that particular point in time. Those trends can, and should, be great planning tools for every fleet operation.

There are always going to be local and even world issues that will drive the market off the straight course of depreciation. When looking at the historical value trends over the past four to five years, Black Book’s business direction — reporting on the market through wholesale channels in a timely manner, primarily with daily updates — is the only way to provide accurate values for dealers, fleets, fleet management companies (FMCs), lenders, and other industry users.

What’s more important for businesses is to make sure they have the correct data and tools to serve their buying, servicing, and remarketing efforts. Also, having great insight into the issues affecting the market is comforting in today’s economically volatile environment.

Reviewing the 2012 Market

Let’s take a look at how the market reacted in 2012 and a little about what we expect 2013 will throw at us.

Whether it is a retail or fleet vehicle, seasonality plays a factor in retention value for remarketing teams or business partners. The most recent (and normally slow) market, with less aggressive retention of November and December this past year, threw us a curve with an unusually strong market.

Ad Loading...

Each week in December resulted in 31-50 percent of the necessary adjustments being increases to the values. Those are levels that normally would appear in late April or May at the end of a strong spring market. Due to the unusually strong market in November and December, the typical first-of-the-year uptick in vehicle values presented a softer pattern than normal.

The percent of adjustments that were increases during the four weeks of December was a solid 42 percent, whereas the first three weeks of January backed off to only 32 percent. Looking at all adjustments, the average segment change for cars came in at -$48 during December, with a slightly softer market and larger declining level of -$55 for January.

The truck, van, and utility segments retained value better than cars overall, but with December trending at -$15 and a slightly weaker market in January at -$29.

So, even though the first-of-the-year market activity and values have taken a slightly different turn than normally expected, there are plenty of reasons to feel good about the market for all of 2013.

Let’s take a closer look at some of the issues and variables we see within the market. As 2012 brought out much of the retail pent-up demand, new-car sales levels far exceeded expectations. An additional 1.7 million sales over 2011 brought the total to 14.5 million. With the significant increase being sold, this also carries over into the used-sales volume, while also creating additional used inventory in the market.

Ad Loading...

Based on 60 percent of new-car sales having a trade-in, it’s expected that there is an additional 1.1 million in used inventory right now, compared to the first part of 2012 (8.7 million over the 7.6 million trade-ins from 2011) and a whopping 2.5 million more than the low sales levels of 10.3 million in 2009 (8.7 million to 6.2 million trade-ins).

The real question comes down to, how is the volume increase going to affect fleet remarketing efforts, this year and even next? There is a very good chance remarketing efforts in 2011 and 2012 actually brought greater than end-of-term residual levels. This increased competing used supply from new car trade-ins alone will be putting additional pressure on remarketing returns throughout 2013, and especially so in 2014.

Green Movement & Using Alternative Fuels

The fleet industry has been more accepting of the drive to go green and to reduce overall emissions than the retail customer. Today, hybrid and plug-in electric vehicle volumes are growing, while the percentage of overall sales is remaining pretty steady for the past several years at just over 3 percent for 2012 being hybrids with two-thirds of the total volume being Toyota models, and a 0.37-percent level being plug-in electrics, of which just over one-third are Chevrolet Volts, according to hybridcars.com.

The more positive view is within the remarketing channels, where there continues to be a growing interest with the number of bidders and buyers for these hybrids and electrics.

It seems the green movement has slipped over into units fueled by compressed natural gas (CNG) and liquefied natural gas (LNG) within the light-duty pickup, van, and medium-duty truck segments. Probably the biggest concern is the lack of readily available infrastructure for refueling of these units. It takes more time than we have patience for to improve the accessibility to convenient refueling applications, which limits the number of used buyers when remarketing occurs, generally lowering values, and ultimately increasing the seller’s lifecycle operating costs.

Ad Loading...

Let’s not overlook the diesel powerplants within the car and utility vehicles. Currently Volkswagen, Audi, BMW, Mercedes-Benz, and Porsche are offering fuel-efficient cars and utilities using diesel.

Although this penetration is only at 0.86 percent of the total market for 2012, of which three-quarters are from the VW brand, the availability of more choices will increase for 2013, according to hybridcars.com. There is also no concern for this energy source regarding fueling infrastructure or range anxiety.

[PAGEBREAK]

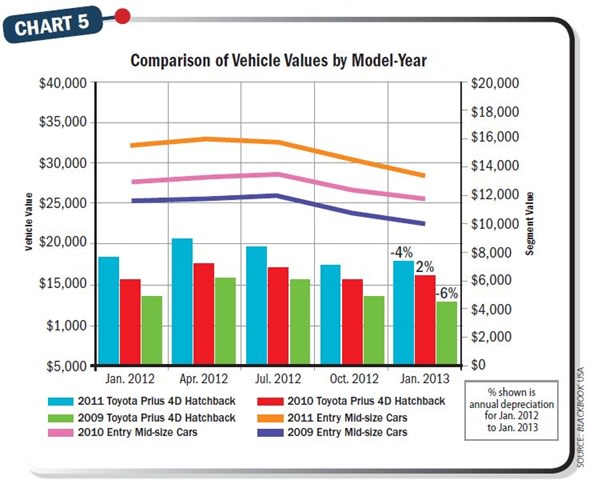

Beginning in January 2012 at a $15,600 average wholesale for the Toyota Prius and at $12,967 for the segment average, the 2010 models had depreciation levels of +2 percent for the Prius to $15,850, while the entry mid-size car segment fi nished $1,278 less, at $11,689, a 10-percent depreciation for the year. Chart courtesy Black Book.

Trending of Market Segments

As Black Book regularly performs fleet industry analysis, a solid portion of the vehicles remarketed are in the full-size car (FSC), passenger minivan (MVW), compact crossover (CXU), and the entry mid-size car (EMC) segments. We recently pulled some data from the highest, or at least higher, volume models within each of these segments to indicate some of the projections along with the current valuation levels.

Previously, some positive returns were noted in relation to end-of-service projected residual levels. In most of these four segments shown, you will see this reality.

Ad Loading...

In Chart 1, the full-size cars include the Chevrolet Impala — the highest volume vehicle remarketed by the top FMCs in 2012. The average 36-month projected value for this segment in 2009 was 34 percent, and, after three years, resulted in a 47-percent return. The projection for the 2010 models segment was increased to 41 percent, and, three years later, it had a return of 47 percent. For individual vehicle trending, the pattern was a similar spread, although below the overall segment averages.

In Chart 2, the passenger minivan segment also showed positive return, but at a more narrow 2010 projection versus a 2013 actual gap within the high-volume model, the Dodge Grand Caravan, at 46-percent projection, ending with a 47-percent actual.

Chart 3 shows compact crossovers bringing a slightly higher percentage level projection with a positive gap at remarketing time. Notice that, in the 2011 projection, the two-year projection value of 62 percent has an actual 65-percent retention and has a smaller gap. We feel this will become an even closer spread for the overall market this year and even more so in 2014.

In Chart 4, the entry mid-size car segment includes a model that stands apart from the crowd and the overall segment averages. From a fleet perspective, the Toyota Prius projections and retention levels are above the segment averages. Notice the 36-month projections from 2009 to 2010 models in relation to the actual returns declined from a 10-percent gap to only 1-percent better retention than the actual return.

Another way to weigh the level of depreciation trending is on an annual basis, as compared to the full normal three-year total life in service. In Chart 5, sticking with the entry mid-size cars and the Toyota Prius example, the 2010 models beginning in January 2012 at a $15,600 average wholesale for the Toyota Prius and at $12,967 for the segment average had depreciation levels of +2 percent for the Prius to $15,850, while the entry mid-size car segment finished $1,278 less, at $11,689, a 10-percent depreciation for the year. The -10 percent level is still stronger than the traditional 15-18 percent depreciation of 16.5 million to 17 million new-car sales the industry has benchmarked over the years.

Ad Loading...

Further data can be viewed by reaching out to Black Book for specific vehicles and segments. The bottom line is the retention values will vary by segment, model, model-year, and length of time in service.

Over the past few years, used vehicles have performed extremely well. With even more technology, improved fuel economy, and the choices of vehicles the variations of retention need to be microanalyzed to have the best business plan prepared. And, in today’s market, the industry has these tools available to assist in your growth.

About the Author

Ricky Beggs is the VP and managing editor for Black Book, and can be reached via e-mail at RBeggs@blackbookusa.com.

A vehicle health score could improve the value of fleet vehicles at remarketing. The path to a universal standard is forming, and fleets that understand the process early will be better positioned when it arrives.

The Iranian conflict and rising gas prices inject much uncertainty into the future wholesale used vehicle markets, as higher gas prices soak up spendable income from vehicle buyers.

James McKinley of City Rent a Truck was named the inaugural Fleet Value Champion at the CAR Conference for his data-driven approach to fleet lifecycle management and vehicle remarketing.

CAR’s annual Fleet Remarketing Awards opened a reimagined 2026 conference designed to bridge the worlds of fleet management and automotive remarketing.

Here's a look inside the awards ceremony at the CAR Conference, where industry leaders reflected on the growth, impact, and future of automotive remarketing.

AI is no longer a luxury but the baseline for profitability in 2026. Auto haulers that adopt these tools now will quickly outpace those using manual workflows and taking a wait-and-see approach.