More News: Used Vehicle Inventory Sets Record for 2025

Wholesale Used Vehicle Prices Decline In October

As the month progressed, used retail sales were higher each week, ending with tighter inventory levels.

November 13, 2025

Compact and mid-size cars continue to see the largest declines compared to last year.

Graphic: Cox Automotive

3 min to read

The Manheim Used Vehicle Value Index (MUVVI) dropped to 202.9 in October, reflecting a 2% decline in wholesale used-vehicle prices (adjusted for mix, mileage, and seasonality) compared to September.

The index is mostly unchanged compared to October 2024. The long-term average monthly move for October is an increase of 0.3%, as the seasonal adjustment factor is typically the weakest of the year.

Non-adjusted wholesale vehicle prices fell 3.7% from September and are 0.2% higher year over year, giving back some of the strength observed throughout most of this year. The long-term average monthly move in non-adjusted values is a decline of 1.5% in October.

In related numbers:

MMR prices for the Three-Year-Old Index declined 2.3% in October.

MMR retention averaged 99% in October, showing no change from September and down 10 basis points year over year.

Sales conversion was 54.9% for the period, down more than two percentage points from September but still higher than the most recent three-year average.

MMR prices declined a bit less than the typical 2.5% decline for this period. MMR retention is generally in line with what is expected for this time of year. Meanwhile, sales conversion indicates a modest softening of demand, as is normal at this time of year, but conversions remain higher than usual for this time of year.

“Trends get a little spooky in October for the wholesale markets, typically showing us the highest levels of depreciation in the year – and this year was no exception,” said Jeremy Robb, Deputy Chief Economist at Cox Automotive, in a Nov. 3 news release. “As October progressed, used retail sales were higher each week, and we ended with tighter inventory levels. This led to slower rates of depreciation than normal in the last week of the month. With tighter days’ supply and solid demand, we may see lower depreciation trends for the rest of Q4. Consumers should see higher tax refunds next year and as more dealers catch wind of that, we could expect more demand at wholesale and retail earlier than usual next year.”

The luxury vehicle segment outperformed the overall market as it has for several months, influenced by higher EV prices helping the segment. On the other hand, compact and mid-size cars continue to see the largest declines compared to last year.

EV values are more volatile, reflecting changing incentives and consumer interest, but may remain higher as values were more depressed last year compared to the rest of the market.

The Electric Vehicle (EV) Index was down 3% from September (post EV tax credit expiration), but up 3.9% year over year.

The Non-EV Index was down 2.2% from September and down 0.1% year over year.

At the end of October, wholesale days’ supply rose to 28 days, higher by two days compared to September, but lower by 1 day year over year.

Wholesale used vehicle supply typically averages around 30 days, indicating a market balance. In October, wholesale supply rose over the month but remained below average, suggesting that inventory may be harder to find, especially as retail demand continues to show strength.

More Remarketing

Manheim Index Shows Used-Vehicle Wholesale Prices Up 2.1% in June

The market is seeing stronger appreciation in older used vehicles this year, and the most affordable segments have been among the year’s best performers.

Read More →

Commercial Fleet Sales Contribute To June, YTD Gains

The fleet sector has boosted its vehicle purchases at a reliable pace in the first half of this year compared with 1H 2025.

Read More →

Used Vehicle Prices Climb Higher As Sales Pace Slows

The higher prices at used retail reflect strong wholesale values earlier in the spring, particularly for older, more affordable vehicles.

Read More →

Wholesale Used Vehicle Market Sustains Moderate Rise In Values, Prices

Trends continue to normalize after a strong start to the year, as consumers contend with higher gas prices in the coming summer months.

Read More →

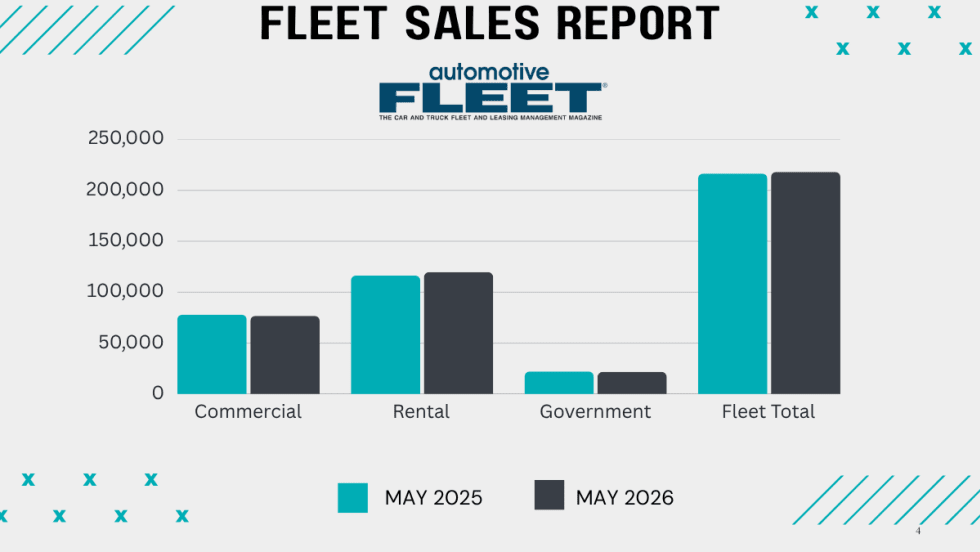

Commercial Fleet Sales Still Lead Sectors Despite May Mini Dip

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

How Connected Vehicle Data Is Lifting Fleet Resale Values

A vehicle health score could improve the value of fleet vehicles at remarketing. The path to a universal standard is forming, and fleets that understand the process early will be better positioned when it arrives.

Read More →

Wholesale Used Vehicle Prices Slightly Up In April

The Iranian conflict and rising gas prices inject much uncertainty into the future wholesale used vehicle markets, as higher gas prices soak up spendable income from vehicle buyers.

Read More →

CAR2026: James McKinley Wins Value Champion of the Year

James McKinley of City Rent a Truck was named the inaugural Fleet Value Champion at the CAR Conference for his data-driven approach to fleet lifecycle management and vehicle remarketing.

Read More →

CAR2026: Eric Autenrieth Wins Remarketer of the Year

Eric Autenrieth was recognized at this year's CAR Conference as the Remarketer of the Year.

Read More →

CAR2026: Lawrence Knapp Wins Consignor of the Year

Lawrence Knapp won the Cosigner of the Year award at this year's CAR Conference.

Read More →