Learn More: 2025 Rental Vehicle Remarketing Summary And Outlook

Up In 2026: Wholesale Used Vehicle Prices, Values

Wholesale values moved even faster than expected on the back of strong retail demand, driving the MUVVI to its highest reading since September 2023.

February 9, 2026

Most vehicle segments are slightly above year-earlier levels in January.

Credit: Cox Automotive

3 min to read

The Manheim Used Vehicle Value Index (MUVVI) rose to 210.5, reflecting a 2.4% increase for wholesale used-vehicle prices (adjusted for mix, mileage, and seasonality) compared to January 2025.

Month over month, the index is up 2.4% in January. The long-term average monthly move is a decrease of 0.2%.

Non-adjusted wholesale vehicle prices are now up 2.5% year over year, and up 2.7% against December 2025. The long-term average monthly move in non-adjusted values is an increase of 0.4% in January.

MMR Prices, Retention & Sales Conversion

MMR prices for the Three-Year-Old Index increased 1.5% in January.

MMR retention averaged 100% in January, up 20 basis points year over year, and up 0.4 percentage points from December.

Sales conversion was 60.7% for the period, 3.2 percentage points higher than the most recent three-year average for January and up 6.5 percentage points from December.

Takeaway: MMR prices for the Three-Year-Old Index increased more than is typical for this period. MMR retention increased slightly and remains seasonally normal for this time of year. Meanwhile, sales conversion indicates strengthening demand, as the metric remains above usual levels for this time of year.

“We had planned for a stronger January from a pricing perspective, but wholesale values moved even faster than we expected on the back of strong retail demand, driving the MUVVI to its highest reading since September 2023," said Jeremy Robb, chief economist for Cox Automotive, in a Feb. 6 news release.

"With tax refund season officially starting last week, we are expecting that more consumers will be getting refunds – and that the size of those refunds will hit a new record," Robb added. "Those factors should help consumers punch the ticket on some big-ticket purchases, even as we have seen a more muted impact on market interest rates amid three Fed cuts since September. The spring bounce for wholesale markets looks like it started early this year, and stronger tax refunds and lower used supply may keep it running for longer than typically seen.”

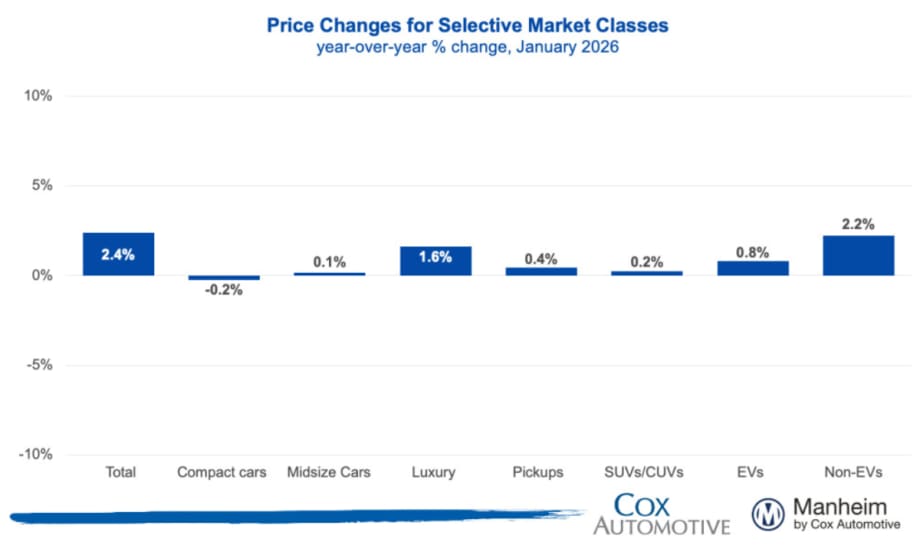

Segment Performance: Year-Over-Year Price Changes

Overall market prices were up somewhat from a year ago, led by the luxury segment and non-electric vehicles, while compact cars posted slight declines.

Takeaway: Most vehicle segments are slightly above year-earlier levels; however, the luxury segment continues to outperform the overall market. We have observed the strength in this segment throughout the last year. Compact and midsize cars continue to see relatively weak price growth compared to this time last year.

EV versus Non-EV Index

EVs: The Electric Vehicle (EV) Index was up 0.8% year over year and up 0.4% from December.

Non-EVs: The Non-EV Index was up 2.2% year over year and also higher by 2.2% from December.

Takeaway: With the expiration of government-backed EV incentives, prices moderated, but remain slightly higher than a year ago, when EV values saw much more depreciation in the first half of the year.

Wholesale Supply and Rental Prices

Wholesale supply: At the end of January, wholesale days’ supply fell to 26.6 days, lower by 0.3 days year over year and lower by 5.1 days compared to December.

Rental prices: Prices for rental vehicles are higher by 2.4% year over year, as they fell slightly in January, down by 0.3% from December. Rental values on a non-seasonally adjusted basis are 2.7% above 2025’s level and rose 0.6% in January, driven by lower average mileage, down 19% against last January overall.

Takeaway: Before the pandemic, wholesale vehicle days’ supply averaged 32 days at the end of January. Days’ supply in January was lower than historical norms but declined seasonally from December.

More Remarketing

Manheim Index Shows Used-Vehicle Wholesale Prices Up 2.1% in June

The market is seeing stronger appreciation in older used vehicles this year, and the most affordable segments have been among the year’s best performers.

Read More →

Commercial Fleet Sales Contribute To June, YTD Gains

The fleet sector has boosted its vehicle purchases at a reliable pace in the first half of this year compared with 1H 2025.

Read More →

Used Vehicle Prices Climb Higher As Sales Pace Slows

The higher prices at used retail reflect strong wholesale values earlier in the spring, particularly for older, more affordable vehicles.

Read More →

Wholesale Used Vehicle Market Sustains Moderate Rise In Values, Prices

Trends continue to normalize after a strong start to the year, as consumers contend with higher gas prices in the coming summer months.

Read More →

Commercial Fleet Sales Still Lead Sectors Despite May Mini Dip

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

How Connected Vehicle Data Is Lifting Fleet Resale Values

A vehicle health score could improve the value of fleet vehicles at remarketing. The path to a universal standard is forming, and fleets that understand the process early will be better positioned when it arrives.

Read More →

Wholesale Used Vehicle Prices Slightly Up In April

The Iranian conflict and rising gas prices inject much uncertainty into the future wholesale used vehicle markets, as higher gas prices soak up spendable income from vehicle buyers.

Read More →

CAR2026: James McKinley Wins Value Champion of the Year

James McKinley of City Rent a Truck was named the inaugural Fleet Value Champion at the CAR Conference for his data-driven approach to fleet lifecycle management and vehicle remarketing.

Read More →

CAR2026: Eric Autenrieth Wins Remarketer of the Year

Eric Autenrieth was recognized at this year's CAR Conference as the Remarketer of the Year.

Read More →

CAR2026: Lawrence Knapp Wins Consignor of the Year

Lawrence Knapp won the Cosigner of the Year award at this year's CAR Conference.

Read More →