Added Insights:Why EVs Will Succeed Long Term

New EV Sales Decline But Used EV Market Grows

April figures show an electric vehicle market facing several challenges that reflect broader economic trends.

May 22, 2025

Uncertainty in the market and tariffs will continue to affect EV sales. A recent consumer survey conducted by Cox Automotive indicates that nearly half of the respondents believe tariffs will affect their decision to buy an EV.

Graphic: Cox Automotive

4 min to read

New electric vehicle sales experienced a decline month-over-month and year-over-year, although the market share in April saw a slight increase compared to March, according to Cox Automotive figures released May 22.

Meanwhile, the used EV market continued to expand, driven by many affordable models.

Manufacturers had mixed results, with some reporting growth and others facing significant decreases.

Inventory levels varied and were influenced by factors such as production adjustments and consumer demand.

New EV Sales: The new EV market faced several challenges in April, reflecting broader economic trends. The volume of new EV sales declined by 5.9% month over month to 100,495 units, while the EV market share rose slightly to 6.9%. Year over year, the EV sales volume decreased by 5.6%.

While most manufacturers saw a month-over-month decline in volume, GM, Tesla, and Nissan reported notable growth in EV sales; Ford, Hyundai Group, and VW Group experienced declines. Tesla’s market share remained below 50%, but it increased by 3.7 percentage points in April, driven by the success of the Model Y, which sold 25,231 units and held a 25.1% market share. GM brands also had a strong month, achieving a combined market share of 14.4%, a 2-percentage-point increase from the previous period. However, uncertainty in the market and tariffs will continue to affect EV sales. A recent consumer survey conducted by Cox Automotive indicates that nearly half of the respondents believe tariffs will affect their decision to buy an EV.

Used EV Sales: The used EV market saw sizable growth in April, driven by strong sales across several key models. Used EV sales grew by 14.4%, reaching 38,763 units and increasing market share to 2.3%, the highest volume and share to date. Year-over-year growth was 60.6%. Tesla continued to dominate the used EV market, with a 27% increase in volume monthly, boosting its market share by 4.7 percentage points to 47%. Chevrolet and Ford followed, holding market shares of 8.9% and 6.0%, respectively, with both brands seeing modest growth in sales volume. This growth in used EV sales comes as new EV sales face challenges due to affordability and availability, making used EVs an option for many buyers.

The price gap between used EVs and internal combustion engine (ICE) vehicles moved below $2,000, the lowest it’s been since July 2024.

Graphic: Cox Automotive

New EV Average Transaction Price: In April, the average transaction price (ATP) for new electric vehicles was $59,255, showing a 0.2% increase from the previous month and a 3.7% increase from the previous year. The price difference between EVs and ICE+ dropped to $11,087, driven by a 2.6% month-over-month increase in ICE+ ATP. Tesla’s ATP increased by 2.6% monthly to $56,120, the highest this year. EV incentives declined by 14% to $6,886, which is 11.6% of the ATP and the lowest dollar amount since June 2024. Despite this decline, EV incentives still exceed the ICE+ average.

Used EV Average Listing Price: In April 2025, the average listing price for used electric vehicles (EVs) was $35,874, showing a 2.8% decline from the previous month but a 3.8% increase compared to the same period last year. The price gap between used EVs and internal combustion engine (ICE) vehicles moved below $2,000, the lowest it’s been since July 2024. Tesla’s prices also saw a decrease, with a month-over-month decline of 1.8%. However, some brands experienced month-over-month price increases, with Volvo leading at a significant 9.6%, followed by Toyota at 4.4%. Affordable options remain available, with 41% of units sold priced below $25,000. Now is the time to get those used EVs under that threshold while the used EV tax credit is still in place.

New EV Days’ Supply: In April, the new EV days’ supply increased by six days, up 4.2%, month over month, rising to 99 days. Year over year, the new EV days’ supply is down nearly nine days (19.9%), marking the widest gap between EV and ICE+ days’ supply since July 2024. Days’ supply varied a lot by make. Lexus and Genesis had some of the tightest inventory, while Ford, Audi and VW saw stocks increase in April. Days’ supply has shifted of late, which is the dynamic nature of the EV market influenced by factors such as production adjustments, consumer demand, and inventory management strategies.

Used EV Days’ Supply: In April, the days’ supply of used electric vehicles declined by 0.2% month over month and year over year. Last month, used EVs had a six-day higher supply than ICE+ vehicles. Now, with ICE+ supply flat and used EV supply declining, the average supply of used EVs is two days lower. Similar to the new EV market, the days’ supply for used EVs varies by make. As used EVs remain an attractive option, inventory will continue to tighten.

More Remarketing

Manheim Index Shows Used-Vehicle Wholesale Prices Up 2.1% in June

The market is seeing stronger appreciation in older used vehicles this year, and the most affordable segments have been among the year’s best performers.

Read More →

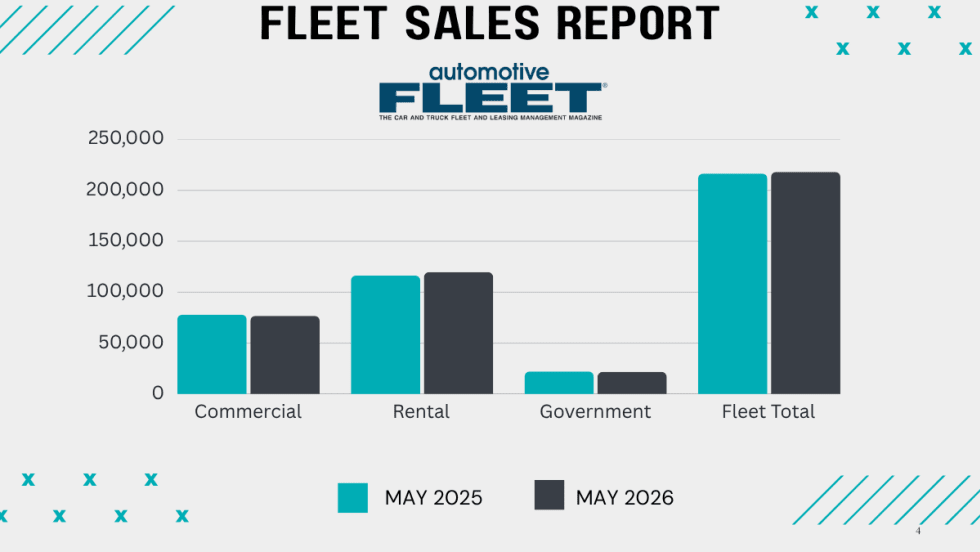

Commercial Fleet Sales Contribute To June, YTD Gains

The fleet sector has boosted its vehicle purchases at a reliable pace in the first half of this year compared with 1H 2025.

Read More →

Used Vehicle Prices Climb Higher As Sales Pace Slows

The higher prices at used retail reflect strong wholesale values earlier in the spring, particularly for older, more affordable vehicles.

Read More →

Wholesale Used Vehicle Market Sustains Moderate Rise In Values, Prices

Trends continue to normalize after a strong start to the year, as consumers contend with higher gas prices in the coming summer months.

Read More →

Commercial Fleet Sales Still Lead Sectors Despite May Mini Dip

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

How Connected Vehicle Data Is Lifting Fleet Resale Values

A vehicle health score could improve the value of fleet vehicles at remarketing. The path to a universal standard is forming, and fleets that understand the process early will be better positioned when it arrives.

Read More →

Wholesale Used Vehicle Prices Slightly Up In April

The Iranian conflict and rising gas prices inject much uncertainty into the future wholesale used vehicle markets, as higher gas prices soak up spendable income from vehicle buyers.

Read More →

CAR2026: James McKinley Wins Value Champion of the Year

James McKinley of City Rent a Truck was named the inaugural Fleet Value Champion at the CAR Conference for his data-driven approach to fleet lifecycle management and vehicle remarketing.

Read More →

CAR2026: Eric Autenrieth Wins Remarketer of the Year

Eric Autenrieth was recognized at this year's CAR Conference as the Remarketer of the Year.

Read More →

CAR2026: Lawrence Knapp Wins Consignor of the Year

Lawrence Knapp won the Cosigner of the Year award at this year's CAR Conference.

Read More →