Vocational Fleet Sales Remain Flat in Canada in 2019

Canada is primarily a service-based economy, largely driven by small local businesses. The strongest vocational segments for fleet sales in Canada are energy and construction. The dominant fleet vehicle segment is light trucks.

The Automotive Fleet & Leasing Association (AFLA) is launching its first-ever fleet conference in Canada. Known as the AFLA Canada Fleet Summit, it will be held on Feb. 12-13, 2020, at the Hilton Toronto Airport Hotel in Mississauga, Ontario. You can register for the conference by clicking here.

Photo courtesy of Elijah-Lovkoff via Gettyimages.com.

6 min to read

From January to September 2019, overall fleet sales in Canada were flat compared to the same nine-month period last year, according to Scotiabank Economics. Lackluster fleet sales are contributing to total new-vehicle sales in Canada remaining flat in calendar-year 2019.

In calendar-year 2018, the most current full-year data available, there was a total of 106,515 fleet cars registered and 306,697 fleet trucks registered, according to Canadian Automotive Fleet magazine. One example, by brand is Chevrolet, Buick, GMC and Cadillac dealers who delivered 73,642 fleet sales for the full year of 2018.

Ad Loading...

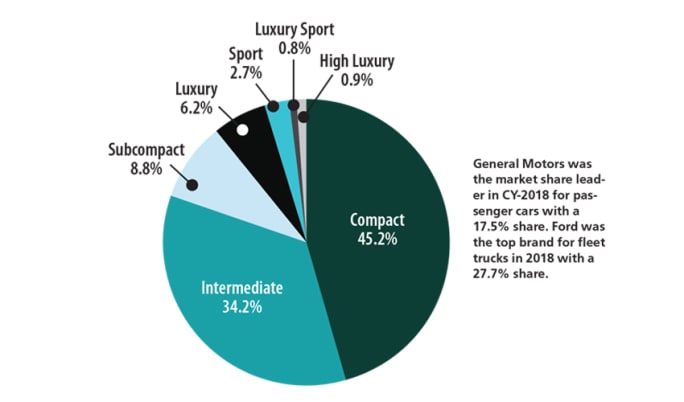

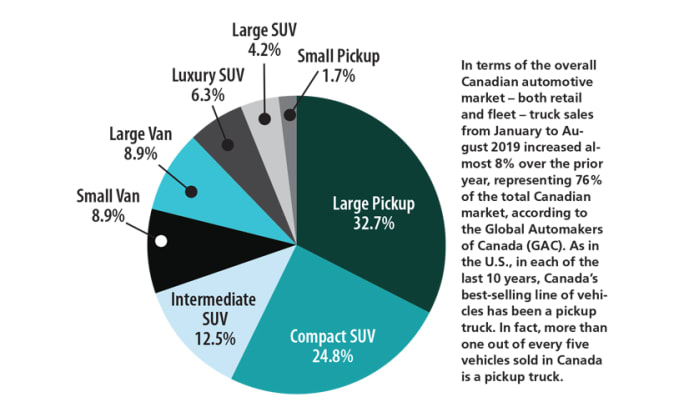

General Motors was the market share leader in CY-2018 for passenger cars with a 17.5% share. Ford was the top brand for fleet trucks in 2018 with a 27.7% share.

Mature Fleet Market

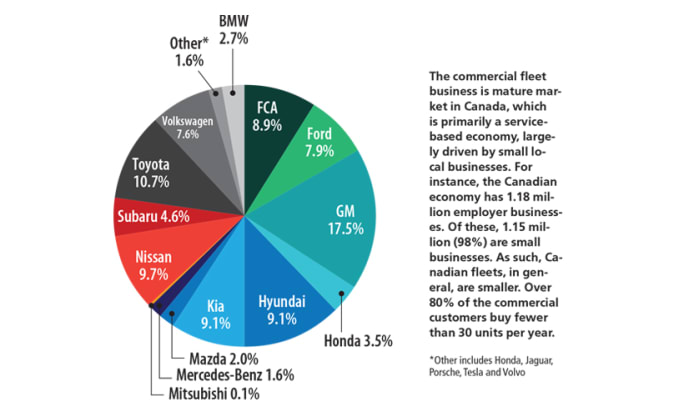

The commercial fleet business is mature market in Canada, which is primarily a service-based economy, largely driven by small local businesses.

The total OEM share for fleet car registrations in calendar year 2018. This accounted for 106,515 assets.

For instance, the Canadian economy has 1.18 million employer businesses. Of these, 1.15 million (98%) are small businesses. As such, Canadian fleets, in general, tend to be smaller. Over 80% of the commercial customers buy fewer than 30 units per year. It is difficult to identify the average fleet size in Canada. Estimates range from 35 to 70 units, with the average very much dependent on what is the definition of “fleet” which can vary.

Beyond the small to medium enterprise (SME) market, there are a number of large megafleets operated by utilities, nationwide delivery companies, and large multinational corporations, many of which operate in the country’s vast energy sector.

Approximately 55-60% of the commercial fleet vehicles are owned and the remainder are leased. Of the leased vehicles, the majority, more than 90%, are funded using an open-end lease. In terms of vehicle depreciation trends, a 2% per-month depreciation reserve is used by most fleets in Canada.

Ad Loading...

Pickups Dominate Fleet Market

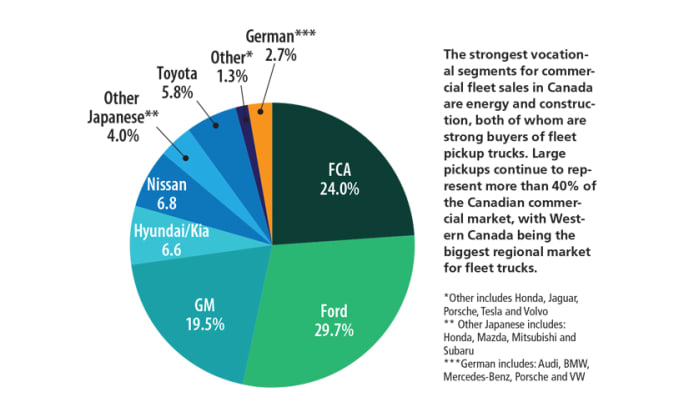

The largest vocational segments for commercial fleet sales in Canada are energy and construction, both of whom are strong buyers of fleet pickup trucks. Construction plays a major role in the economic activity in Canada, especially in the provinces of Ontario and Quebec. Currently, the uptick in new construction activity is stimulating commercial fleet sales.

The total OEM share for light truck fleet registrations in 2018. This accounted for 306,697 assets.

Large pickups continue to represent more than 40% of the Canadian commercial market, with Western Canada being the biggest regional market for fleet trucks. In terms of the overall Canadian automotive market — both retail and fleet — truck sales from January to August 2019 increased almost 8% over the prior year, representing 76% of the total Canadian market, according to the Global Automakers of Canada (GAC). As in the U.S., in each of the last 10 years, Canada’s best-selling line of vehicles has been a pickup truck. In fact, more than one out of every five vehicles sold in Canada is a pickup truck.

According to DesRosiers Automotive Consultants “Top 10 August 2019” report, passenger car sales continue to decline year-to-date across the industry while pickups and all classes of SUVs gain market share. In Canada, the compact-crossover segment is the fastest-growing segment in Canada, which is similarly the fastest-growing segment in the U.S. Most buyers in this segment are switching from passenger cars, but others are also downsizing from larger SUVs.

Cost containment pressures run throughout the Canadian fleet market. One way Canadian fleets have been looking to reduce acquisition and operating costs is by downsizing to a smaller truck segment. For instance, some fleets are moving from three-fourth ton trucks to half-ton in an effort to reduce acquisition cost and improve fuel efficiencies.

10 Provincial Economies

Canada’s fleet market is diverse, and its vitality varies by region. As a result, there is not a single fleet market in Canada and market dynamics will vary by region and industrial sector.

Ad Loading...

Total fleet car registrations by vehicle segment in 2018. Compact cars held a 45.2% share, followed by intermediate cars which held 34.2% share.

In 2019, government spending at both the federal and provincial level has slowed. There is a tighter fiscal policy at the provincial level, but the forecast is for growth to pick up in calendar-year 2020 across most regions.

AFLA to Launch Canada Conference in February

The Automotive Fleet & Leasing Association (AFLA) is launching its first-ever fleet conference in Canada. Known as the AFLA Canada Fleet Summit, it will be held on Feb. 12-13, 2020, at the Hilton Toronto Airport Hotel in Mississauga, Ontario.

The conference will focus on disseminating Canadian-specific fleet best practices and facilitate peer-to-peer benchmarking of non-proprietary fleet information.

You can register for the conference by clicking here.

The weakest fleet sales are occurring in Western Canada, which has experienced sluggish growth over the past year due to softness in commodity prices, in particular, the decline in shale oil prices, which is constraining growth in the provinces of Alberta and Saskatchewan.

The downward pressure on commodity prices has caused a pullback in business investment in many areas, including a decline in the acquisition of fleet vehicles by the oil and energy sector. The slowdown has been most acute in Alberta, where mandated production cuts and elevated unemployment restrained growth. Vehicle sales in Alberta posted consecutive year-over-year decreases.

According to the Canadian Association of Petroleum Producers’ (CAPP) “2019 Crude Oil Forecast, Markets and Transportation” report, the forecast is for a constrained outlook for Canadian oil production from 2019 to 2035.

Although the country’s overall crude oil production is expected to grow over the coming years, the CAPP growth forecast is significantly reduced from previous expectations due to ongoing pipeline constraints and inefficient regulations, which are holding back expansion of Canada’s oil sector.

Ad Loading...

The crude oil slump weakened the Canadian dollar against the U.S. dollar. The Canadian dollar has fallen by about 20% against the U.S. dollar. On the positive side, a devalued Canadian dollar boosts the tourism industry stimulating daily rental sales and helps exporting manufacturers by making their products and services more price competitive, boosting new-vehicle demand in the fleet transportation segment.

The economic slowdown in the oil-rich provinces of Alberta and Saskatchewan has been somewhat offset by growth in other provinces, such as Quebec and Ontario, whose economies are based more so on manufacturing and exports of finished products.

After expanding by 2.5% in 2018, the growth in the manufacturing-heavy Quebec economy has slowed to just below 2% .

Though manufacturing plays an important role in Ontario’s economy responsible for 12% of Ontario’s GDP, the service sector makes up the bulk, 78%, of the economy. The forecast is the services industries will outperform goods industries, remaining the primary growth driver in Ontario’s economy.

Analysis of 2019 Fleet Sales

Historically, overall fleet sales in Canada have always been tied to the robustness of the national economy.

Ad Loading...

Total light truck registrations by vehicle segment in 2018. Large pickups held a 32.7% share of the market, followed by 24.8% for compact SUVs.

Overall improvements in sectors such as housing, construction, and infrastructure assisted in modestly growing overall fleet sales. For instance, government spending on infrastructure is increasing, which will stimulate the economy, positively impacting government fleet sales.

Construction is playing a bigger role in the economic activity Canada is experiencing in Ontario and Quebec, which has stimulated commercial fleet sales. Also helping the Canadian economy is the ongoing strength in the U.S. market and the weaker Canadian dollar, which is boosting U.S. demand for Canadian exports.

Canada is a net export nation with 75% of its exports going to the U.S., its largest trading partner. One factor strongly influencing the commercial fleet market is the foreign exchange rate of the Canadian dollar, which has declined against the U.S. dollar. The ongoing growth in the U.S. market and the weaker Canadian dollar boosts U.S. demand for Canadian exports.

CY-2020 Economic Forecast

The forecast is that vehicle sales in Canada will slowly edge downward with a total of 1.93 million units delivered in 2019. One factor favoring growth in retail sales is that the car parc for Canadian consumers is aged, averaging 10-11 years old, creating pent-up demand. Low interest rates have also made auto loans more affordable stimulating retail buying in the new car and truck markets.

The Canadian economy is forecast to achieve an average GDP growth of 1.6% for calendar-year 2019, according to economic forecasts. Nonetheless, growth was reported in 15 out of 20 major industries, according to Statistics Canada.

Part Two: Commercial auto remains one of the most challenging and costly lines of coverage for fleet operators and insurers alike. Continue learning more about how to effectively address these issues from Onur Aksan, Enterprise Business Development Executive, Geotab

Vehicle replacement decisions affect every aspect of fleet performance, from operating costs to asset availability. This guide explores how fleet leaders use integrated data, benchmarking, and lifecycle analytics to determine the right fleet size and optimize replacement timing with greater confidence.

Commercial auto remains one of the most challenging and costly lines of coverage for fleet operators and insurers alike. Learn more about how to effectively address these issues from Onur Aksan, Enterprise Business Development Executive, Geotab.

Departmentally assigned vehicles often create hidden costs through underutilization, poor visibility, and increased administrative burden. This white paper explores how shared motor pool strategies help fleets reduce costs, improve accountability, and optimize vehicle utilization.

Fleet leaders are under pressure to reduce costs, adapt to economic uncertainty, and make smarter decisions. See how peers across North America are responding with real data, proven strategies, and forward-looking insights. Download the 2026 Market Pulse Report to benchmark your strategy and uncover where you can gain an edge.

Viaduct will join Sumitomo as an independent subsidiary. Partnership strengthens global reach and accelerates AI-driven innovation for fleets and manufacturing.

Held in Sydney, the Australasian Fleet Management Association’s 2025 Summit marked ten years of growth as the event expanded its global reach and doubled down on practical, non-commercial fleet leadership programming.