Mexico: Analysis of the Fleet Market

The automotive industry in Mexico has been growing each year since 2009, but 2017 was the first year sales decreased. Although retail and fleet sales declined, Mexican automotive industry continues to post strong export sales.

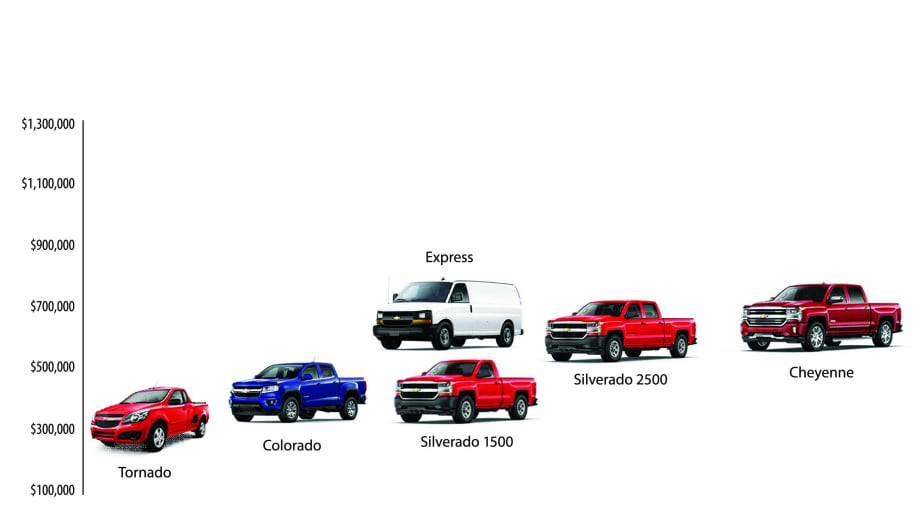

Pickup trucks are bread-and-butter fleet vehicles in Mexico as illustrated below by the model range of GM de Mexico’s truck portfolio. GM’s smallest truck, the Tornado is imported into Mexico from GM Brazil and competes in the Pickup-B segment of the market. The Tornado also can be upfitted with a box on the back allowing it to function as a small van.

Photo courtesy of GM.

Historically, fleet sales in Mexico averaged between 17% and 20%. Fleet sales have been steady for the past decade, but industrywide fleet sales in Mexico declined 13.6% in CY-2017 compared to the prior year. The decline in sales primarily occurred in the daily rental and government segments. One silver lining to the industry’s 2017 sales performance was that total commercial fleet sales increased.

Photo courtesy of GM.

Annual sale of new vehicles in Mexico decreased in calendar-year 2017 by 4.6% to 1.53 million light vehicles, primarily because of higher inflation, which dampened domestic consumption, according to the Mexican Association of the Automotive Industry (AMIA).

This is in contrast to calendar-year 2016, when auto sales in Mexico increased 19% to a record 1,603,672 light vehicles, the highest volume in the history of the country’s automotive industry. A key contributor to this sales increase in 2016 was General Motors de Mexico, which produced 20% of those units. The period from 2015-2016 marked two consecutive years of strong double-digit gains for the Mexican domestic market fueled by strong auto financing and a stable economy, as well as more rigorous enforcement to curtail illegal imports of used cars from the United States, which Mexican dealers complained cannibalize new-vehicle sales.

However, the sales momentum from 2015-2016 was turned around in CY-2017 when total automotive sales in the Mexico domestic market, including both retail and fleet sales, cumulatively decreased 4.6% versus 2016. The decline in auto sales in CY-2017 was the first decline in the prior eight years of automotive sales growth.

“In the best case, the forecast for 2018 sales is to be flat because of the market volatility we are having, which is going to be challenging for every OEM,” said Miguel Gonzales, fleet director for GM de Mexico.

There were several factors contributing to the decline in retail automotive sales in 2017. First, was the decision by the Mexico central bank to raise interest rates to curb inflationary pressures, which increased the cost of car loans. Second, the Mexican government ended fuel subsidies in 2017, which caused fuel prices to spike generating consumer uncertainty. Third, both factors combined have contributed to a decline in overall consumer confidence in Mexico.

The increase in the price of vehicles, higher interest rates, and the indebtedness of many Mexican consumers put a downward pressure on automotive purchases by local buyers.

Fleet Sales Within Mexico Decline in CY-2017

Industry-wide, fleet sales in Mexico decreased 13.6% in CY-2017 compared to the prior year. The decline in fleet sales primarily occurred in the daily rental and government segments. One silver lining was that total commercial fleet sales in Mexico increased.

Historically, fleet sales to government and daily rental companies account for a cumulative 20% of fleet sales, with each segment representing 10% of the Mexican fleet market.

Among the reasons why fleet sales to daily rental companies decreased were higher fuel prices and reduced consumer confidence, contributing to a decline in local market car rentals, which offset the record increase in foreign tourists in 2017.

Fleet sales to governmental agencies declined due to the Mexican government’s decrease in investment expenditures resulting in less need for replacement vehicles.

In CY-2017, the only fleet segment in Mexico that increased sales vis-a-vis 2016 was the commercial market, which represents 55% of total fleet sales in the country. In addition, fleet leasing companies operating in Mexico represent another 25% of total fleet sales.

“In 2017, the OEMs sold 75% of their fleet vehicles to private commercial companies and leasing companies,” said Gonzales of GM de Mexico.

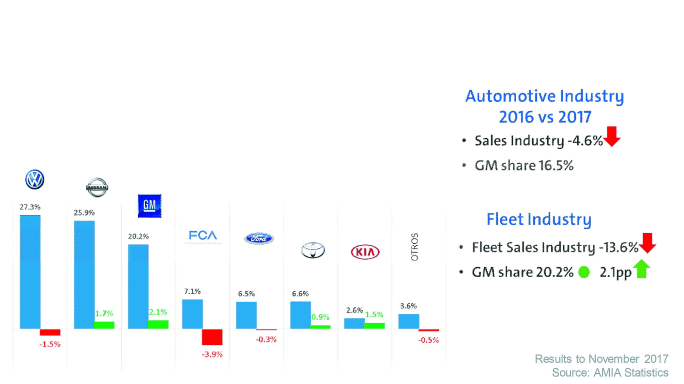

Although fleet sales decreased 13.6% in CY-2017, GM de Mexico gained fleet market share, reaching 20.2%, which represented a 2.1 percentage point increase.

Preliminary 2018 Sales Trends in Mexico

The 2017 decline in Mexican auto sales coincided with President Trump’s first year in office, which was highlighted by the uncertainty caused by his threat to withdraw from the North American Free Trade Agreement (NAFTA). The uncertainty about the future of NAFTA created volatility in the value of the peso against the U.S. dollar that prompted Mexico to raise interest rates to curb the resulting inflationary pressures.

As of press time, only first quarter 2018 sales in Mexico were reported, but the momentum of the 2017 sales decline has continued into March 2018, with Mexican vehicle sales down to 118,600 units, a 13.4% decline compared to the prior year. Both passenger car and truck sales declined. The biggest decline was with passenger cars, which were down 16.3% to 74,809 units. While SUVs and pickups were down, they declined only 8% vis-à-vis 2016 to 43,791 units.

When analyzing March 2018 sales by vehicle segment, the largest segment by volume was subcompact cars, accounting for 40,315 units sold, of which the Chevrolet Aveo (5,197 units) was the industry’s top-selling subcompact, followed by the Nissan March (5,108 units), and Chevrolet Beat (4,324 units).

In the compact car segment, a total of 27,173 units were sold. The Nissan Versa (7,920 units) was the top-selling compact, followed by the VW Jetta (3,716 units), and Nissan Sentra (3,320 units).

In the SUV segment, a total of 27,039 units were sold. Honda CR-V (2,270 units) was the top-seller, followed by Nissan Kicks (1,880 units), and Kia Sportage (1,831 units).

In the pickup segment, a total of 15,682 units were sold, with the Nissan NP300 (6,562 units) being the best-selling pickup model.

Breaking down sales by brands, Nissan was the market leader in March with 24% market share, with GM being No. 2 with a 16.5% share, followed by VW Group at 13.6%, Toyota at 7%, and Kia with a 6.5% market share.

By entering into renegotiations of NAFTA, promising a U.S.-Mexico border wall, and embracing an America First economic policy, President Trump has exerted downward pressure on Mexico’s auto industry over the past year.

These developments have not only created economic uncertainty, but also political uncertainty as to who will be the new Mexican president after elections in July 2018.

Mexico’s Automotive Market

There are 34 million vehicles in operation in Mexico, of which 34% of them are commercial vehicles. The majority of large fleets operating in Mexico are owned or leased by multinational companies.

Historically, fleet sales in Mexico averaged between 17% and 20%. In terms of vehicle acquisition trends in the Mexican fleet market, the most important segments for fleet are, in order, B-Car, C-Car, and Pickup-D. These are the most important vehicle segments for commercial fleet; however, the sales volumes in these segments have decreased versus the year prior.

Another reason for GM de Mexico’s strong performance in 2017 sales is the freshening of it new-product portfolio.

“Some important news with our fleet vehicles portfolio is that we updated the Chevrolet Aveo. We have just launched the 2018 Aveo with a facelift to the front grille and bumper, and because we know safety is becoming more and more important for our customers, we have added option packages that include airbags,” said Gonzalez. “In the second half of 2017, we launched the brand-new Chevrolet Spark model-year 2018 that will incorporate airbags and ABS in all its packages, including the cargo model.”

Earlier, the new Chevrolet Sonic was launched with a complete exterior redesign, with the addition of airbags and ABS in all packages.

The subcompact is the most popular vehicle segment in the overall automotive market in Mexico, accounting for more than 30% of new-vehicle sales in the country.

GM de Mexico has several significant new-model launches in Mexico. In the A-Car segment, GM launched the new Beat, which starts around 100,000 pesos. This is the latest iteration of GM’s perennial best seller. The previous generation of the Beat, launched more than 10 years ago, was the best-selling vehicle for many years both in the retail and fleet markets.

“The most popular Beat model in the Mexico fleet market is the cargo version, which has an air-conditioned rear cargo area. GM also launched a Notchback version of the Beat, which is the most affordable van in the market. All of our vehicles are equipped with airbags and in the highest trim level package, the Beat is equipped with the Chevrolet MyLink system,” said Gonzales of GM de Mexico.

The key vehicle for the vocational fleet markets is the B-Car, which is the highest volume vehicle segment in Mexico. Approximately 37-38% of total fleet sales for the industry are allocated in this segment.

In the B-Car segment, GM launched in late in 2017 a new 2018 Chevrolet Aveo, “This new generation with a complete new image, improved its safety capabilities including two or four airbags, and a four-wheel ABS systems,” said Gonzales. “It has a 1.5L engine that features higher fuel efficiency, and the vehicle is bigger, providing more space for passengers.”

GM de Mexico also sells electric vehicles, such as the Volt and Bolt EV, and high-performance vehicles, such as the Camaro and Corvette.

The second most popular vehicle segment is the C-Car, which represents around 14% of total fleet sales in Mexico. In the C-Car segment, GM launched the brand-new Chevrolet Cavalier last August which is positioned between the Aveo and Cruze. Imported from China, the new 2018 Chevrolet Cavalier offers a small 1.5L engine with 107 hp and 104 lb.-.ft. of torque associated with five-speed manual transmissions or an automatic six-speed with manual mode. The Cavalier also features important safety features: airbags for all passengers, ABS, and StabiliTrak. “The Cavalier has high fuel efficiency, with 20.2 kilometers per liter, with the best fuel efficiency in the segment. It also features the OnStar system,” said Gonzales.

One of the most important segments is the fast-growing Pickup-B segment, which is now the third most important vehicle segment in the Mexican market.

There is growing popularity with fleets of Pickup-E and SUV-B models. Capitalizing on this popularity is GM de Mexico, which offers the Equinox, Traverse, Tahoe, and Suburban. GM launched in Mexico the brand-new Equinox and brand-new Traverse at the end of the 2017.

The GM truck lineup in Mexico also includes the Colorado, which replaces the S10, the Silverado 1500, Silverado 2500, and the Express van and cargo van.

GM’s smallest pickup truck, the Tornado is imported into Mexico from Brazil. “It is a very good small pickup. It competes in the Pickup-B segment. It features a 1.8L, four-cylinder engine, which gives it a very good TCO that is the best in the market,” said Gonzales. “And it has a very good capacity. In Mexico, we have agreements with upfitters to put a box on the back, giving a company a small van based off that vehicle, which is ideal for use in cities with the narrow streets. It is also used as a government vehicle.”

Although Mexican consumers are holding back on new-vehicle purchases, Mexico’s auto export sector is very strong and delivering trade surpluses that are helping to stabilize the economy.

The Mexican automotive OEM trade association, AMIA, has released a preliminary production forecast of over 4 million units for 2018, a 6% increase in output over 2017, whose full-year production came to 3.77 million units, of which 3.10 million units were exported. About three-quarters of the exports went to the U.S. For instance, exports represent 69.1% of GM de Mexico’s total production, with the majority of units earmarked for sale in the U.S. The second-largest automotive export destination for GM de Mexico is Canada, which is the recipient of Mexico-assembled Silverado, Sierra, and Trax models that are shipped to Canadian dealers.

“The third most important market for GM de Mexico is Argentina, but we only export Trax to them,” said Gonzalez.

Calendar-year 2017 was the best year ever for automotive production in Mexico. Exports of local automotive production in Mexico exports grew 9.4 % year-over-year, surpassing total automotive exports from Japan and South Korea.

Mexican auto production and exports hit a record high in 2017, far outpacing growth in 2016, despite fears that shipments could be hurt by a renegotiation of NAFTA. Full-year 2017 auto exports grew 12.1% and production increased 8.9%. Mexico had a nearly $71 billion trade surplus in autos and auto parts in 2017, including light and heavy vehicles, which was a record.

Leasing Growing Within Mexico

The popular Chevrolet Cavalier returned to the Mexico market in 2018. The five-passenger

Cavalier is a C-Car and is positioned in the executive segment of the GM Mexico

portolio. It offers a suite of safety equipment and provides excellent fuel economy.

Photo courtesy of GM.

Vehicle ownership has been the traditional funding method in Mexico, but there is a growing acceptance of leasing as a form of vehicle funding, especially among commercial fleets.

In the Mexican fleet market, there are two distinct fleet leasing products available. One is the traditional “American” open-end model based on transferring residual risks to the lessee, and operational expenses (such as taxes, insurance costs, maintenance, and repairs) are likewise passed as they occur. Open-end leases convert into financial leasing under Mexican generally accepted accounting principles (GAAP). Residual value risk is borne by the lessee and interest rates are typically variable.

The second lease funding option is the “European” closed-end model – also known as “renting” or “full-service leasing.” It is based on a monthly installment payment, which includes all operational expenses based on an agreed mileage and all risks are borne by the lessor. Interest rates are kept fixed over the period of the lease.

In the past eight years, full-service leasing is becoming more popular among corporate and government fleets.

Most fleet leases in Mexico are open-end leases. Closed-end leases are not as popular and are typically more expensive than open-end leases. The preferred acquisition option for most medium and large corporations is purchase. The reason is that corporations operating in Mexico are cautious about interest rate risk. Typically, fleet funding is based on a floating interest rate; however, fixed rates are available, which are tied to the Prime rate.

Vehicle lease terms are typically 36 months, with some lease terms extending to 48 months. Most leases are written on fixed-rate contracts insulating lessees from future run-ups in rates.

Initiatives to Boost Fleet Sales

In Mexico, manufacturer fleet pricing is based on buying volume. Fleet vehicles can only be purchased through dealers using a courtesy delivery system. Typically, vehicles are delivered out of dealer inventory.

GM de Mexico initiatives to further increase its volume of local fleet sales include expanding its Fleet Services Program to increase coverage in its dealer network and the re-launching of the Small-Medium Business Program. In 2015, GM launched its “Fleet Services” initiative in Mexico, homologating prices across a range of dealers.

“GM dealers in Mexico are playing an important role in supporting the corporation’s fleet sales initiatives. For instance, GM offers the only fleet-certified dealer network in the market,” said Gonzales. “Dealers are a key factor to success in fleet sales, and we have the best and most professional dealer network.”

In addition, GM de Mexico is aiming to improve performance in its Supplier and Business Partners Program as well. Several fleet leasing companies have initiated certification programs for their preferred maintenance network.

At a growing number of businesses in Mexico, there is a move to focus on their core business, which favors the outsourcing of non-core activities, such as fleet administration and management of fleet services.

Rising Fuel Prices in Mexico

Mexico has significant oil reserves and is the seventh largest oil producer in the world. Previously, there was only one fuel supplier in Mexico, the state-owned oil company Petroleos Mexicanos (PEMEX), which is one of the largest oil companies in the world. At that time, PEMEX owned and managed all gasoline stations within the country. As a result, gasoline and diesel pump prices are very stable and subsidized by the Mexican government. Due to its monopoly, PEMEX had no incentive to negotiate on prices or provide services, such as payment by credit card.

In 2017, the government of Mexico began deregulating the country’s energy sector. The change in policy eliminated fuel subsidies and price controls to allow prevailing international gasoline prices to manage the market. It is the first such government move since 1992 when the government controlled inflation by setting a ceiling on the maximum allowable price of fuel.

Since Nov. 30, 2017, fuel prices have been fully deregulated in all regions of Mexico, meaning that the federal government no longer sets or publishes daily maximum prices. The Mexican government’s move raised the maximum allowable price of fuel, with regular gasoline prices increased 14%, premium was raised 20%, and diesel went up 17%.

The price increases varied across Mexico, but universally fuel prices were quite high when compared to the average salary of a working person. The higher fuel price increases triggered demonstrations across the country. Pushback from the public also included blockades at gas distribution terminals, seaports, and transportation routes. As well, people stockpiling gasoline and diesel before prices further increased. In addition, theft by drug cartels and crime groups from PEMEX who tap pipelines to siphon off fuel has been rampant. Fuel theft from PEMEX refineries and pipelines costs the Mexican federal government more than US $1 billion annually in lost revenue.

Despite the public protests, the Mexican government hopes that deregulation will attract more foreign investment in its oil and gas industry. The decision reverses 79 years of central control of the country's oil industry. In 1938, the Mexican government nationalized the industry by expropriating the assets of nearly all of the foreign oil companies operating in Mexico.

Over the long term, officials in the Mexican government expect that fuel prices will become more reasonable once new competitors return to the country and build new import terminals and pipelines, as well as engage in oil exploration.

In Mexico, there is limited coverage by fuel management companies and these typically include only pre-paid options. Not all fuel stations in Mexico accept credit cards, with most cards being pre-paid. Many company drivers receive a budget to purchase fuel.

Some companies in Mexico require that fleet drivers to pay for maintenance and repairs of their company vehicle.

In addition, Mexico’s energy reform opened the retail fuel market to private foreign and national companies, which until recently was monopolized by PEMEX. There are now more than 30 gas station brands in Mexico, according to the federal Energy Secretariat.

At the end of a vehicle’s service life, most corporations give drivers the option to buy the vehicle.

In Mexico, almost all off-lease vehicles are sold back to the driver at an extreme bargain price because, historically, there has been no formal used-vehicle market, auctions, or wholesalers.

Approximately 95% of fleet passenger vehicles are sold to drivers.

Macroeconomic Trends Affecting Mexican Economy

Mexico has a population of 130.7 million people living in 32 states. It has a diversified economy ranked 11th in the world with a gross domestic product (GDP) of $1.4 trillion USD. The growth in the Mexican economy is not only with local businesses operating within the domestic economy, but also from significant foreign investments, in particular by the global automotive industry.

Photo courtesy of GM.

Mexico has a population of 130.7 million people living in 32 states. It has a diversified economy ranked 11th in the world with a gross domestic product (GDP) of $1.4 trillion USD.

The growth in the Mexican economy is not only with local businesses operating within the domestic market, but also by significant foreign investments.

Today, Mexico is the world’s seventh largest automotive producer having surpassed Brazil in 2014 and the world’s fourth largest exporter of assembled automobiles. The total Mexican automotive industry employs 1.7 million people, which includes direct and indirect employees. What has accounted for the dramatic growth in the past two decades has been a huge volume of foreign investments in Mexico by a variety of automotive OEMs establishing brand-new factory operations in the country, mainly for export purposes. Currently, the automotive sector accounts for more than 17% of Mexico’s manufacturing sector.

A key factor driving this investment in the Mexican automotive sector is that the country has 13 free-trade arrangements, which, besides the U.S., encompasses 45 countries within the European Union, South America, and Asia.

Mexico’s auto sector has benefited from NAFTA as major manufacturers, such as General Motors Co., Ford Motor Co., Fiat Chrysler Automobiles, and Volkswagen AG, have made the country a top export hub, attracted by low-cost labor and free trade pacts with more than 45 nations.

One unintended consequence to the rapid expansion of the automotive industry is that it has exceeded the capacity of Mexico’s infrastructure to handle this increased business activity. For instance, this increased business volume has constrained the haulaway auto transport industry and ports infrastructure capability, which has increased lead times to export vehicles. The deficiency in port infrastructure is delaying the loading of ships departing for South America and the off-loading of ships arriving from Asia.

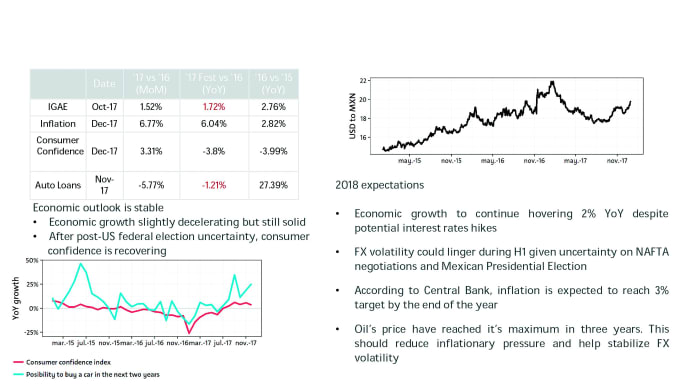

After achieving 2.4% growth in GDP in CY-2017, the Mexican economy will continue to grow at rates above 2% in CY-2018. The same rate of growth is forecast for calendar-year 2019.

In other ongoing trade developments, Mexico will be temporarily exempt from U.S. tariffs on steel and aluminum imports set to take effect in late May. The exclusion is likely contingent on satisfactory NAFTA negotiations, with progress in the most recent round of talks—concluded in early March.

Interest Rates & Regulations in Mexico

In February 2018, Mexico’s central bank raised its key interest rate to curb inflation pressures, due to a weakening peso and higher gasoline and food prices.

Economists expect the Mexican peso to remain volatile due to concern about Mexico’s trade ties with the U.S. and the national election on July 1, 2018, when voters will elect a new president to serve a six-year term, 500 members of the Chamber of Deputies and 128 members of the Senate.

Last January 2018, the exchange rate fell to one U.S. dollar for 22 pesos, but recovered a bit to one U.S. dollar for 19 pesos. The uncertainty of NAFTA negotiations and the outcome of these presidential election has caused fluctuation in the exchange rate between the dollar and peso. In addition, oil price increases have contributed to upward inflationary pressures. In addition, a weaker peso will put a drag on growth in the domestic Mexican economy, but will benefit exports. Higher fuel prices will also create upward pressure on inflation.

The weakness of the currency has two factors: on the one hand, the price of vehicles in the local retail market will be higher and, on the other hand, it will decrease the value of exports. There is significant upward price due to vehicles equipped with the latest technologies being marketed in the domestic market. A weaker peso also lowers the cost of Mexican automotive exports.

Current interest rates and taxation rates are having a favorable impact on fleets. Two years ago, a new tax law was implemented by the Mexican government, which was favorable for leasing.

Taxes are a major factor in fleet purchases. There is a federal tax ‘tenenica,’ which is 10% of the original cost of the vehicle paid over four years. Also, license plates must be replaced every three years. There are also additional taxes levied by individual Mexican states. Tax reform has boosted non-oil revenues through the Fiscal Responsibility Act.

In Mexico, the sales tax rate VAT is a tax charged to consumers based on the purchase price of certain goods and services. Revenues from the Sales Tax Rate are an important source of income for the government of Mexico.

In terms of regulatory trends, there are 32 states in Mexico, each with their own regulatory environment. For instance, there are registrations and de-registrations (alta y bajas), road tax (tenencia), environmental inspections (verifaciones), and licensing fees (permiso de cargo).

Insurance is not mandated by law, but a comprehensive coverage package is a market standard for fleet. Many companies offer to pay the deductible at a first accident; subsequent payments are made by the driver.

Related: Commercial Fleet Market in Argentina Gains Strength

More Global Fleet

Proven Ways to Reduce Work Truck Downtime

The age-old problem of downtime will always be a reality, but with new strategies at hand, fleets have more ways to keep trucks on the road longer.

Read More →

The Top 300 Commercial Fleets

The Top 300 Commercial Fleets: See the List

Read More →

Cameras, Safety and Insurance: From Reactive Claims to Real-Time Prevention (Part 2 of 2)

Part Two: Commercial auto remains one of the most challenging and costly lines of coverage for fleet operators and insurers alike. Continue learning more about how to effectively address these issues from Onur Aksan, Enterprise Business Development Executive, Geotab

Read More →

Cameras, Safety and Insurance: From Reactive Claims to Real-time Prevention

Commercial auto remains one of the most challenging and costly lines of coverage for fleet operators and insurers alike. Learn more about how to effectively address these issues from Onur Aksan, Enterprise Business Development Executive, Geotab.

Read More →

Fleet Costs Are Rising: Here’s How Leaders Are Responding

Fleet leaders are under pressure to reduce costs, adapt to economic uncertainty, and make smarter decisions. See how peers across North America are responding with real data, proven strategies, and forward-looking insights. Download the 2026 Market Pulse Report to benchmark your strategy and uncover where you can gain an edge.

Read More →

Enterprise Fleet Management Surpasses 900,000 Vehicles in U.S. & Canada

Enterprise Mobility connects with mobility solutions around the globe

Read More →

Automotive Fleet's Guide to Fleet Electrification

Unlock the secrets to a successful transition to electric fleets with Automotive Fleet's comprehensive Fleet Electrification Guide!

Read More →

Sumitomo Rubber Industries to Acquire Viaduct

Viaduct will join Sumitomo as an independent subsidiary. Partnership strengthens global reach and accelerates AI-driven innovation for fleets and manufacturing.

Read More →

AfMA’s 2025 Education & Leadership Summit: 26 Years of Impactful Connection

Held in Sydney, the Australasian Fleet Management Association’s 2025 Summit marked ten years of growth as the event expanded its global reach and doubled down on practical, non-commercial fleet leadership programming.

Read More →