Tax Consequences Under Different Reimbursement Methods

As a general rule when considering total cost of ownership (TCO), employees with high-mileage needs should be provided with a company vehicle; those with low-mileage needs should have their job function reviewed to determine if personally owned vehicles (POVs) would produce the lowest TCO through a business reimbursement program.

by Janis Christensen

June 13, 2014

Photo courtesy of iStockPhoto.com.

11 min to read

Photo courtesy of iStockPhoto.com.

Today's leading organizations are leveraging multiple modes of transportation to minimize their total cost of moving people and delivering goods and services. Well-run organizations are integrating both employer- and employee-provided vehicles in fleet programs as part of their vehicle allocation methodology.

As a general rule when considering total cost of ownership (TCO), employees with high-mileage needs should be provided with a company vehicle; those with low-mileage needs should have their job function reviewed to determine if personally owned vehicles (POVs) would produce the lowest TCO through a business reimbursement program.

Ad Loading...

The fleet manager or other company leader should have authority over both programs to properly control costs and successfully provide fair, safe, and equitable transportation for all employees.

Rather than focus on the pros and cons between the different means of providing business transportation, we'll review the importance of understanding the differences between taxable and non-taxable business reimbursement plans for use of POVs.

In one case, reimbursement is considered income to the employee and must be included on his or her W-2 statement. As such, the reimbursement is subject to employment taxes, both for the employee and employer, and can include withholding taxes, FICA, and federal and state unemployment taxes. The employee has the option to deduct the business expenses personally, depending on the individual's tax situation.

In the second case, reimbursement is tax-free for both the employer and employee.

Employers should consider the advantages and disadvantages of each type of plan when deciding how to structure the reimbursement of employee business expenses.

Ad Loading...

Understanding Taxable Reimbursement Plans

Reimbursement plans that do not meet IRS guidelines to be tax free for the employee are categorized as "Non-Accountable Plans." These include flat-dollar allowances and cents-per-mile reimbursements that exceed reasonableness standards accepted by the IRS.

In these cases, the employer is responsible for including the reimbursement amounts as taxable income. The employee has the option to claim actual vehicle business expenses on his or her itemized tax return.

The advantage of this arrangement is that it minimizes the record-keeping responsibility of the employer and simplifies the administrative procedure; however, this convenience comes at a cost to the employer and employee.

Reviewing the Consequences of Taxable Reimbursement Plans

Ad Loading...

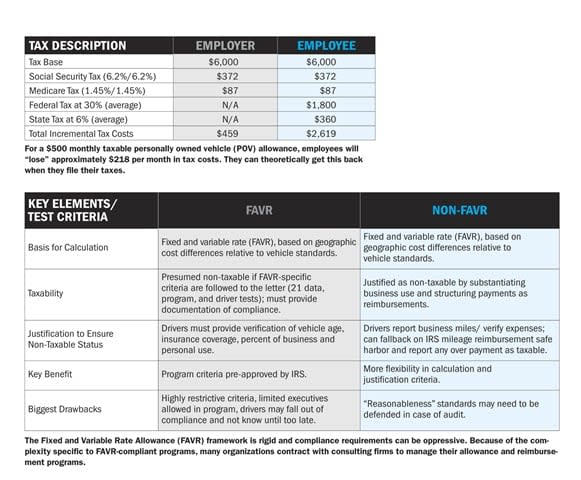

The table below illustrates the tax consequences to both the employer and employee for a $500 monthly ($6,000 per year) taxable POV allowance.

In the example, the employee's $500 monthly reimbursement produces a net amount of $282 per month (56 percent of the allowance). Theoretically, employees can deduct all business-related expenses and business mileage on their federal and state personal income tax returns and receive the incremental monthly tax cost of $218. Notwithstanding, this may not hold true in all cases.

For example, the employee must itemize deductions and a 2 percent of adjusted gross income (AGI) threshold must be met before the expense can be deducted. If the employee is married and files a joint income tax with a combined annual income, the allowable itemized deductions will be diminished. Even if the employee overcomes the AGI floor limitation, tax benefits may be curtailed by the alternative minimum tax, which disallows the deduction of "employee business expense" in its calculation. Finally, unlike employer-provided vehicles, any employee interest expense to finance the POV is not tax deductible.

With respect to the true cost to the employer, 107.65 percent of the allowance amount is actually paid and, in this example, reflects a total additional cost of $459 per year. Employers should utilize the fully burdened expense of a taxable plan when comparing costs against non-taxable reimbursement plans and company-provided vehicles.

It is also logical to presume that some employees may attempt to recover some or all of the "lost" monthly $218 tax cost back by inflating other business expenses.

Ad Loading...

Offering Non-Taxable Plans

As a result of the unfavorable tax implications, companies may elect to offer tax-free POV reimbursement programs to their employees. These include cents-per-mile reimbursement based on the IRS Standard Mileage Rate and tax-free structured allowance programs that qualify as IRS Accountable Plans. Employers should weigh the disadvantages of the additional paperwork associated with Accountable Plans against the added tax burden expense with the Non-Accountable Plans.

Using IRS Standard Mileage Rate

Many organizations use the IRS mileage rate because employers perceive it as easy, tax-exempt, and defensible. In reality, the Standard Mileage Rate is intended to be a deduction guideline for taxpayers who opt for a standard deduction in lieu of tracking business vehicle expenses diligently.

The rate is derived from weighting and blending cost factors from across the U.S. It is not representative of vehicle ownership and operating costs for any specific vehicle in any specific geographic area of the country. Some vehicle costs (e.g., insurance, financing, fuel, vehicle registration, and vehicle sales taxes) vary substantially by geographic area and can drive wide variances in vehicle ownership and operating costs between low- and high-cost locations, particularly those areas with higher insurance costs.

Ad Loading...

Therefore, depending on the types of vehicles driven and where employees are driving, the true per-mile ownership and operating costs for employees' vehicles actually may be greater than the IRS rate, particularly when fuel costs are volatile.

Fairness of IRS Standard Per-Mile Reimbursement Plan

Using the IRS Standard Mileage Rate for all drivers — regardless of territory type, location, or number of miles driven — is a common reimbursement method. On the surface, the per-mile reimbursement approach appears to work best, because treating employees equally is often perceived as synonymous with treating employees equitably; however, when employees have widely varying travel or expense patterns, they are treated inequitably under a uniform reimbursement structure.

For example, assume two drivers (Driver A and Driver B) work for the same employer, live in the same community, own the same year/make/model vehicle, purchase the same type of insurance coverage at comparable prices, and incur the same type of miscellaneous ownership expenses (tax and registration fees). Further, assume both drivers are reimbursed using the 2014 IRS Standard Mileage Rate of 56 cents per mile for business miles. Driver A is assigned to service a territory that has a high density of business within a relatively confined area and, therefore, drives 12,000 business miles per year. Driver B, however, is assigned to service a broad territory and must drive further between business calls, traveling around 24,000 business miles per year.

At 56 cents per mile, Driver A will receive $6,720 for POV reimbursements in a year, while Driver B will receive $13,440. If we presume both drivers incur the same fixed annual ownership costs of $5,000, Driver A is reimbursed $1,720 or 14 cents per mile in addition to the $5,000, while Driver B receives $8,440 or 35 cents per mile plus $5,000. It is reasonable to presume that Driver B experiences a higher rate of vehicle deprecation due to the greater number of miles driven; however, it is unlikely as large as the disparity of 21 cents-per-mile difference between Driver A and Driver B. Instead, Driver B is overpaid due to the inequity of a fixed cents-per-mile plan.

Ad Loading...

Meanwhile, employees such as Driver A may attempt to maximize reimbursement for mileage and vehicle expenses if they feel they are not being adequately reimbursed. One common way is to overstate business mileage.

An often-quoted statistic claims that companies switching from a POV reimbursement program to a company-provided vehicle program experience declining reported business mileage by an average of 30 percent. This is not because employees drive less — the business miles no longer generate reimbursement monies, so employees are reporting actual miles.[PAGEBREAK]

Data source: Janis Christensen

Customizing IRS Accountable Plans

The IRS provides broad guidelines for calculating and documenting non-taxable vehicle allowances and reimbursements to substantiate "amount, time, place, and business purpose of expenses."

The Accountable Plan must be based on geographic-specific fixed and variable costs customized by driver or group and paid periodically. An Accountable Plan allowance program combines a flat dollar amount (based on ownership costs) with a per-mile reimbursement (derived from actual operating costs). If structured according to IRS guidelines, the allowances are non-taxable and no withholding or fringe-benefit value reporting is required.

Ad Loading...

To be deemed non-taxable, a vehicle mileage reimbursement or allowance program must meet three criteria:

Business Connection: The reimbursements must be for deductible business expenses of the employer that are paid or incurred by the employee in the performance of services as an employee.

Substantiation: The employee must be required to substantiate the elements of amount, time, use, and business purpose of the reimbursed expenses to the employer. To accomplish this, the employee should submit an account book, diary, log, statement of expense, trip sheet, or similar record supporting each of these elements and entries should be recorded at, or near, the time of the expenditure. The employee should also supply any supporting documentary evidence.

Employer Reimbursement: The employee must be required to return to the employer any excess of reimbursements over substantiated expenses within a reasonable period of time. Under IRS Safe Harbor rules, the employee may provide substantiation within 60 days or return unsubstantiated amounts within 120 days after an expense is paid or incurred. If the employer furnishes period statements (not less frequently than quarterly) of unsubstantiated expense, amounts substantiated or returned within 120 days of the statement will be considered returns or substantiated within a reasonable time.

Accountable plans must also adhere to the following guidelines:

Reasonably calculated, not to exceed the amount of the expenses or the anticipated expenses.

Provided on a uniform and objective basis with respect to expenses.

Periodically paid at a rate that combines a fixed rate and a variable rate.

Consistently applied in accordance with reasonable business practices.

Ad Loading...

Providing an IRS Template for Tax-free Accountable Plan

The IRS provides a template for an Accountable Plan known as a Fixed and Variable Rate Allowance (FAVR), which is merely an IRS-supplied template for an Accountable Plan; it is a set of suggested guidelines an employer can apply to an allowance and reimbursement approach to help ensure the approach will be presumed non-taxable via IRS Accountable Plan criteria. A FAVR plan is an optional non-taxable approach and is not mandatory. The basis for developing a FAVR-compliant plan is the same as an Accountable Plan, except the IRS provides specific guidelines.

FAVR guidelines include 21 data, program, and driver tests, which all must be met for the approach to be considered "FAVR compliant." FAVR has very specific parameters as to who can participate in/qualify for the FAVR approach, and how data can be applied in determining allowance and reimbursement amounts. For example, this data must be derived from a base locality, reflect retail prices, and be reasonable/statistically defensible approximating costs of standard vehicles. Most data elements have specific requirements:

Insurance: Employees must maintain vehicle insurance consistent with levels used in deriving allowance amount.

Vehicle Age: Age of employees' vehicles must not exceed depreciation schedule used to derive amount of the allowance.

Vehicle Value: Cost for a calendar year may not exceed 95 percent of retail dealer invoice plus state and local sales or use taxes up to $28,200 for automobiles and $30,400 for trucks and vans (2014 values).

Minimum Mileage: 5,000 annual business miles.

Business-Use Percentage: Annual business mileage may not exceed 75 percent.

Enrollment: At least five employees in the program.

Management Employee Enrollment: Cannot exceed 50 percent of program enrollees at any time during the calendar year and enrollee cannot be a controlling employee of the corporation.

This framework is rigid and compliance requirements can be oppressive, particularly for companies and drivers unaccustomed to frequent and diligent mileage and vehicle data reporting and/or unfamiliar with a program that dictates the maximum age of their vehicle or levels of insurance they must carry. Because of the complexity specific to FAVR-compliant programs, many organizations contract with consulting firms to manage their allowance and reimbursement programs. A comparison of FAVR and Non-FAVR Accountable Plans is provided in the table below.

Ad Loading...

The following administrative tasks are common to both Accountable Plans:

POV Drivers: Identify qualifying drivers (FAVR) or assign driver tiers by miles and/or job (non-FAVR).

Data: Collect driver information, proof of license and insurance, validation of vehicle make/model and purchase price/value.

Validation: Verify driver-provided info (e.g., review registrations, compare against databases).

Benefits of Centralized Fleet Program

Well-run organizations integrate both company vehicles and POVs into their overall fleet program as part of the vehicle allocation methodology process. The fleet manager is an ideal candidate to have authority over both programs due to the numerous commonalities that exist between both strategies. Two primary areas of note are POV and company-vehicle-related risks associated with non-compliance with Sarbanes-Oxley (SOX) Act regulations and company liability under the theories of negligence or vicarious liability.

Sarbanes-Oxley Ramifications

Ad Loading...

Compliance with SOX is mandatory for all publicly traded corporations, which must establish processes to ensure honest corporate disclosure and greater accountability. A company's obligation for compliance does not diminish when POVs are used for business travel (versus company-provided vehicles) and non-compliance with IRS rules will likely indicate non-compliance with SOX.

Many companies rely on consulting firms to establish and maintain their FAVR program, but it is the company's responsibility to be certain their selected vendor is in compliance. Thus, it is recommended that companies obtain a certificate of IRS regulation compliance (and, thereby, SOX) from the consulting firm and validate compliance through standard auditing practices.

Risk Management Considerations

If an employee creates liability in a POV, the negligent employee's personal auto policy responds in a primary position to the loss. When the employee's auto policy limits are exhausted, the company's auto policy will respond and the courts could find the company liable under the theories of negligence or vicarious liability. To mitigate risk associated with any POV program, companies should consider the following guidelines:

Restrict employees who are allowed to conduct business with POVs.

Review employees' motor vehicle records (MVRs) before they are allowed to drive the POV.

Require proof of business insurance with a minimum of $300,000 combined single limits and validate coverage is renewed on a regular basis.

Be named as an additional insured on the employee's personal auto policy.

Require the employee's auto insurance to include sufficient uninsured/underinsured coverage, rental reimbursement, and towing.

Require POV insurance to be obtained from a financially solvent insurer.

Ad Loading...

Inspect employees' POVs on a regularly scheduled basis to assure vehicles are properly maintained and safe to operate.

Investigate all crashes and provide training to prevent future crashes.

Establish a safety policy for POV drivers.

Provide training for POV drivers.

Janis Christensen, CAFM, is director of corporate fleet consulting at Mercury Associates. She can be reached at jchristensen@mercury-assoc.com.

Fleet drivers face constant visual, cognitive, and environmental interruptions the moment they hit the road. From roadside chaos to mental fatigue and digital overload, today’s biggest driving risks often come from outside the vehicle itself.

FLASH Weather AI has launched a first-of-its-kind hail prediction model capable of forecasting hail size and arrival time at 1-kilometer resolution up to 55 minutes ahead, giving fleets and insurers critical time to prepare for severe storms.

As litigation risk rises, vehicles are increasingly targeted. This Coca-Cola bottler shares how it’s reducing exposure through driver training, technology, and a proactive risk management approach.

From identity management to third-party certifications, the right technology partner should make security easier to manage. Here are the three building blocks that fleet managers need to stay in control as connected systems scale.

Distracted driving remains one of the most persistent risks in fleet operations. New approaches focus on removing mobile device use entirely while adding real-time safety support.

As distraction risks evolve, fleets are turning to smarter, more connected technologies to better understand what’s happening behind the wheel. Part 2 explores how these tools are helping identify risky behaviors and improve visibility across operations.

Distracted driving is often measured by what we can see—phones in hand, eyes off the road. But what about the distractions we can’t? A recent incident raises a bigger question about awareness, attention, and why subtle risks so often go unnoticed.