Robust Economy in Mexico Drives Growth in Fleet Market

Presently, there are 34 million vehicles in operation in Mexico, of which 34 percent of them are commercial vehicles. The majority of large fleets operating in Mexico are owned or leased by multinational companies.

Mexico has a population of 122 million people living in 32 states. It has a diversified economy ranked 14th in the world with a gross domestic product (GDP) of $1.2 trillion USD.

The growth in the Mexican economy is not only with local businesses operating within the domestic market, but also by significant foreign investments, as a multitude of international companies are building (or will be building) all-new plants in Mexico to export products to the U.S. and other countries in South America, Europe, and Asia.

Ad Loading...

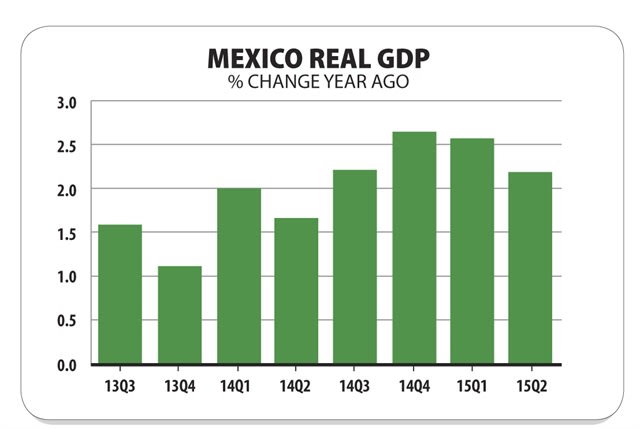

Fleet Market in Mexico

Presently, there are 34 million vehicles in operation in Mexico, of which 34 percent of them are commercial vehicles. The majority of large fleets operating in Mexico are owned or leased by multinational companies.

FERNANDEZ

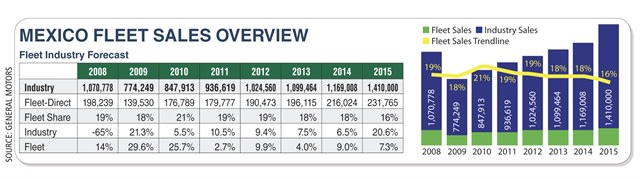

“Annual new-vehicle sales have been increasing in Mexico. Historically, fleet sales in Mexico averaged between 17 and 20 percent. In 2015, it is expected that fleet sales will account for 20 percent of all automotive sales in Mexico,” said Gerardo Fernandez, fleet director for GM Mexico.

Source: General Motors

During the first six months of calendar-year 2015, the fleet industry in Mexico experienced strong growth.

“It’s growing almost 10-percent more versus the same period last year. This is important to highlight because during the year we struggled with some economic conditions. For example, the low prices in oil, and the more than 25-percent depreciation of the Mexican peso against the U.S. dollar,” said Fernandez.

The peso depreciation is an important factor affecting the Mexican auto industry, especially when compared with new-vehicle prices. On average, new-vehicle prices have only increased a little more than 5 percent.

Ad Loading...

“Different companies are analyzing this, and they are deciding whether to add buys to their regional fleet plan,” said Fernandez.

Fleet Vehicle Preferences

In Mexico, manufacturer fleet pricing is based on buying volume. Fleet vehicles can only be purchased through dealers using a courtesy delivery system. Typically, vehicles are delivered out of stock.

The subcompact is the most popular vehicle segment in the overall automotive market in Mexico, accounting for more than 30 percent of new-vehicle sales in the country. The next most popular vehicle segment is compact cars, at 30-percent market share. The multiple-use vehicle segment is the third most popular vehicle segment at more than 19 percent of the new-vehicle market.

“In terms of vehicle acquisition trends in the Mexican fleet market, the most important segments for fleet are, in order, B-Car, C-Car, and Pickup-D. These are the most important vehicle segments for commercial fleet; however, the sales volumes in these segments have decreased versus the year prior. Growing in popularity with fleets are Pickup-E and SUV-B,” said Fernandez.

The key vocational markets for local sales is the B-Car, which is the highest volume vehicle segment in Mexico. “Approximately 37-38 percent of total fleet sales, for the industry are allocated in this segment,” said Fernandez. “It’s important to mention the Chevrolet Aveo has been the leader for almost four consecutive years. This is also the top-selling vehicle in Mexico, not only for fleet, but for the retail industry as well.”

Ad Loading...

The second most popular vehicle segment is the C-Car, which represents around 14 percent of total fleet sales in Mexico.

One of the most important segments is the fast-growing Pickup-D segment, which is now the third most important vehicle segment in the Mexican market. GM recently launched the S10, which is being imported into Mexico from Brazil.

Funding Options

The traditional asset-driven culture in Mexico is moving toward a more “focus on core business” approach, which favors the outsourcing of non-core activities, such as car fleet ownership and management, even in the public sector.

“In the past five years, full-service leasing is becoming very popular among corporate and government fleets,” said Fernandez.

Most fleet leases in Mexico are open-end leases. Closed-end leases are not very popular and are typically more expensive than open-end leases. The preferred option for most medium and large corporations is purchasing. The reason is that corporations operating in Mexico are cautious about interest rate risk. Typically, fleet funding is based on a floating interest rate; however, fixed rates are available, which are tied to the Prime rate.

Ad Loading...

Vehicle lease terms are typically 36 months, with some lease terms extending to 48 months. Most leases are written on fixed rate contracts insulating lessees from future run-ups in rates.

In the Mexican fleet market, there are two distinct fleet leasing products available:

The traditional “American” open-end model based on transferring risks to the lessee, and operational expenses (such as taxes, insurance costs, maintenance, and repairs) are likewise passed as they occur. Open-end leases convert into financial leasing under Mexican generally accepted accounting principles (GAAP). Residual value risk is borne by the lessee and interest rates are typically variable.

The second lease funding option is the “European” closed-end model – also known as “renting” or “full-service leasing.” It is based on a monthly installment payment, which includes all operational expenses based on an agreed mileage and all risks are borne by the lessor. Interest rates are kept fixed over the period of the lease.

Embryonic Fuel Management

Source: Deutsche Bank, IEA

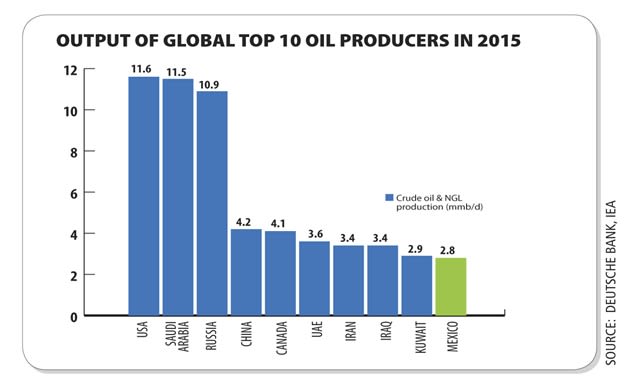

Mexico has significant oil reserves and is the 7th largest oil producer in the world. There is only one fuel supplier in Mexico, the state-owned oil company PEMEX, one of the largest oil companies in the world.

Fuel in Mexico is controlled by PEMEX, which owns and manages all gasoline stations within the country. As a result, gasoline and diesel pump prices are very stable. Due to its monopoly, PEMEX has no incentive to negotiate on prices or provide services, such as payment by credit card. But, this will start to change in January 2016 as new legislation takes effect, which is designed to make Mexico a completely open market by 2018.

Ad Loading...

In Mexico, there is limited coverage by fuel management companies and these typically include only pre-paid options. Not all fuel stations accept credit cards, with most cards being pre-paid.

Many company drivers receive a budget to purchase fuel.

Vehicle Remarketing Practices

At end of service, most corporations give drivers the option to buy the vehicle, regardless of the kind of acquisition.

“In Mexico, almost all off-lease vehicles are sold back to the driver at an extreme bargain price because, historically, there has been no formal used-vehicle market, auctions, or wholesalers,” said Fernandez.

Approximately 95 percent of fleet passenger vehicles are sold to drivers.

Ad Loading...

Stringent Regulations

There are 32 states in Mexico, each with their own regulatory environment. For instance, there are registrations and de-registrations (alta y bajas), road tax (tenencia), environmental inspections (verificaciones), and licensing fees (permiso de cargo).

Insurance is not mandated by law, but a comprehensive coverage package is a market standard for fleet. Many companies offer to pay the deductible at a first accident; subsequent payments are made by the driver.

Fleet Maintenance Trends

GM has launched its “Fleet Services” initiative in Mexico, homologating prices across a range of dealers.

Several fleet leasing companies have initiated certification programs for their preferred maintenance network.

Some companies require their drivers to pay for maintenance and repairs.

Taxation and Interest Rates

Source: Economy.com

Current interest rates and taxation rates are having a favorable impact on fleets. Two years ago, a new tax law was implemented by the Mexican government, which favorably impacts leasing.

Ad Loading...

Taxes are a major factor in fleet purchases. “There is a federal tax ‘tenenica,’ which is 10 percent of the original cost of the vehicle paid over four years. Also, license plates must be replaced every three years. There are also additional taxes levied by individual Mexican states,” said Fernandez.

Surge in Mexican Auto Production Capacity

Source: Bank of America Merrill Lynch

Mexico is the 8th largest automotive producer in the world, surpassing Brazil in 2014. What has accounted for the dramatic growth in the past two decades has been a huge volume of foreign investments in Mexico by a variety of automotive OEMs establishing brand-new factory operations in the country, mainly for export purposes.

A key factor driving this investment in the Mexican automotive sector is that the country has 10 free-trade arrangements, which, besides the U.S., encompasses 45 countries within the European Union, South America, and Asia.

Currently, the automotive sector accounts for more than 17 percent of Mexico’s manufacturing sector.

In the past decade, expansion of the automotive sector surged in Mexico. In 2014, more than $10 billion in investments was committed during the calendar-year. For example, in August 2014, Kia Motors announced plans for a $1 billion factory in Nuevo León. At the time, Mercedes-Benz and Nissan were already building a $1.4-billion plant near Puebla, while BMW was planning a $1-billion assembly plant in San Luis Potosí. In addition, Audi began building a $1.3-billion factory near Puebla in 2013.

Ad Loading...

In December 2014, GM announced plans to invest $3.6 billion in Mexico to double its production capacity at its plants around the country. The investment will be directed toward expansion projects at GM’s four manufacturing complexes in Mexico. GM is planning to make the investments through 2018 — on top of $1.4 billion already invested in the past two years. GM produces about 647,000 vehicles annually in Mexico — 80 percent of which are exported.

One unintended consequence to the rapid pace of investment is that it has exceeded the capacity of Mexico’s infrastructure to handle this increased business activity. For instance, this increased business volume has constrained the haulaway auto transport industry and ports infrastructure capability, which has increased lead times to export vehicles. The deficiency in port infrastructure is delaying the loading of ships departing for South America and the off-loading of ships arriving from Asia.

About the Author

Mike Antich is editor of Automotive Fleet magazine, published by Bobit Business Media, and conference chair of the Global Fleet Conference held in North America. He can be reached via e-mail at mike.antich@bobit.com.

Part Two: Commercial auto remains one of the most challenging and costly lines of coverage for fleet operators and insurers alike. Continue learning more about how to effectively address these issues from Onur Aksan, Enterprise Business Development Executive, Geotab

Commercial auto remains one of the most challenging and costly lines of coverage for fleet operators and insurers alike. Learn more about how to effectively address these issues from Onur Aksan, Enterprise Business Development Executive, Geotab.

Departmentally assigned vehicles often create hidden costs through underutilization, poor visibility, and increased administrative burden. This white paper explores how shared motor pool strategies help fleets reduce costs, improve accountability, and optimize vehicle utilization.

Fleet leaders are under pressure to reduce costs, adapt to economic uncertainty, and make smarter decisions. See how peers across North America are responding with real data, proven strategies, and forward-looking insights. Download the 2026 Market Pulse Report to benchmark your strategy and uncover where you can gain an edge.

Viaduct will join Sumitomo as an independent subsidiary. Partnership strengthens global reach and accelerates AI-driven innovation for fleets and manufacturing.