Wholesale Market Keeps the Industry Flowing

The supply of used vehicles entering the market in 2013 is increasing, creating a “pretty solid” environment for resale. The remarketers of tomorrow may face some challenges.

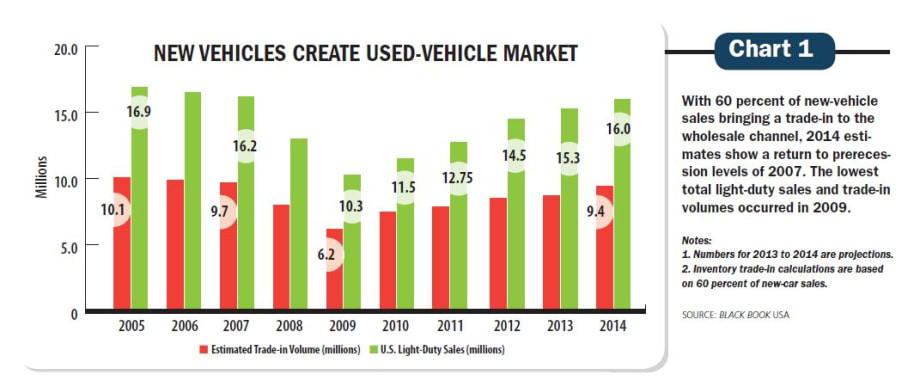

With 60 percent of new-vehicle sales bringing a trade-in to the wholesale channel, 2014 estimates show a return to prerecession levels of 2007. The lowest total light-duty sales and trade-in volumes occurred in 2009.

Notes:

1. Numbers for 2013 to 2014 are projections.

2. Inventory trade-in calculations are based on 60 percent of new-car sales.

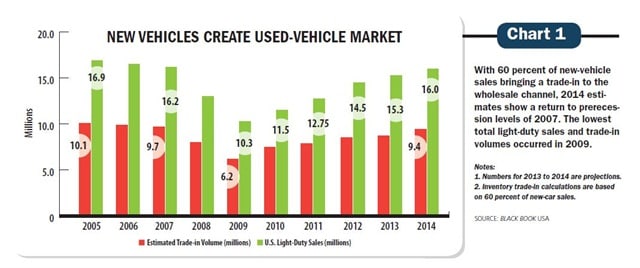

With 60 percent of new-vehicle sales bringing a trade-in to the wholesale channel, 2014 estimates show a return to prerecession levels of 2007. The lowest total light-duty sales and trade-in volumes occurred in 2009.

Notes:

1. Numbers for 2013 to 2014 are projections.

2. Inventory trade-in calculations are based on 60 percent of new-car sales.

Whether you are a franchised or independent dealer, a large or small fleet management company, or part of the lending community, the wholesale market and channels that support the distribution of used vehicles continues to adjust.

Note: You can click the image at the beginning of this article to view all of the charts referenced within. All charts are courtesy Black Book USA.

There is no question that the transaction by a consumer who purchases a new or used vehicle from a franchised or independent dealer in a retail environment is the starting point leading to the values at the wholesale level. And, one must also distinguish the differences within the wholesale channels.

As a fleet remarketer, you are a solid source of good, used vehicles that normally do not compete directly against new sales. Your opportunities are with a focused used buyer and finding the correct wholesale channel to supply that market. The cost is not just what one dealer will offer for a trade-in, or what he or she will ask on the auction block or in an online listing. It entails much more, such as buy and sale fees, transportation to and from the auction or lot, and also necessary reconditioning.

Black Book continues to see more and more vehicles purchased sight unseen, or at least only “seen” through an online condition report. This enables a vehicle to be offered to more potential buyers and, in some cases, offered even before it is taken out of service (with a fleet or as a rental unit).

Reporting the market values has evolved significantly over time to now include the traditional physical and emerging electronic lanes . The speed in changing the market values is almost expected to be instantaneous as there is more transparency in the wholesale market activity and market values than ever before. There still remain opportunities for arbitrage, but many of those opportunities disappear quickly due to the industry transparency, and will then show up as another opportunity.

Since the 2008 economic recession, the positive movement in the market has made heroes out of remarketers while creating the challenges for those remarketers of tomorrow. Risk analysts must understand there is currently a changing used market with even more adjustment coming.

Now that the Seasonally Adjusted Annual Rate (SAAR) has climbed consistently to about 15.3 million, the supply of used vehicles into the market in 2013 is increasing and we are not too far from prerecession levels. With Black Book expecting new-car sales levels to hit 16 million in 2014, we will be just short of prerecession levels for new sales and ultimately used market volume levels and values.

[PAGEBREAK]

Reviewing Past Trends

When looking at used vehicles currently in the three- to six-year-old vehicle age group, the more recent depreciation should bring a big “thank you” for the efforts of the fleet remarketing specialists, but not the hero status of 2011 and 2012.

In almost every view one takes comparing the 2012 and 2013 calendar years , depreciation is greater than more recent time periods.

Annual depreciation from Aug. 1, 2011, to Aug. 1, 2012, represented a very strong market of only -12.1 percent. For the same time period in 2012 to 2013 that change was slightly higher at -13.4 percent. For a three month period of May 1, 2012 to Aug. 1, 2012/2013, the change was -3.4 percent in 2012 and -3.6 percent in 2013.

When looking at a solid used market, no matter what year, the retention is much better than prerecession levels of -15 percent to -18 percent annually and -4.5 percent to -4.8 percent for quarterly periods.

Even with larger depreciation in more current times, the market is still termed as “pretty solid.” As a remarketer or risk analyst, one might want to understand the reason for the larger levels of change and whether to expect that trend to continue or even increase. At least for the vehicles in the fleet remarketing efforts, there is not a direct competition to the more recently advertised and incentivized new car sales, which pushes the one- and two-year-old models even further down.

The used-vehicle market has always been driven by supply and demand. Finding that one vehicle that sends the market over the cliff and tips the scales to excess supply is the unknown. During and since the recession years, the demand for solid used vehicles over new vehicles became more prevalent. Lower acquisition costs, very reasonable finance rates, and also longer loan terms all got the attention of consumers. The only challenge was supply being so tight due to fewer vehicles being sold and thus fewer traded in at the new car stores and even fewer finding their way into the wholesale market.

Nearing the end of the recession period those trade-ins also became significantly older, with upwards of 20,000 to 50,000 more miles on the odometer than desired.

As new-car sales continue to increase, we are now beginning to see better supplies from trade-ins along with more of these trade-ins actually making their way into the wholesale channels instead of all staying on the franchised retail lots. The age of the trade-in is starting to ease back down to a slightly newer model as well. This is great news for the buyer, while not as enticing for the seller or remarketer.

[PAGEBREAK]

Looking to the Future

Is there a market or segment that should fare better during the next few months or year, or one to be more wary of in depreciation levels?

Looking at some historical movement in values some of the better retention vehicles will come from truck, van, and utility units. During the past year from Aug. 1, 2012, to Aug. 1, 2013, except for the most recent monthly period with the cars at -1.4 percent and the trucks at -1.3 percent, the quarterly period at -4 percent for cars and -3.3 percent for trucks and then the full year cars at -15.5 percent and the trucks at -11.4 percent the truck depreciation has been less than for the cars. One year ago, from Aug. 1, 2011, to Aug. 1, 2012, the same depreciation difference occurred for the yearly period, -13.7 percent for cars and -10.5 percent for trucks, while the quarterly period was slightly more for trucks at -3.4 percent for cars and -3.5 percent for trucks. The most recent monthly level of depreciation was the same for both segment types.

Another way to look at depreciation/retention is by actual segment type. During the past year, 14 of the 24 segments tracked by Black Book depreciated less than prerecession levels. Twelve of those were truck related, with the top four being the three pickup segments and the compact SUVs, all at less than -6 percent.

Only one segment declined greater than expected from traditional levels: entry mid-size cars at -20.5 percent. This is a competitive segment with around 16 current models and 56 players in the three smallest, more fuel-efficient segments, which are not only fighting the competition, but trying to get interest while gasoline prices remain fairly stable and well below record high levels.

So, what’s ahead for the fleet and commercial remarketing industry?

Fortunately, the signs of an improving economy are still at the forefront. The housing, construction, and service industries are the drivers behind improved truck values. Even if gasoline prices increase somewhat, these vehicles will continue to do well.

If we are faced with much higher gas prices, and by much higher we mean $5 per gallon and remain at that level, Black Book feels the depreciation of the entry level cars, compact cars, entry mid-size cars, and the upper mid-size cars will be at the low end of depreciation and be some of the more in-demand and popular units. The two mid-size car segments continue to be a solid portion of the fleet market.

“Fleet churn” is very active in today’s market and, unlike the rental market, commercial fleet users are getting their needs met with new models and inventory while maintaining values at solid levels.

The very mature and solid wholesale channels will keep remarketing efforts on an even keel. Add in the various tools and technology available that tracks, reports, and analyzes the used market from progressive companies such as Black Book and commercial fleets will be able to handle the challenges of a changing used market.

More Remarketing

Manheim Index Shows Used-Vehicle Wholesale Prices Up 2.1% in June

The market is seeing stronger appreciation in older used vehicles this year, and the most affordable segments have been among the year’s best performers.

Read More →

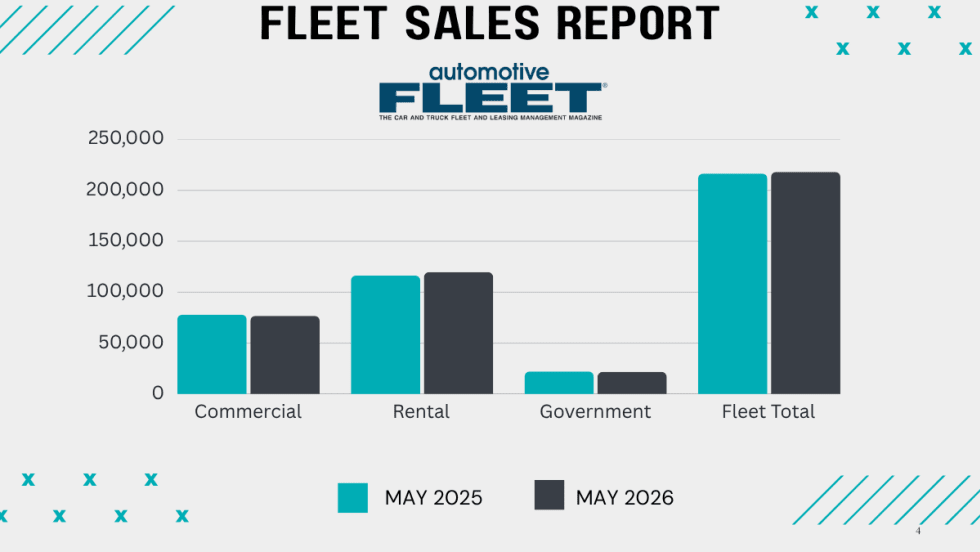

Commercial Fleet Sales Contribute To June, YTD Gains

The fleet sector has boosted its vehicle purchases at a reliable pace in the first half of this year compared with 1H 2025.

Read More →

Used Vehicle Prices Climb Higher As Sales Pace Slows

The higher prices at used retail reflect strong wholesale values earlier in the spring, particularly for older, more affordable vehicles.

Read More →

Wholesale Used Vehicle Market Sustains Moderate Rise In Values, Prices

Trends continue to normalize after a strong start to the year, as consumers contend with higher gas prices in the coming summer months.

Read More →

Commercial Fleet Sales Still Lead Sectors Despite May Mini Dip

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

How Connected Vehicle Data Is Lifting Fleet Resale Values

A vehicle health score could improve the value of fleet vehicles at remarketing. The path to a universal standard is forming, and fleets that understand the process early will be better positioned when it arrives.

Read More →

Wholesale Used Vehicle Prices Slightly Up In April

The Iranian conflict and rising gas prices inject much uncertainty into the future wholesale used vehicle markets, as higher gas prices soak up spendable income from vehicle buyers.

Read More →

CAR2026: James McKinley Wins Value Champion of the Year

James McKinley of City Rent a Truck was named the inaugural Fleet Value Champion at the CAR Conference for his data-driven approach to fleet lifecycle management and vehicle remarketing.

Read More →

CAR2026: Eric Autenrieth Wins Remarketer of the Year

Eric Autenrieth was recognized at this year's CAR Conference as the Remarketer of the Year.

Read More →

CAR2026: Lawrence Knapp Wins Consignor of the Year

Lawrence Knapp won the Cosigner of the Year award at this year's CAR Conference.

Read More →