Fleet Depreciation Rates Decrease in CY-2012

The ongoing tight supply of used vehicles has kept resale values strong and reduced fleet depreciation rates. This is expected to continue through CY-2013. A return to traditional resale values isn’t expected until CY-2014.

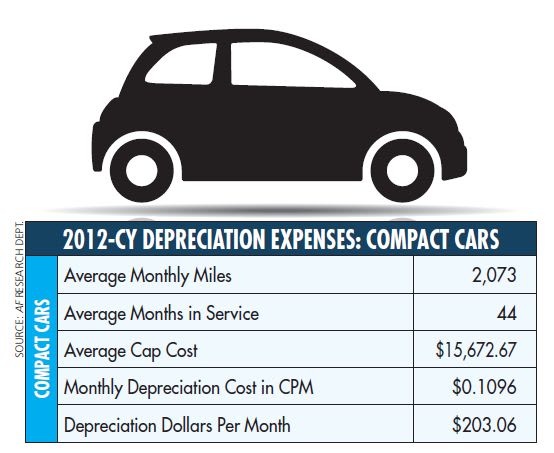

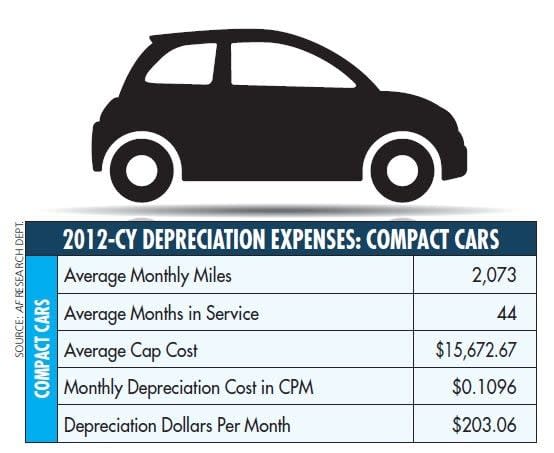

While monthly miles, on average, went up for compact cars in 2012, monthly depreciation in both cents per mile (CPM) and dollars per month dropped compared to 2011.

The ongoing strong used-vehicle market continued to benefit commercial fleets by exerting downward pressure on fleet vehicle depreciation rates during calendar-year (CY) 2012.

Three fleet management companies (FMCs) participated in this year’s annual fleet depreciation study providing data and commentary as to fleet depreciation trends in CY-2012 compared to CY-2011. The participating FMCs were ARI, LeasePlan USA, and PHH Arval.

“PHH analyzed several car and light-truck segments, including cars, crossovers, SUVs, pickups, and vans. Overall, average percentage depreciation (as a percentage of capitalized cost) declined from 2010 to 2012 (year-to-date as of October 2012), but results varied by vehicle segment,” said Bill Cieslak, vice president, North American remarketing for PHH Arval. “Cars, crossovers, and vans experienced a drop in percentage depreciation of roughly 5 to 6 percentage points from 2010 to 2011, but, then increased 2 to 6 points from 2011 to 2012, although none of these segments have returned to their 2010 percentage depreciation level.”

While monthly miles, on average, went up for compact cars in 2012, monthly depreciation in both cents per mile (CPM) and dollars per month dropped compared to 2011.

This was borne out by other participating FMCs. Regardless of whether data was examined from the standpoint of net resale gains or cents-per-mile expense, all pointed to decreases in depreciation for CY-2012, as observed by LeasePlan USA.

“Using the cents-per-mile measure to normalize the effects of varying monthly miles driven between years, depreciation expense has decreased substantially, between 5 and 15 percent in segments where terms/service life were similar and sufficient data existed in both years,” said Becky Langmandel, asset risk and analytics manager for LeasePlan USA.

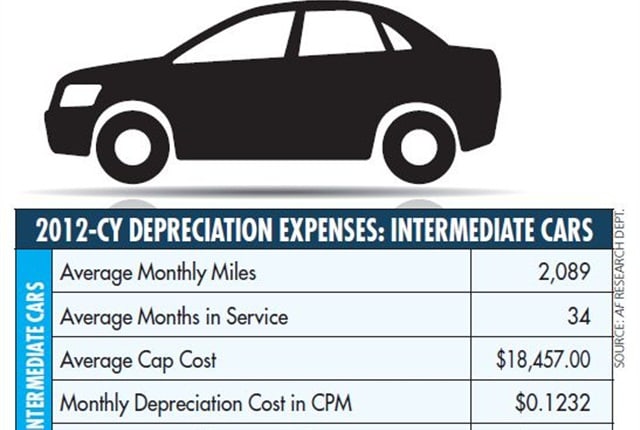

For intermediate cars, miles also edged up and cents per mile dropped compared to 2011. Dollars per month decreased as well.

All participating fleet management companies reported decreases in vehicle depreciation in 2012; however, the percentage of depreciation varied by vehicle segment. The segments experiencing the greatest decrease in depreciation were intermediate and compact cars.

“The light-truck, full-size van, minivan, and sport/utility vehicle segments reported modest gains in the resale market, compared with the even more robust gains realized in the compact/intermediate car segments,” said Bob Graham, vice president, vehicle remarketing for ARI. “Year-to-date in 2012, vehicle depreciation continued to decrease slightly in comparison to 2011 and 2010. This is attributed to the strong used-vehicle market and lower acquisition costs for better-equipped vehicles.” The light-truck and SUV segments experienced the least depreciation reductions.

“Average percentage depreciation held steady for pickups from 2010 to 2011 and declined slightly from 2011 to 2012. The SUV segment experienced a 5-percentage point increase from 2010 to 2011, and a further 3-percentage point increase from 2011 to 2012. This was partly attributable to a more aged (i.e., higher months in service) portfolio of SUVs sold in 2011 and 2012,” PHH Arval’s Cieslak said.

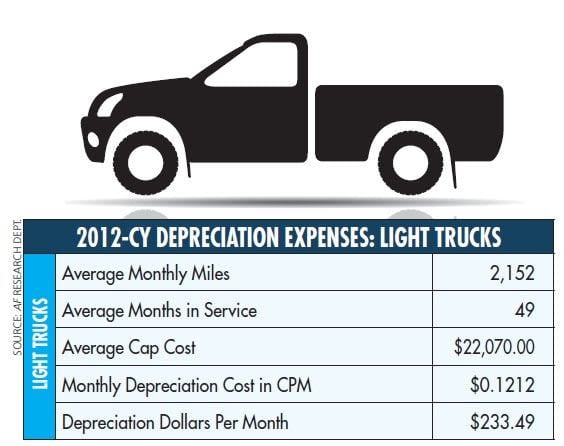

Across the board, light trucks saw their depreciation expenses decrease in 2012 compared to 2011. In addition, the average months in service fell from 56 months to 49 months.

[PAGEBREAK]

Impact of Replacement Cycles

Following the economic downturn in 2008-2009, many fleets extended months in service for vehicles in operation, delaying their traditional replacement cycle, which impacted depreciation.

“The extended replacement has contributed to decreased depreciation rates, as measured by percent depreciation per month, in every segment. The decline in average percent depreciation per month was 12 basis points for pickups and vans, and ranged from 14 to 32 basis points for car, crossover, and SUV segments,” Cieslak said. “Overall, the larger decline occurred from 2010 to 2011, followed by a smaller decline from 2011 to 2012.”

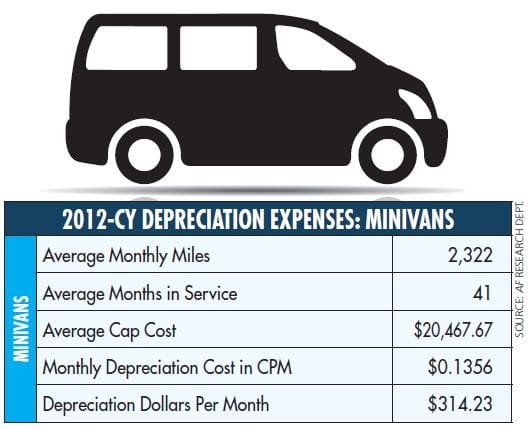

There were few changes in the minivan segment from 2011. Months in service edged down slightly, as did the average cap cost and monthly depreciation.

However, more fleets are slowly returning to their traditional replacement cycles. But, those vehicles coming out of service today are older with higher miles.

“Fleets appear slow in returning to standardized cycling patterns. The impact of extended cycling, downsizing, and rightsizing strategies implemented in previous years are now evident. Vehicles are traveling higher miles, on average, than previous years, with the exception of the sport/utility vehicle segment, which remains relatively flat,” Graham said. “The number of months in service has increased on average for most segments, with the exception of intermediate cars and full-size vans, which experienced slight reductions. The increase in months in service and mileage was largely offset by the current strong resale values. As a result, fleets experienced overall decreases in depreciation in 2012.”

Survey data varied slightly by fleet management company, influenced primarily by the types of clients in their portfolios.

“On average, for each vehicle segment, PHH clients’ replacement cycling patterns showed a modest increase in average service life each year from 2010 to 2012, roughly four months overall, with the exception of SUVs. The SUV segment showed a much larger shift in replacement cycles; the average service life for SUVs sold in 2012 was 12 months longer than vehicles sold in 2010,” Cieslak said.

LeasePlan reported its client fleets shortened replacement cycles in CY-2011, with this trend continuing through this year.

“Therefore, the average service life in months is relatively stable year-over-year for the high-volume segments,” Langmandel said.

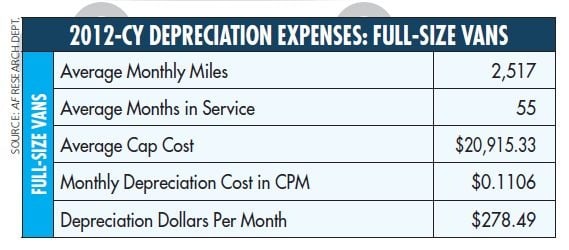

Full-size vans saw their average monthly miles increase by more than 10 percent in 2012 compared to 2011, while their monthly depreciation rates decreased.

Wholesale Resale Market Status

The key reason for the ongoing strength in the used-vehicle market continues to be the lower inventory of units available for resale.

“The continued tight supply of used vehicles in 2012 kept resale values strong and reduced depreciation rates overall, albeit not by as much as during the peak of the resale market in 2011,” Cieslak said.

The question is, how much longer will resale values remain strong?

“The strong resale market continues to positively influence overall depreciation for fleet vehicles in 2012. The present short supply of used vehicles, OEM streamlined production schedules to better control surplus inventory, new-vehicle equipment specifications, and overall pricing have all contributed to higher-than-normal resale values,” Graham said. “This trend is expected to continue throughout 2013. The market is expected to return to more normalized values in early 2014.”

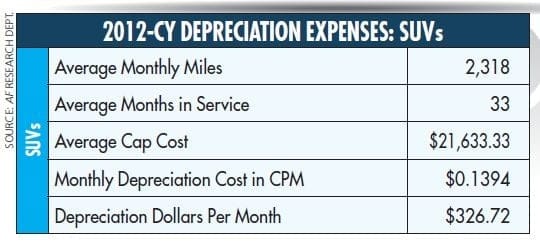

In the SUV segment, months in service and miles per month went up slightly compared to 2011. The good news, monthly cents-per-mile depreciation costs and dollars-per-month depreciation costs were lower in 2012.

As any remarketer will tell you, it is difficult to predict future resale values with certainty; however, there is a seasonality and cyclicality to the wholesale market, when resale values are traditionally higher or lower during the calendar-year.

“Our clients understand the used-vehicle secondary market is cyclical in nature and that they have the ability, in many cases, to capitalize on higher market levels by adjusting replacement cycles and disposing units when the market is more favorable due to a supply/demand imbalance,” said Langmandel of LeasePlan USA. “We communicate to our clients that the market is increasingly volatile and there may be more downside than upside, relative to the historical market averages.”

[PAGEBREAK]

Acquisition Cost Trends

Acquisition costs are a crucial component in determining a vehicle’s net depreciation value. Despite decreases in OEM incentives, vehicle capital costs have remained relatively consistent over the past two to three years.

“In 2012, most vehicle segments experienced moderate price increases. Pricing for vehicle value has never been better, as OEMs are offering products with better fuel economy, more features, and enhanced safety features,” said Graham of ARI. “Vehicles now offer more value for fleet dollars spent, with better impact on overall resale value due to the robust resale market at present. All of this is reflected in decreased depreciation seen to date.”

Traditionally, higher acquisition prices for new vehicles influence overall demand for used vehicles among retail buyers.

“In general, when new-vehicle prices increase by more than overall inflation, the demand for used vehicles increases, which favors demand in the supply/demand ratio, and, in turn, affects an increase in used-vehicle prices,” said Cieslak of PHH Arval. “In 2012, new-vehicle prices did not increase significantly, relative to overall inflation, and therefore had a minimal impact on the used-vehicle market. New-vehicle capitalized cost is only one of many factors that impact the used-vehicle market and depreciation.”

However, there is not necessarily a set formula to how higher acquisition prices impact resale values.

“From an individual model perspective, increasing new-vehicle transaction prices do result in an increase in the wholesale prices of one-year-old used vehicles, and two-year olds, and so on. While the upward impact is measureable, it is not as impactful on a percentage basis as the decline in used-vehicle prices caused by lower new-vehicle invoice prices or increases to consumer new-vehicle incentives,” said Langmandel of LeasePlan USA.

Depreciation Trends Forecast

What is the forecast for fleet vehicle depreciation trends for the 2013 calendar-year?

“Over the short term, if the market follows its usual seasonal pattern of lower demand going into the end of the year, we will begin to see an increase in demand and prices heading into Q1 2013 as dealers position their inventory for the ‘tax refund’ season. In addition, although the impact of Super Storm Sandy is not yet known with regards to vehicle losses, after Hurricane Katrina there was a short-term supply/demand imbalance that resulted in an increase to used-vehicle pricing for a few months, and, therefore the start of 2013 may not follow the usual seasonal trends,” Langmandel said. “Longer term, toward the end of 2013, we expect the secondary market to ‘normalize’ as the higher supply from the past two to four years of increasing new-vehicle sales continues to hit the auction lanes and higher numbers of trade-ins from increasing new-vehicle sales are disposed at auctions.”

Many remarketers, likewise, foresee resale values ultimately softening.

“The combined trend of increased used-vehicle sales volume, increased new-vehicle sales, and the improved affordability of new vehicles due to the very low cost of loans will have used-vehicle values trending toward a more normalized level in relationship to the cost of new vehicles. We expect this trend will continue throughout 2013 and into 2014,” Cieslak said.

But, for the near term, most remarketing experts foresee ongoing strength in used-vehicle resale values.

“Barring any major economic disruptions, for the remainder of 2012 and 2013, we expect to continue to see higher than normal resale values for most of the vehicle segments. In the first quarter of 2014, however, we expect to see the start of a return to more normalized resale conditions. As the supply of used vehicles increases, resale values will decrease, and effective depreciation will start to increase, returning to more historically normalized values,” Graham said.

This view was echoed by Cieslak.

“Used car and truck values reached their apex late in 2011. As levels of new-vehicle sales continue to improve, additional trade-in vehicles will provide dealers and auctions with increased used-vehicle supply. In addition, the supply of off-consumer-lease vehicles will continue to grow over the next three years. These will result in changes to the supply/demand ratio of used cars and trucks (favoring supply), thereby providing for a modest increase in vehicle depreciation rates,” Cieslak said.

Fleet managers should be especially cautious when setting up lease depreciation rates for vehicles that will be coming out of service in 2015-2016 or later.

“Clients should exercise caution when looking at the present resale values when setting their depreciation for new units going into service. Depreciation should not be based on historic resale values, but should be determined from anticipated resale value at time of turn in,” Graham said.

More Leasing

Mike Albert Fleet Solutions Names Marty Kuhn CEO, First from Outside the Family

Kuhn has a theory of what sets the company apart from larger FMCs: depth of partnership over breadth of volume.

Read More →

Union Leasing Rebrands as Moventum Fleet Management

The name Moventum reflects the company’s position at the intersection of movement and momentum, with the guiding principle "Keep Work Moving."

Read More →

How Does a Mid-Major FMC Compete? Ask BBL Fleet

This Pittsburgh-based FMC built a technology-first culture, sustained double-digit organic growth, and expanded its Midwest footprint through a recent acquisition. How did it happen?

Read More →

What’s Really Happening in Fleet Supply Right Now

Fleet supply has improved, but not everywhere. Merchants Fleet’s Charles Matthew explains where constraints still exist, what risks are emerging, and why fleets shouldn’t wait to place orders.

Read More →

These Edges Are Measured in Inches — Matt Dyer on Fleet’s New Normal

The Merchants Fleet CEO contends that fleets that drive the business win the inches. In 2026, every one of them counts.

Read More →

Who Gets a Company Car? (In 2026 and Beyond)

As costs rise and scrutiny increases, fleets are refining criteria that govern eligibility for company-owned vehicles.

Read More →

DriveItAway Holdings, Free2move Launch Operations In Nine Cities

The co-branded program with Stellantis’ mobility division scales up leasing and financing options nationwide with more cities to come online in 2026.

Read More →

AFLA 2025 Conference in Pictures

Drawing over 640 attendees, the 2025 AFLA Annual Conference was held Sept. 14-17 at the JW Marriott Marco Island Beach Resort in Florida.

Read More →

DriveItAway, Free2move Partner to Expand Vehicle Access for Dealers

The arrangement enables franchise dealers to offer flexible lease-to-own programs with no credit checks, no down payments, and no long-term commitments.

Read More →

New Survey: How Well Are FMCs Serving Fleets? We Want Your Input

Fleet managers: Share your experience to help benchmark fleet management companies’ service, strategy, and support.

Read More →