Auto Market Forecast for 2024: The Old Normal

Cox Automotive welcomes a return to normalcy after four years of everything but normal, with nothing in the data suggesting vehicle market surges in any direction.

In the wholesale market, Manheim operations are expected to experience constrained growth with a volume increase of less than 1%. While the volumes of repossessions, rentals, and off-lease vehicles are expected to increase compared to the previous year, they are still likely to remain below pre-pandemic levels.

Photo: Cox Automotive

For the U.S. auto market, the word that will likely sum up 2024 is “normalcy,” according to Cox Automotive’s Forecast: 2024 released Jan. 3.

Powered by data insights, Cox Automotive developed five themes that offer a collective vision and valuable perspective on the road ahead for the U.S. auto industry. Running throughout the five themes is a welcome return to normalcy after four years of everything but normal, with nothing in the data suggesting surges in any direction, as the industry witnessed in 2021 and 2022.

“A decade from now, when we look back at the years immediately following the global pandemic of 2020, we’ll be awed by the dramatic swings and unprecedented circumstances the economy and auto market endured,” said Cox Automotive Chief Economist Jonathan Smoke in a news release. “To name a few, we saw historic appreciation in vehicle values, unimagined drops in supply, and interest rates moving from all-time lows to 23-year highs at an unforgiving pace. The past four years have been chaotic, even by auto industry standards, and have shifted many normal seasonal patterns out of whack, which adds to the difficulty of forecasting what comes next.”

For 2024, the Cox Automotive Economic and Industry Insights team sees the U.S. auto market being steered by five key themes.

1. Slow Growth Ahead, But It Sure Beats a Recession

Cox Automotive expects that the economy in 2024 will experience weak growth but will not experience a recession. High interest rates and declining inflation will likely continue, limiting consumer spending. Job and income growth may slow down. The labor market, which significantly contributes to vehicle sales in the U.S. market, is expected to weaken. However, unemployment levels will remain low enough to support a healthy auto industry. Meanwhile, wage growth may cool in 2024 but will stay above average.

Although the possibility of higher loan rates is still on the table, the expectation is for rates to come down from record highs in the year ahead. Although the downward trend likely won’t be significant, any decline will help improve vehicle affordability and relieve many households struggling financially.

Consumer debt is expected to grow slowly in 2024, while credit remains tight but stable. Consumer spending will likely slow down, but it should remain healthy enough to support constrained growth. Overall, the economy in 2024 may not be very exciting, but that is much better than the instability of a recession.

2. Vehicle Supply Is Back, Favoring Consumers, Placing Downward Pressure on Prices

In 2024, Cox Automotive is expecting new-vehicle inventory to rise, incentives to be higher and discounting to increase. New inventory is expected to reach pre-pandemic norms in 2024, with almost 3 million units available, or three times the amount during the chip shortage. Days’ supply will stay healthy.

New-vehicle transaction prices are expected to decline moderately. The increase in inventory is expected to lead to higher incentives and discounts; however, we won’t see incentives at the record highs reached in 2019 when discounting exceeded 10% of transaction prices and the new-vehicle market was pushed above 17 million units for a 5th consecutive year according to Kelley Blue Book counts. Market forces will likely exert downward pressure on vehicle prices, further improving consumer affordability.

With higher supply and lower prices, new-vehicle sales in 2024 are expected to gain over 2023, but market growth will be constrained, with an increase of less than 2% expected and the market new-vehicle market reaching sales of 15.6 million sales. Retail new-vehicle sales are forecast to be mostly flat in the year ahead, with fleet sales continuing to improve, although at a pace slower than 2023.

In 2024, the used-vehicle market is expected to grow by less than 1%. The total number of used vehicles sold is expected to reach 36.2 million, with 19.2 million vehicles sold via retail channels. Certified pre-owned (CPO) sales are expected to reach 2.7 million units, up 3% from 2023. Limited production between 2020 and 2022 has led to a scarcity of prime, available CPO products despite strong demand.

In the wholesale market, Manheim operations are expected to experience constrained growth with a volume increase of less than 1%. While the volumes of repossessions, rentals, and off-lease vehicles are expected to increase compared to the previous year, they are still likely to remain below pre-pandemic levels. As for price patterns, Cox anticipates a normalization trend, and predicts that 2024 will be the first year in five where we will experience fairly normal depreciation.

3. In 2024, Bid Farewell to the Seller’s Market

In 2024, dealerships will face the challenge of finding more efficient ways to protect their profit margins. The good news is that the margins for used vehicles and fixed operations are expected to remain relatively strong. However, sales departments for new vehicles will be challenged due to an increase in manufacturer’s suggested retail prices (MSRPs) and invoice prices – thanks to material and labor costs and a further shift to pricier models – and downward pressure on transaction prices. For many dealers, their profits will also be affected by higher floor plan costs and the need to invest in infrastructure to support the growing sales of electric vehicles. Heading into 2024, dealers are less optimistic about the future due to interest rates and weaker profits.

4. The 2024 Electric Vehicle Market Will Be the Year of More: Models, Incentives, Discounts, Advertising, and Sales Muscle

Demand for electric vehicles (EVs) is increasing, and dealers and manufacturers know that selling more EVs will require additional effort. The expectations for EV growth in the U.S. market have shifted from “rosy to reality” as sales increase, but customer acceptance of EVs isn’t keeping pace. Nevertheless, Cox Automotive expects 2024 to be the Year of More for EVs.

The Cox Automotive team expects that the automobile industry will fully acknowledge the need to convince average consumers of the benefits of electric vehicles. They also believe that many consumers may not easily be convinced. However, with more electric vehicle models available, more incentives, more discounts, more advertising, and greater sales efforts, Cox Automotive still expects that electric vehicle sales in the U.S. will exceed the 1-million-unit record set in 2023. Furthermore, electric vehicles, plug-in hybrids, and hybrids combined are likely to account for almost 24% of the market, with electric vehicles alone accounting for more than 10% of total sales.

Although fewer electric vehicles (EVs) may now qualify for the Inflation Reduction Act tax credits due to new guidelines, the federal incentives will still encourage consumers to purchase EVs. Furthermore, leasing of electric vehicles is expected to increase from about 20% to 25%.

Meanwhile, the used EV market is expected to be the fastest-growing segment of the wholesale/used-vehicle market.

5. Car Buying in America: Normal is Nice

After four years of anything but normal, Cox Automotive expects balance to return to the U.S. auto market in 2024. This will lead to more options, better deals, and easier access to online buying tools for American consumers and fleet buyers. Cox anticipates that 2024 will be the best year for car buyers since the pandemic.

Research suggests that Americans are emphasizing buying/owning personal transportation, in contrast to 2018, when consumers put a higher value on “access to transportation.” After tumbling in 2021 and 2022, satisfaction with the car buying process is expected to improve in the year ahead, thanks in part to better inventory and the return of discounting, but also from improved processes at the dealership that save time and make car buying more efficient.

Sales growth will be weak and constrained in 2024, which is a more normal state compared to the chaos of the past four years. Although the headline-making swings in economic trends are always interesting to analyze, such turbulence is rarely good news for businesses over the longer term. From the current viewpoint – and unless any unforeseeable events occur – the forecast for the automotive market in 2024 is fairly normal. This might not make headlines, but it should be a welcome relief for everyone involved.

More Remarketing

Manheim Index Shows Used-Vehicle Wholesale Prices Up 2.1% in June

The market is seeing stronger appreciation in older used vehicles this year, and the most affordable segments have been among the year’s best performers.

Read More →

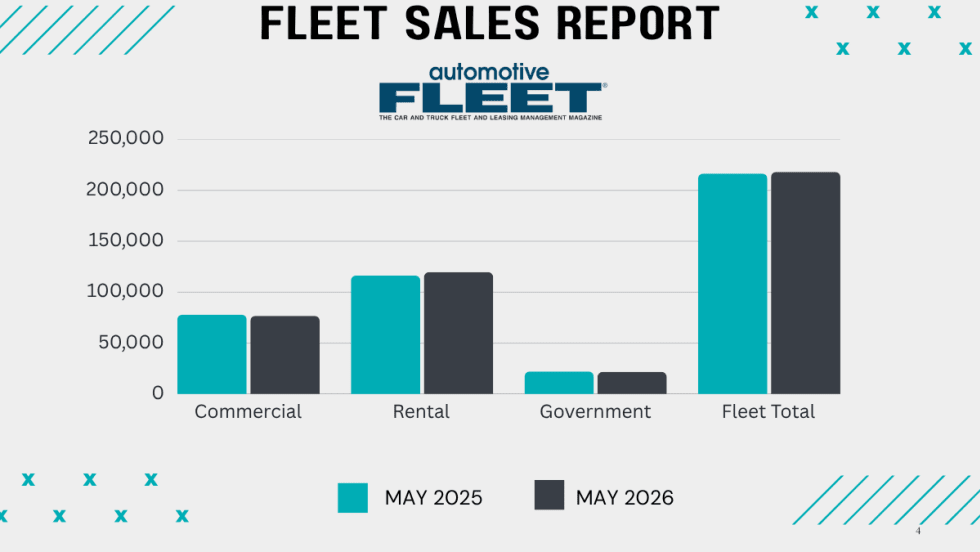

Commercial Fleet Sales Contribute To June, YTD Gains

The fleet sector has boosted its vehicle purchases at a reliable pace in the first half of this year compared with 1H 2025.

Read More →

Used Vehicle Prices Climb Higher As Sales Pace Slows

The higher prices at used retail reflect strong wholesale values earlier in the spring, particularly for older, more affordable vehicles.

Read More →

Wholesale Used Vehicle Market Sustains Moderate Rise In Values, Prices

Trends continue to normalize after a strong start to the year, as consumers contend with higher gas prices in the coming summer months.

Read More →

Commercial Fleet Sales Still Lead Sectors Despite May Mini Dip

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

How Connected Vehicle Data Is Lifting Fleet Resale Values

A vehicle health score could improve the value of fleet vehicles at remarketing. The path to a universal standard is forming, and fleets that understand the process early will be better positioned when it arrives.

Read More →

Wholesale Used Vehicle Prices Slightly Up In April

The Iranian conflict and rising gas prices inject much uncertainty into the future wholesale used vehicle markets, as higher gas prices soak up spendable income from vehicle buyers.

Read More →

CAR2026: James McKinley Wins Value Champion of the Year

James McKinley of City Rent a Truck was named the inaugural Fleet Value Champion at the CAR Conference for his data-driven approach to fleet lifecycle management and vehicle remarketing.

Read More →

CAR2026: Eric Autenrieth Wins Remarketer of the Year

Eric Autenrieth was recognized at this year's CAR Conference as the Remarketer of the Year.

Read More →

CAR2026: Lawrence Knapp Wins Consignor of the Year

Lawrence Knapp won the Cosigner of the Year award at this year's CAR Conference.

Read More →