Related: The Middle East Fleet Market: A Tale of Three Regions

Fleet Market in Brazil on the Road to a Long Recovery

The strongest vocational segments operating commercial fleet vehicles are pharmaceuticals, agribusiness, and food corporations. But the majority of fleets in Brazil are smaller, with the average fleet size around 100 units.

February 8, 2018

The General Motors Gravataí facility, officially known as Complexo Industrial Automotivo de Gravataí (CIAG, for short, or Automotive Industrial Complex of Gravatai, in English). Photo: GM.

10 min to read

The three pillars of the Brazilian economy are agribusiness, petroleum exports, and commodities. All three of these economic segments are seeing improvement, helping the Brazilian economy to grow 1.1% in calendar-year 2017, reversing the economic contraction that extended from 2014 to 2016.

Brazil is ranked as the ninth-largest economy in the world and the largest in Latin America, and the forecast is that its gross domestic product (GDP) will grow 3% in calendar-year 2018.

A critical sector in the Brazilian economy is its domestic automotive industry. There are already signs of a production upturn in Brazil. In the first quarter of 2017, output rose by 24% year on year, owing its growth largely to a 70% rebound in exports. But this is a tale of good news and bad news.

The good news is that the Brazilian automotive industry production increased to 2.4 million vehicles in 2017; but, the bad news is that this represents an idle capacity of 48% since the country’s automotive total production capacity is 5.1 million units. While the idle capacity is high, the silver lining is that Brazil can double automotive production without triggering inflationary pressures.

Domestic automotive production grew 15.2% and sales climbed 14.6% in November 2017 compared to November 2016.

New car and truck sales are expected to grow 9% in 2018, according to the country’s National Association of Motor Vehicle Manufacturers (known by the Brazilian acronym of ANFAVEA). The group’s prior forecast was 7.3%. If sales finish strong, the market might grow by double digits in 2018.

Automakers in Brazil produced about 249,100 new cars and trucks in November 2017, while sales in Brazil totaled around 204,200 vehicles, with the balance exported to foreign markets.

Heavy truck sales in Brazil may rise to 30% in 2018. This is up from the prior forecast of 20% growth.

Fleet Sales in Brazil

With a population of more than 210 million people, Brazil is the largest fleet market in South America. While fleet sales in Brazil are improving, total sales still remain down compared to prior years. The fleet market in Brazil continues to be tough, and all automotive manufacturers are using a variety of financial incentives to defend and bolster market shares.

As the economy improves, increased government revenues should stimulate increased government fleet sales to replace aging vehicle inventory that has built up in recent years during the decline in government fleet acquisitions.

ANFAVEA reported that light commercial vehicle (LCV) sales increased 4.7% year-over-year to 28,307 units and passenger car sales increased 15.5% year-over-year to 161,176 units in June 2017.

General Motors holds the status as Brazil’s top seller. Brazil is the largest market for Chevrolet outside of North America and GM is looking to further expand its service offerings to Brazilian fleets and retail buyers. In the fourth quarter of 2017, GM launched the 2018 Chevrolet Equinox in Brazil to supplement its product portfolio that also includes the Tracker and Trailblazer.

“GM has been a sales leader in South America for 17 consecutive years, and in Brazil it has returned to market leadership for the last two years, due to the excellent reputation the brand has in the region and by always innovating in order to better serve the consumer,” said Marcelo Tezoto, Senior Manager - Fleet Sales for General Motors. “In 2018, the main markets are expected to continue to recover and grow at double digits. GM, in particular, works to continue growing organically and sustainably bringing new products and technologies to companies and fleets.”

One positive aspect for future fleet sales in Brazil is that there is much interest from international investors looking for new projects, and Brazil has tremendous infrastructure needs, which indirectly translates into an uptick in truck and equipment purchases among subcontractors.

Size of the Fleet Market

Out of the approximately 4 million corporate vehicles in Brazil, more than half are located in the Southeast region of the country, which contains the major population centers, including Rio de Janiero and Sao Paulo.

The strongest vocational segments acquiring commercial fleets are pharmaceutical, agribusiness, and food companies. There is also a big demand for fleet vehicles by rental companies.

Examples of companies operating major fleets in Brazil are Danone, Honeywell, Kraft, Merck, Pirelli, and Proctor & Gamble.

But, the majority of fleets are smaller with the average fleet size in Brazil around 100 units.

One challenge facing fleet managers in Brazil is the geographic dispersion of fleets due to the country’s massive size. This geographic dispersion is compounded by poor road conditions and poor driver education.

The fleet sales focus by OEMs in Brazil is larger corporations, while smaller companies are serviced by the OEMs’ dealer network. There are 3,955 automotive dealers in Brazil.

Fleet Acquisition Preferences

Brazil imposes 35% import duties to “incentivize” commercial companies to buy vehicles that are produced locally. Not only does the 35% import duty apply to vehicles, but also to imported replacement parts that will be needed during the course of a vehicle’s service life.

In terms of fleet acquisition trends, the compact SUV is one of the fastest growing vehicle segments in the Brazilian market. The compact SUV segment is experiencing large incremental volume compared to last year. The SUV segment has doubled in size in Brazil in the last two years, and currently represents 15% of the market.

One factor impacting fleet acquisition in Brazil is the increase in new-vehicle prices.

Among the factors contributing to increased vehicle prices were a 15.8% increase to provide mandated safety equipment and the Inovar-Auto program that encourages more fuel-efficient technologies. The Inovar-Auto was approved by decree in October 2012 and is an incentive program using taxation exemptions to encourage automakers to produce more fuel-efficient vehicles and invest in the Brazilian domestic auto industry.

Other factors influencing fleet acquisition are high inflation, high interest rates, and tight credit availability that started to drive down sales in 2014 and through 2016. But, sales started to improve in 2017, with the forecast that this will continue in calendar-year 2018.

Fuel Price Trends

As a response to the 1973 oil crisis, the Brazilian government began promoting bioethanol as a fuel. This national initiative has been successful in helping Brazil reduce its dependence on imported petroleum. Historically, imported oil accounted for more than 70% of the country’s oil needs, but Brazil succeeded in becoming self-sufficient in oil in the 2006-2007 time frame.

Despite this, current petroleum fuel prices in Brazil are increasing. Gasoline prices in Brazil increased to US$1.24 per liter in December 2017. Historically, gasoline prices in Brazil averaged US$1.14 per liter from 1992 until 2017. Contributing to the increased cost of fuel are higher taxes on gasoline and diesel.

Flex-fuel bioethanol vehicles continue to be popular in Brazil. Companies prefer flex-fuel vehicles to mitigate the fluctuations in the price of petroleum fuels. Despite boasting the world’s highest rates of ethanol use, Brazil also has among the highest petrol prices in the Americas.

“Fuel prices in 2017 reached the top of historical prices in Brazil, which caused many fleets to downsize to more fuel-efficient vehicles,” said Tezoto.

Maintenance Trends

The third-party vehicle maintenance/service provider network in Brazil is not reliable in some parts of the country. But, OEM-franchised dealers do a good job in servicing fleets.

While parts availability has been an issue for some Brazilian OEMs, it is not so with General Motors.

The supply of spare parts for fleet owners and customers in general is good.

There is upward pricing pressure on maintenance cost inflation in Brazil, with an increase of around 8% in 2017.

Used-Vehicle Market

The used-vehicle market is very strong in Brazil, especially when compared to the new-vehicle market.

While new-vehicle sales volume declined in the 2014-2016 timeframe, the used-vehicle sales activity is very robust as Brazilian consumers seek lower-cost transportation.

The strength of the used-vehicle market is much better than the new-vehicle market.

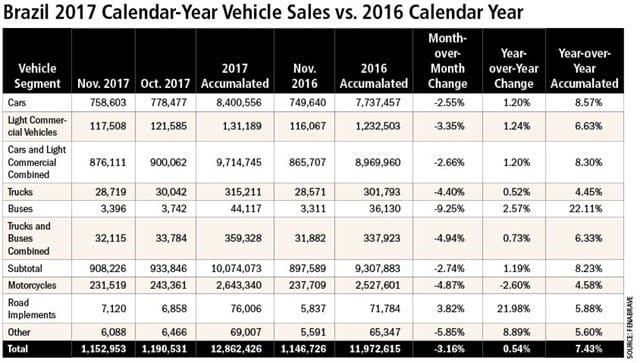

“The data obtained by Fenabrave - National Federation of Automotive Vehicle Distribution, an entity representing vehicle dealers in Brazil, show that the transactions of used vehicles, considering cars, light commercial vehicles, trucks, buses, motorcycles and road implements, in November, remained stable, amounting to 1,152,953 units, only 0.5% up on the same period of last year, when 1,146,726 units were traded,” said Tezoto.

Even though there has been a decrease in volume in the used-vehicle market versus last year, it is lower than the decrease in sales in the new-vehicle market. Vehicle depreciation rates vary and are influenced by engine displacement, size of the vehicle, brand, and other variables. A small vehicle has, on average, 10% depreciation after the first year. A large vehicle, such as an SUV, has around 26% depreciation after the first year of usage.

“In comparison with the 1,190,531 used vehicles sold in October 2017, the volume of November indicates a drop of 3.1%, due to the holidays that left the month with one working day less (20 days against 21 days). In the accumulated sales from January to November, the market of used maintained the tendency of constant growth. The 12,862,426 units transacted represent an advance of 7.4%, against the 11,972,615 units of the same months of 2016,” said Tezoto.

Considering only the car and light commercial vehicle segment, transactions in November 2017 totaled 876,111 units, up 1.2% compared to the same month last year.

“One less business day also hurt the segment, which showed a reduction of 2.6% compared to October, when 900,062 units were transferred. However, this market still maintained its pace of advance in the accumulated of the year, totaling 9,714,745 vehicles, 8.3% above the result of the same period of 2016,” said Tezoto.

“The scenario of the segment of used vehicles continues with bias of high, even with the small reduction in November, exclusively caused by the amount of working days. Of the total sales of light commercial vehicles sold, with up to 3 years of manufacturing, represented 17.4% in November, and 14.8% in the accumulated of the year,” said Tezoto.

Economic Trends & Interest Rates

There are a number of sales taxes specifically based on the type of vehicle and its powertrain. Taxation depends on the engine size, type of vehicle, and the segment to which it belongs. For instance, a vehicle with 1.0L engine has a lower taxation rate than a 2.0L engine. Pickup trucks have fewer taxes than passenger cars.

Additionally, following the seven interest rate cuts since November 2016, it may be that the reduced rates are beginning to assist auto sales.

Interest rates for auto financing reached the lowest level in two years, according to ANEFAC, the Brazilian financial association.

“In July, the average CDC (direct consumer credit) rate was 2.15% per month (29.08% per year). The level is the lowest since August 2015, when the rate was 2.14% per month (28.93% per year). In comparison with June 2017, when the CDC interest rate was 2.17% per month, the reduction was 0.92%. The CDC has the lowest rates among all credit modalities for individuals. The reduction in vehicle financing rates is accompanied by a downward trend in interest rates in general. This can be explained by the constant reduction of SELIC (floating-rate), according to ANEFAC. The entity expects interest to continue falling in the coming months because of low inflation,” said Tezoto. “In Brazil, interest rates affect the acquisition capital of the vehicles, either through acquisition by the final customer or via fleet management.”

There is still volatility in the market in Brazil, making it difficult for fleet management. It is difficult to predict the long-term interest rates and vehicle residual values. Even though the economy is expected to be on the positive side again this year, fleets are still struggling with economic volatility.

Real interest rates are still very high. They’re about 12% a year on the long term. Inflation is coming down, which is good, but the real interest rate is still very high, one of the highest worldwide.

Then there is the global concern about whether the U.S. President Donald Trump will scrap the North Atlantic Free Trade Agreement (NAFTA). The President pulled out of the planned Trans-Pacific Partnership Agreement, through which Chile, Peru and Mexico had all hoped to increase exports, and may act to raise trade barriers on imports from other parts of Latin America. This could dampen export hopes.

Subscribe to Our Newsletter

More Global Fleet

Proven Ways to Reduce Work Truck Downtime

The age-old problem of downtime will always be a reality, but with new strategies at hand, fleets have more ways to keep trucks on the road longer.

Read More →

Sponsored•July 23, 2026

The Top 300 Commercial Fleets

The Top 300 Commercial Fleets: See the List

Read More →

Cameras, Safety and Insurance: From Reactive Claims to Real-Time Prevention (Part 2 of 2)

Part Two: Commercial auto remains one of the most challenging and costly lines of coverage for fleet operators and insurers alike. Continue learning more about how to effectively address these issues from Onur Aksan, Enterprise Business Development Executive, Geotab

Read More →

Cameras, Safety and Insurance: From Reactive Claims to Real-time Prevention

Commercial auto remains one of the most challenging and costly lines of coverage for fleet operators and insurers alike. Learn more about how to effectively address these issues from Onur Aksan, Enterprise Business Development Executive, Geotab.

Read More →

Sponsored•May 13, 2026

Why Fleet Managers Are Replacing Departmental Vehicles with Shared Motor Pools

Departmentally assigned vehicles often create hidden costs through underutilization, poor visibility, and increased administrative burden. This white paper explores how shared motor pool strategies help fleets reduce costs, improve accountability, and optimize vehicle utilization.

Read More →

Sponsored•May 6, 2026

Fleet Costs Are Rising: Here’s How Leaders Are Responding

Fleet leaders are under pressure to reduce costs, adapt to economic uncertainty, and make smarter decisions. See how peers across North America are responding with real data, proven strategies, and forward-looking insights. Download the 2026 Market Pulse Report to benchmark your strategy and uncover where you can gain an edge.

Read More →

Enterprise Fleet Management Surpasses 900,000 Vehicles in U.S. & Canada

Enterprise Mobility connects with mobility solutions around the globe

Read More →

Sponsored•October 14, 2025

Automotive Fleet's Guide to Fleet Electrification

Unlock the secrets to a successful transition to electric fleets with Automotive Fleet's comprehensive Fleet Electrification Guide!

Read More →

Sumitomo Rubber Industries to Acquire Viaduct

Viaduct will join Sumitomo as an independent subsidiary. Partnership strengthens global reach and accelerates AI-driven innovation for fleets and manufacturing.

Read More →