Related: The U.S. Commercial Fleet Market Continues to be Strong

The State of the Australian Commercial Fleet Market

Although acquisition costs are a key factor for vehicle selection decisions, fleet application, fuel economy, CO2 emissions, safety, and overall TCO continue to play important roles in the purchase decision-making process.

October 5, 2016

Chart courtesy of General Motors.

9 min to read

Graphic courtesy of istockphoto.com

There was volatility in the Australian fleet market in calendar-year 2015, as a result of global economic headwinds and the ongoing sluggishness in the commodity markets, which represents a sizeable segment of the Australian economy. These market conditions have prompted the forecast that fleet sales will continue to be flat through calendar-year 2016.

Australia has a strong economy that is mainly based on services and mining. It is the 12th largest economy in the world. The macroeconomic factors that drive automotive demand in Australia are the prevailing interest rate, finance availability, current and expected rates of general economic growth, and the level of government and consumer spending.

Two bright spots in the Australian economy are the rate of inflation and low interest rates.

“Inflation and official interest rates are at 2.0% and have been holding steady since June 2015. They remain historically low,” said Gary West, corporate sales manager for General Motors International in Singapore.

Australia’s key export is its resources, and China consumes much of those resources. During the boom in commodities demand (and prices) there was massive growth in the Australian mining industry resulting in an investment surge in the construction of new mines and natural gas facilities. This growth cascaded into the rest of the Australian economy. However, for the past several years, the extraction and mining industries have been buffeted by the slowdown in the Chinese economy, due to decreased demand and lower commodity prices. The price of Australia’s key commodities — such as iron ore, gold, and coal — remain, largely flat. As a result, the mining industry has implemented operational cost-cutting measures, which is affecting the number of vehicles the industry is purchasing. The slowdown in business activity in this segment has also impacted other business activity of other companies, similarly resulting in flat demand for fleet vehicles.

As oil prices have fallen, it has also put more pressure on liquefied natural gas (LNG) producers to contain costs. One reaction has been to cut back on staff and exploration dollars. The fall of crude oil prices has also strengthened the position of gasoline in Australia, in turn, significantly reducing the sale of liquefied petroleum gas (LPG)-powered vehicles, which had been experiencing significant growth over the past five years.

One area of caution is the construction industry. “The recent housing boom is cooling and may have implications for construction activity,” said West.

However, the Australian fleet market is broad based, and, while some sectors may be retrenching, other segments are expanding.

“The economy is in transition — from the mining boom and traditional manufacturing to more innovative, tech-focused industries,” said West.

Another positive aspect of the Australian economy is the increasing number of Australians who are gainfully employed.

“The government reported a low unemployment rate of 5.8% - 6.0% in January 2016,” said West.

Two market factors positively influencing the Australian economy are the exchange rate for the Australian dollar and interest rates. The Australian dollar has fallen to a level favoring export, and providing a much needed buffer for many resource sector exports. Current interest and taxation rates are favorable to fleets. But currency exchange rates are volatile and easily subject to change.

“Slowly recovering commodity prices and actions by other central banks globally are strengthening the Australian dollar — which may have a negative effect on economic recovery in Australia. In March 2016, the Australian dollar gained 12% from the January low of US$0.69,” said West.

Fleet Market Conditions

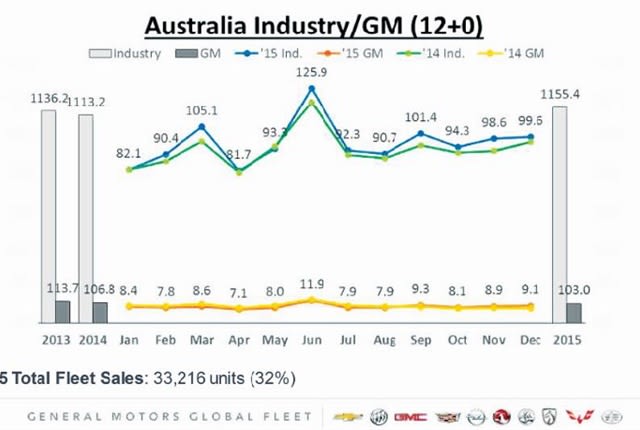

Australia had a new-vehicle sales record in CY-2015 with Australians buying 1,155,408 new passenger cars, SUVs, and commercial vehicles. SUV sales, in particular, continued to boom in 2015, with the segment now accounting for approximately 35% of the market, up from 31% in 2014. Light commercial vehicles held 17% of the market in 2015, roughly the same as in 2014. Government purchases declined 1.4%.

The top five brands in the Australian market, in terms of sales, are Toyota, Mazda, Holden, Hyundai, and Volkswagen.

“GM Holden posted three consecutive months of sales growth across Q4 to consolidate its position among the top three vehicle brands in the country, with both the Trax and Colorado model lines posting record results in 2015. Also, 2015 saw the launch of the Holden Astra hatch, Cascada convertible, and Insignia sedan, and VFII Commodore — the most powerful and advanced Commodore in the nameplate’s 37-year history,” said West. “This is part of Holden’s commitment to deliver 24 new models by the end of 2020 in order to build the best and most comprehensive model lineup in the brand’s history.”

Fleet Market Profile

Fleet sizes in Australia can range from small and medium enterprise fleets of fewer than 20 units to mega-fleets exceeding 1,000 vehicles. Larger fleets tend to be more prevalent in the fast-moving consumer goods, telecommunications, logistics, and utility industries. One key component of the Australian fleet market is tool-of-trade vehicles, known elsewhere in the world as utility or work vehicles. There is an ongoing trend among tool-of-the-trade companies to downsize by operating fewer vehicles in their overall fleets.

In Australia, the average fleet size ranges from 75 to 100 vehicles. The key fleet segments are:

Mining and construction industries, which primarily use light commercial vehicles (LCVs) and SUVs.

Telecommunications and utility industries, whose fleets are comprised of passenger cars and LCVs.

Daily rental, which primarily uses passenger cars.

Political subdivisions, such as federal, state, and local governments.

There are seven major fleet management companies in Australia. Recently GE Capital’s Custom Fleet was acquired by Element, a Canadian-headquartered company, which is now the largest fleet management company in North America. The other major players in the Australian fleet management market are LeasePlan Australia, sgfleet, FleetPartners, Orix Australia, FleetPlus, and Interleasing, which also operates an employee benefits business division offering novated lease administration called Maxxia.

The biggest challenge reported by Australian fleet managers is reducing total cost of ownership (TCO), as their senior management exerts ever-increasing pressure to contain fleet costs.

Chart courtesy of General Motors.

Vehicle Acquisition Trends

Procurement, as elsewhere in the world, has gained increased influence in fleet purchase decisions. One byproduct has been the growing trend to sole-source from a single OEM. Although acquisition costs are a key factor, fleet application, fuel economy, CO2 emissions, safety, and overall TCO continue to play important roles in the purchase decision-making process.

Large cars are expected to continue losing market share as TCO makes large passenger car operation more expensive. On the other hand, SUVs have gained market share, particularly over the past five years, due to their popularity among both retail and fleet drivers, stemming from the introduction of new products, aggressive prices, perceptions of social status, and safety.

In terms of sustainability initiatives, the Australian government is providing low-interest loans to corporate and government fleets, as well as not-for-profit organizations to purchase low-emissions vehicles. The program specifically excludes retail buyers. The government hopes that fleet buyers and lessees will increase the proportion of low-emissions vehicles operating on Australian roads, as well as lead the adoption of new technologies, such as electric and fuel-cell vehicles.

The AU$50 million program is funded through the Clean Energy Finance Corp. (CEFC) and provides corporate, government, and not-for-profit fleet buyers with access to favorable loan interest rates when choosing eligible low-emissions passenger and light-commercial vehicles. The program is designed to stimulate the sales of these vehicles to attain Australia’s 2020 greenhouse-gas-emissions-reduction target.

An emerging area of focus is urban mobility. “In November 2015, GM Holden provided Codha Wireless with two vehicles to demonstrate autonomous driving technology at a trial in South Australia. The trials were very interesting and it is fascinating technology we are monitoring very closely,” said West. “GM is taking a leadership position on urban mobility, and GM Holden will benefit from that.”

OEMs to Cease Domestic Vehicle Assembly

Dramatic changes are occurring in the Australian automotive industry. Ford announced it will stop assembling vehicles in Australia in October 2016. Similarly, Toyota and the GM subsidiary Holden announced that they will cease local vehicle production in 2017. When the last assembly plant closes, it will transform Australia into an import-only market.

Holden will transition to a national sales operation by the end of 2017.

Although Holden will cease local manufacturing, it has opened the spigot of its product pipeline for the introduction of new products into the Australian market.

“Holden will introduce 24 new models and 36 powertrain combinations by the end of 2020,” said West.

In 2016, Holden is bringing to Australia three European-sourced vehicles — the Holden Astra Compact, Cascada Soft Top/Cabriolet, and the Insignia Midsize.

“Holden will have a world-class Captiva replacement and two additional SUVs, on top of the next-gen Commodore and a true sports car. This will be Holden’s biggest and best range ever. GM wants Holden to win in Australia and Holden has a strong plan for the future,” said West.

Although Holden will cease local assembly, it will retain a significant engineering presence in the country and continue to operate the Lang Lang Proving Grounds in Victoria, to ensure Holden vehicles continue to be tuned for the unique driving conditions in Australia and New Zealand.

Australian Used-Vehicle Market

The key remarketing channels in Australia are auctions, wholesale tender, retail yards, and novated lease remarketing.

The estimated size of the used-vehicle market in Australia is approximately 3-million units sold annually. Growth in used-vehicle wholesaling has been 3.7% per year over the past five years, with growth for 2016-2019 forecast to be 5.2% per year.

The importation of used vehicles from Japan plays an important role in the Australian used-vehicle market. Used vehicles or “grey imports” strongly compete with the new-vehicle market in Australia. Within the last two years, the used-vehicle market segment of the country has seen an impressive growth. In 2015, more than 6,000 used vehicles were imported into Australia from Japan.

Growth in Novated Leases

One unique funding method in Australia is the novated lease. A novated lease allows companies to improve salary vehicle packaging for staff, while transitioning away from “benefit” company-supplied lease vehicles. Essentially, it is an individual employee lease, but paid for by the client company via a pre-tax salary deduction from the employee. The tax income and goods and services tax (GST), purchasing, and disposal benefits for the employee are significant, while the client company holds no responsibility for the vehicle if the employee should leave the organization at any stage.

Salary packaging/novated leasing is a growing segment for the fleet user/chooser as fleets downsize and take their assets off the balance books. In the past, employers traditionally only offered novated leases to their middle or senior managers. Now, the trend is to include all staff. Some companies are using novated leases as an employee recruitment tool.

While novated leasing has distinct advantages for businesses looking to reduce risk and responsibility on discretionary benefit vehicles — a common trend over the past 10 years — it offers substantial benefits in motivating salary packaging and engagement for all staff within an organization, creating fleet growth potential far in excess of the traditional company vehicle fleet.

Editor's note: This article first appeared online in the Q1 - Q2 Global Fleet Market Conditions supplement magazine June 2016.

Subscribe to Our Newsletter

More Global Fleet

Proven Ways to Reduce Work Truck Downtime

The age-old problem of downtime will always be a reality, but with new strategies at hand, fleets have more ways to keep trucks on the road longer.

Read More →

Sponsored•July 23, 2026

The Top 300 Commercial Fleets

The Top 300 Commercial Fleets: See the List

Read More →

Cameras, Safety and Insurance: From Reactive Claims to Real-Time Prevention (Part 2 of 2)

Part Two: Commercial auto remains one of the most challenging and costly lines of coverage for fleet operators and insurers alike. Continue learning more about how to effectively address these issues from Onur Aksan, Enterprise Business Development Executive, Geotab

Read More →

Cameras, Safety and Insurance: From Reactive Claims to Real-time Prevention

Commercial auto remains one of the most challenging and costly lines of coverage for fleet operators and insurers alike. Learn more about how to effectively address these issues from Onur Aksan, Enterprise Business Development Executive, Geotab.

Read More →

Sponsored•May 13, 2026

Why Fleet Managers Are Replacing Departmental Vehicles with Shared Motor Pools

Departmentally assigned vehicles often create hidden costs through underutilization, poor visibility, and increased administrative burden. This white paper explores how shared motor pool strategies help fleets reduce costs, improve accountability, and optimize vehicle utilization.

Read More →

Sponsored•May 6, 2026

Fleet Costs Are Rising: Here’s How Leaders Are Responding

Fleet leaders are under pressure to reduce costs, adapt to economic uncertainty, and make smarter decisions. See how peers across North America are responding with real data, proven strategies, and forward-looking insights. Download the 2026 Market Pulse Report to benchmark your strategy and uncover where you can gain an edge.

Read More →

Enterprise Fleet Management Surpasses 900,000 Vehicles in U.S. & Canada

Enterprise Mobility connects with mobility solutions around the globe

Read More →

Sponsored•October 14, 2025

Automotive Fleet's Guide to Fleet Electrification

Unlock the secrets to a successful transition to electric fleets with Automotive Fleet's comprehensive Fleet Electrification Guide!

Read More →

Sumitomo Rubber Industries to Acquire Viaduct

Viaduct will join Sumitomo as an independent subsidiary. Partnership strengthens global reach and accelerates AI-driven innovation for fleets and manufacturing.

Read More →