Why Element Wants to Buy the Fleet Businesses of GE Capital

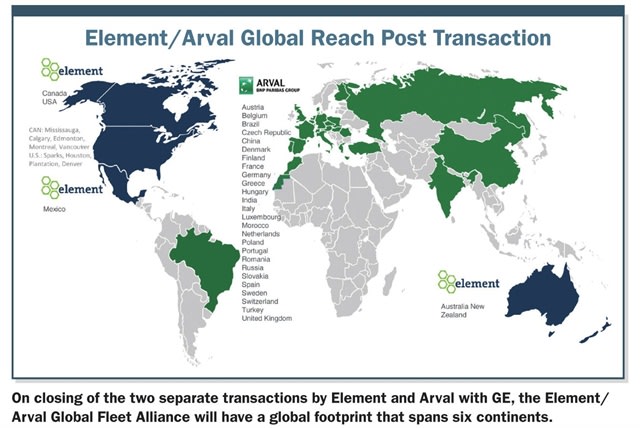

Element Financial Corp. has reached a definitive agreement to buy GE Capital's fleet assets in the U.S., Mexico, Australia, and New Zealand. Separately, Arval will acquire the European portion of GE's fleet business.

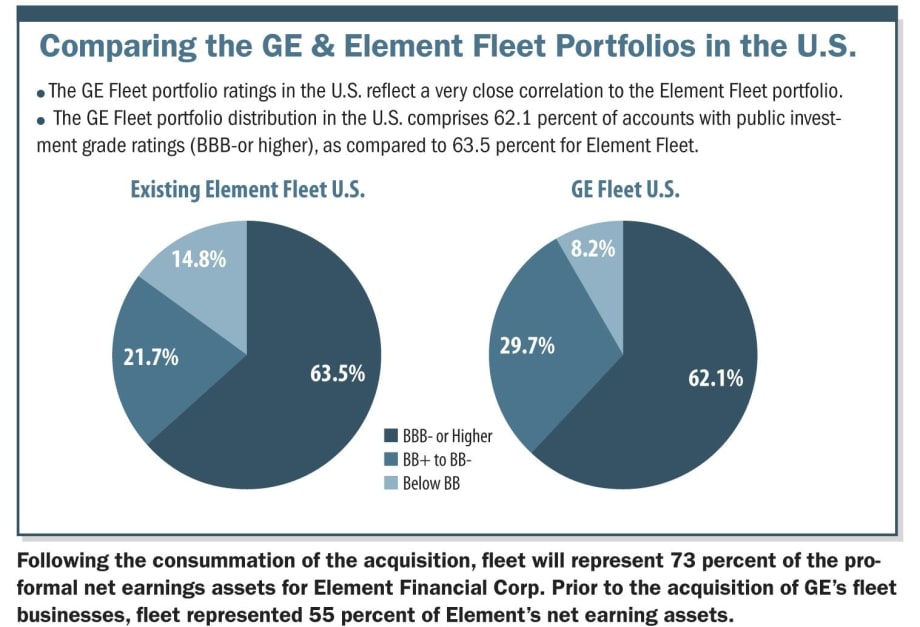

General Electric Co. agreed to sell a segment of its fleet management business to Element Financial Corp. for $6.9 billion. Specifically, Element will acquire GE Capital's fleet assets in the U.S., Mexico, Australia, and New Zealand.

Separately, GE signed a memorandum of understanding with Arval, a subsidiary of BNP Paribas, to sell its European fleet business, which includes 160,000 vehicles in 12 European countries. The assets in Japan are not included in either of the announced agreements.

The U.S. and Mexico portion of the agreement with Element is expected to close in the third quarter, and the Australia and New Zealand part in the fourth quarter.

This will be the second fleet acquisition Element has made with GE. In 2013, it bought GE Capital's Canadian fleet business, and created a Canadian-U.S. partnership. In an unrelated acquisition, Element purchased the North American fleet management business of PHH Corp. in 2014.

Nullmeyer

To learn more about Element's fleet strategy, Automotive Fleet interviewed Brad Nullmeyer, president of Element Financial Corp.

Automotive Fleet: Why did Element buy the fleet businesses of GE Capital and how will it fit with the recent acquisition of PHH?

Nullmeyer: The genesis of Element Fleet started back in 2012 with the purchase of TLSI (TransportAction Lease Systems). We supplemented that in June 2013 with the purchase of GE Fleet in Canada and put those two companies together.

We followed that in 2014 with the acquisition of PHH, which gave us the North American platform we wanted, because previously we just had the Canadian platform. We were in partnership with GE in Canada at the time, meaning we were managing the Canadian business and they were doing our U.S. referral business.

The PHH platform is very important for us. In addition to giving us the North American platform, it gave us a great relationship with Arval on a global basis.

We strongly feel there's a consolidation in the fleet industry that will serve as what we're calling the "catalyst for innovation."

We believe the combination of these two companies will establish one of the world's leading fleet management companies. We have strengths that complement each other — both the global reach and the vision we share around connected vehicles, predictive analytics, deep data dives, and managing driver behavior. We can use that catalyst for innovation to reach the goal, which is improved and deeper customer service and products for our customers.

The combination of those two will give us the platform that will allow us to accelerate the development and deployment of these next-generation analytics and fleet service tools, which we think are really required in this industry. We were a player in the fleet industry in a previous company (Newcourt Credit Group) many years ago. We like the fleet business a lot. We think, with the connected driver and increased use of technology, that we can really innovate the fleet industry, which, in some cases, people say, has been a sleepy industry, with sleepy growth rates.

We're going to eliminate that perception by innovating and providing exceptional levels of service and products for our customers that each of these companies by themselves could not individually accomplish.

We truly believe you need scale to be able to invest the necessary amount of dollars and research into the development of new fleet products to deploy to a large customer base.

We need the global reach — which we have in an unmatched way with this acquisition and our deeper relationship with Arval — to provide to customers the global product offering many of them want.

We particularly like GE's U.S. operation being complementary with PHH in the U.S. We did have a partner in Australia and New Zealand through Arval, but we are now a principal in both countries.

Lastly, we deepened the partnership with Arval. We extended that relationship to 10 years and expanded it to an exclusive basis. We are going to combine joint marketing and research dollars.

Obviously, with integration comes angst and extra work, but opportunity also arises. At the end of the integration, our customers will have a much better suite of tools to run their businesses. Any integration has bumps along the way. We'll minimize those and focus on our client's experience during that transition. But, what will come out of the integration will be an incredibly strong set of fleet-management tools our customers will love.

AF: Could you summarize the chronology leading up to this agreement?

Nullmeyer: In June 2013, we purchased GE's fleet business in Canada. We've also purchased a few other portfolios from GE — the helicopter portfolio and some aircraft portfolios. We know GE quite well; we know how they operate.

We had been talking to them for a period of time about the possible acquisition of its U.S. fleet company. Then, we stopped talking for a long period of time.

In the past year or so, we have been continuing our talks about putting the two companies together in some form. It really came to fruition April 10, 2015, when their CEO announced their pivot strategy. If you go back and look at that paper, they announced that morning that the real estate portfolio had been sold. The next one on the list, right below it in a big green box, was the $9-billion fleet portfolio. That's when we got into serious discussions with GE that morning, with respect to acquiring the fleet portfolio. Both companies intended that transaction to be done before June 30, 2015, and that's what came to fruition.

AF: There's a formal transitional services agreement that's in place with GE. Could you elaborate on what that agreement entails?

Nullmeyer: Our No. 1 objective is not to disrupt the client experience. We want our clients to have as seamless an integration experience as possible. Then, they will get these new analytical tools.

But, between here and there, we want to make sure everything is business as usual. The transitional service agreement with GE is very much that. It continues the billing and collecting; it continues payroll, benefits, and all the things you need to run the business smoothly, until we can transition to a combined platform.

AF: Some fleets have said the integration of portfolios in Canada was not as smooth as anticipated. What lessons were learned to ensure there will be a smoother integration with these two substantially larger companies?

Nullmeyer: I would be the first to admit the transition in Canada was not as smooth as we would have liked. This transition will be much smoother, because I now own both sides. I'm both the pitcher and the catcher on the receiving end of IT.

So, in previous transactions, you had Element in Canada requesting clients be transferred off a GE system onto an Element system. I had no control over what GE internal IT people were doing.

In this case, we now own the system those people are on, so we control all data mapping back and forth between the two. It's a much different integration because we now own it.

We will set up an office of integration completely outside of the leaders of our business. It will be a corporate function with input from our customers. We're going to have our customers on both sides of our business (GE and PHH) come to the table, and work with us on what type of systems and products they would like to see. With our transitional service agreement with GE, we have the time and ability to do that.

AF: What is the timeline for the integration of GE and PHH?

Nullmeyer: It's a staged transition. It will be between 12 and 18 months, depending on what type of systems you're looking at. The transition of the payroll systems and general-ledger systems will happen within months. If you're a GE customer on the GE system, you'll be able to stay on that system. There will be no change to what you do. As we bring in new products, either from the PHH or GE side, and offer either one of those front-end services, that will take a transition period. That could be as long as 12 to 18 months.

That's why the transitional services agreement goes that long, but we'll be very specific in making sure no customers have a negative experience during the transition.

The client advisory boards on both sides have already been engaged and talked to, and both sides are very anxious to participate because it makes their products and fleet operation much better.

AF: With the size of the larger company, is it conceivable there could be an interim dual presidency, or will there be a single president of the Element North American fleet business?

Nullmeyer: We are early in the process, but our goal is to do this integration quickly so that it is fair to the employees and so that our customers see the benefits as soon as possible. We expect to have one leader of the business and one face to the customers.

AF: Will the official corporate headquarters be where the new president resides?

Nullmeyer: Probably, but that's not necessarily where that person is today. We're a Canadian domicile company. Both groups have excellent campuses, excellent people working at them, and deep domain experience. We want to make sure we capitalize on that. Again, that will become clear over the next four to six weeks as we plan and start to put together what really is the best of both of those worlds.

We will decide where we think we can pull the best customer service and expertise. Then, the leader will be in whichever of those two becomes U.S. head office for fleet.

AF: Both Element and GE have made significant investments in new technologies. Is your ultimate goal to merge the two technology platforms to one?

Nullmeyer: Yes, the ultimate goal would be to merge to one. Both companies operate on an off-site mainframe. We're relatively indifferent to which one of those we need. GE outsources its mainframe to one company and we outsource ours to another. There will be only one big mainframe chugging away somewhere.

Both of us have spent a lot of money on the front-end development systems, GE more so than us. When PHH was owned by the mortgage company, PHH Corp., they didn't have as big a budget as GE. As a result, GE Fleet has spent a substantial amount of resources on technology, which we now own. We have products that are similar, but very complementary in nature.

Our technology group has been challenged with putting those two platforms together to make the customer's experience the easiest to use.

One system we're heading to will take the best of both worlds, and all the customer-forwarding applications, to create a very complementary data analytics reporting.

AF: How do you see the new, integrated entity differentiating itself in the marketplace?

Nullmeyer: The new entity will be the largest in the North American region. It will be the most forward and progressive company. It has a mindset, on both sides, to innovate, to change the fleet industry. When I travel to bank meetings or analyst meetings, I hear them refer to the fleet business as sleepy — growing only a few percent a year. We see the two companies together being innovators. We have the resources and the size to be able to do that.

Our innovation will be with our consulting practice, which is fantastic; how we jointly see the connected car; and, perhaps most importantly, our very large database of fleet data to do predictive analysis. That's very important when we're talking to clients about what their cost should be for a certain type of vehicle, in a certain region, with a certain type of usage pattern.

We can compare those based on our data, and run analytics, such as what kind of car or light truck they should purchase. We'll have a huge amount of data, and we'll have the willingness and vision to do predictive analytics. That is really going to change this industry over the next 12 to 18 months.

AF: You see technology being one of the growth opportunities. What about other areas? Element, in and of itself, has a pretty strong competence in heavy-duty trucks. When you merge PHH and GE together, it will create a very formidable presence in that segment. Are you looking to expand your truck business and truck portfolio?

Nullmeyer: Yes, absolutely. In addition to the technology I've talked about, we see various other avenues in which we can see growth, and, more importantly, offer services to our clients.

We like the Class 8 truck business, including the full maintenance segment of that business. That will certainly be a product we can add on.

When we're servicing a customer, such as a beverage company, and we're doing all of their light-duty repair trucks and their cars for their salespeople, we should be servicing their Class 8 trucks as well. And, it will be much more than what we have traditionally done, which is money-over-money leasing. It will be moving into the full-maintenance service products and full total cost of ownership for our clients.

AF: Do you foresee procurement opportunities to leverage additional discounts with the merger of these two large companies?

Nullmeyer: There will be procurement savings. We've already planned for it; we're going to be doing that shortly after the closing. So, if we're buying "x" number of tires from a manufacturer, I will be buying twice as many. Certainly, there will be savings there.

Our customers will share those savings. Also, being able to provide more services will allow us to leverage activities such as tow truck availability, when oil-change companies are open, or when we have a service site we want to open 24/7 so someone can get back on the road. We'll be able to demand better pricing for our clients, better service for our clients, and better response rates, mostly by the fact that we'll be buying twice as much as we were last week.

Secondly, we're going to leverage that into our Arval relationship. On a worldwide basis, we will buy even more again, so we're going to take advantage of it. Again, those savings will all be passed onto our customers, either in the form of better pricing or better service.

AF: Some critics say Element will grow to a size where it will be difficult to provide good customer service. How would you respond to that?

Nullmeyer: We'll have $12 or $13 billion in fleet assets. That's a nice-size company, but it's not that big. We will absolutely be able to provide good customer service. If you look at this company, everywhere will have customer service, customer service, customer service driven into it. What they will now have is the capacity from above with the capital and our strategic direction to be able to have those tools.

There's a long way to go before it's too big. The services we provide to customers are very menu driven and we will have the tools to provide the very best customer service.

Also, this is a very large part of our company — more than 70 percent of our assets and earnings will be from fleet. So, Element Financial Corp., as a parent company, is incredibly focused on fleet.

AF: It will take a tremendous amount of money to finance this acquisition. Some critics say it is a prelude to rates increasing.

Nullmeyer: No, the market drives rates. This market is driven off rates and then it's driven off services. You can price services for what the value is. I could never raise my prices because I paid to buy a company.

The customer will get better customer service on the funding side of the business, and they'll also get products that are bigger, faster, stronger and more of them that they can select. As for prices, anybody who suggests you can raise prices to pay for an acquisition against the market forces is delusional.

AF: How is Element looking to deepen its partnership with Arval?

Nullmeyer: PHH Arval has been around for a while. PHH, as a fleet company, was buried inside the mortgage company and did a fantastic job, but could only do so much. They were limited for resources by the mortgage company, and also by what they could do.

The relationship with Arval was strong, but wasn't as deep as we wanted it to be. We have deepened that relationship into actions such as joint marketing and procurement dollars.

Element Fleet, as a company, was very interested in the U.S., Mexico, Australia, and New Zealand. We didn't think we had the scale or mindset to be fantastic in Europe. That's when we got together with Arval and brought them into the transaction.

Arval, as part of this, will purchase the European parts of the GE fleet assets. Also, we've changed our relationship with Arval to be much stronger and deeper, to include more things like the procurement buying dollars and joint marketing dollars.

Ultimately, we're going to be servicing our clients better. We have software that's coming that sits on top of all these systems. If a customer really wants to know how their cars are doing in Australia, Brazil, the UK, Germany, or the U.S., they'll be able to do that through one software package. That's really what our global customers want.

With the stronger relationship with Arval, we'll be able to firm up deeper and better pricing for these clients on a global basis. If a client wants to do global pricing, which some of them do, we'll be able to do that. If they want to buy off a menu that's just the U.S., just Canada, just Australia, or just Europe, they can do that as well.

AF: Who will the new businesses in Australia and New Zealand report up to?

Nullmeyer: They will report directly to me. We are new to the Australian market as a principal. The Australian business has a very strong management team.

Because the Australian and New Zealand company is so far away from the U.S., GE ran it as a separate business reporting to the UK, so it was a very self-contained business unit. They're just about to launch a brand new, multi-million-dollar lease management computer system. It's fantastic. The system is about 95-percent complete and coming out soon. We will purchase the new lease management computer system as part of the acquisition.

The Australian and New Zealand business is a very forward-looking, progressive, innovative company with a great management team. They are thrilled with the services we'll be able to offer to their clients. We're really excited about the seasoned Australian management team.

What we'll provide for them is the strategic outlook, where we want them to go, and provide the capital. We'll give them all the tools they need to really excel in the Australian marketplace.

The Australian marketplace has four major suppliers. All of them are about the same size, depending what numbers you believe. They're all about the same size in vehicles. We believe with our capital, our equity, our strategic direction, and, most importantly, the management team there, we can be an absolute leader in Australia.

AF: Why was Japan the only GE Capital fleet business omitted from the sale?

Nullmeyer: They did not offer Japan for sale due to their corporate-tax accounting structure, and corporate structure in Japan. The very first day we met with GE, they said they were keeping Japan as a country. It was not offered for us to service.

AF: What keeps you up at night in terms of the fleet marketplace? Do you have any concerns?

Nullmeyer: Two things keep me up at night. Element Financial Corporation is an independent finance company. We're not owned by the banks or as big as GE. Our funding sources are very important to us. We have covered that by having a minimum of three-year committed financing from our banks, such as Bank of Montreal, which is our lead bank. We raised our senior line to $8.5 billion for funding. That's a three-year commitment.

We will have the funding, irrespective of what happens in the marketplace, irrespective of what happens in the commercial paper market, because we have our banking group behind us on a pre-committed basis. That's what I think about when I go to bed, but I sleep well knowing I have three-year banking commitments.

The only other thing that keeps me up is that the fleet industry is pretty stable. The concern is that we can slide back into thinking this is an old, sleepy business. To avoid this, we need to continually innovate by making sure everybody all through our ranks also continually innovates, and is excited about the fleet business.

Fleet is now moving into a technology-driven field. It's no less exciting than if you were in the banking market, providing core banking services for some of your bankers. That's what we're providing for our fleet clients. We're providing them the tools to manage a core, top-five spend. The worst thing we can do as a company and group of individuals is just rest on our laurels. We must have a relentless pursuit of excellence throughout our whole ranks.

I was pleased that PHH was able to keep that culture, even though they were part of the mortgage company. At GE, they have that culture. Our trick now will be to put those two companies together and keep that culture. I feel really good about that. Obviously, I know the team at PHH quite well. We got to know the GE team very well over the past year, as we worked with them, because they serviced us in Canada.

We feel really good about putting these two companies together.

More Blog Posts

Fleets Want Trust Restored with Suppliers

During this period of ongoing supply constraints, the trust that fleet managers had with OEMs, upfitters, and dealers has been strained. Fleet managers say they have had too many experiences over the past three years coping with erroneous information, adjusting to multiple price increases, and feeling betrayed by inadequate transparency from suppliers.

Read More →

Scheduled Replacement Cycles Are Becoming a Distant Memory

The ongoing difficulty in sourcing replacement vehicles is forcing companies to extend the service lives of vehicles that are unable to be replaced, which, inevitably, increases unscheduled maintenance expenses.

Read More →

Fleet Simplification is the Antidote to Asset Variability

Fleet simplification identifies asset functions to uncover commonality among the equipment and assets. Simplification increases operational efficiency as end-users become accustomed to the controls, displays, and operation of less diverse units.

Read More →

The Dangers of Static Fleet Policies

A fleet policy is a living document, flexible enough to adapt to evolving business priorities, developing industry trends, and changing industry best practices and standards.

Read More →

Short-Term vs. Long-Term Cost Reductions

Corporate procurement staff are often driven by short-term, immediate cost reductions. However, a longer perspective to soft cost savings is critical because fixating on short-term results will hurt a company in the long run.

Read More →

Uptick in Unscheduled Maintenance Increasing Vehicle Downtime

Fleet data analysis can identify recurring downtime issues. It’s important to determine the root causes of downtime so procedures can be developed to minimize such problems.

Read More →

Eliminate Needless Curb Weight to Maximize ICE & EV Efficiencies

Vehicle weight relates directly to fuel economy. In today’s era of electrification, there is also a direct correlation between vehicle weight and battery range.

Read More →

Tech Dependence Risks Dumbing Down Fleet Manager Expertise

The line between creative thinking and problem solving and doing what the data indicates is thin. To lead in fleet management, you need to balance understanding the fundamentals and embracing what smart technology offers.

Read More →

Leverage the Synergy of Safe Driving to Achieve Sustainability and Cost Goals

Safe driving, emission reductions, and cost containment can all be achieved at the same time.

Read More →

The Playbook for Fleet Manager Success

There are many paths to success — most of them involve being flexible, open-minded, and willing to learn.

Read More →