Trends in Commercial Fleet Management 2008-2010

The high cost of fuel is the No. 1 challenge facing fleets. Annual fuel cost increased, on average, $600 per vehicle from 2005-2007. In addition, other fuel-related commodities, such as replacement tires, have increased in cost.

The high cost of fuel is the No. 1 challenge facing fleet managers. Overall operating costs for commercial fleets increased 3 percent, on average, in calendar year 2007. The increase was directly attributable to higher fuel costs.

In 2007, the price of a gallon of regular unleaded gasoline increased almost 7 percent over record high prices in 2006. The annual fuel cost from 2005-2007 increased $600 per vehicle on an annual basis, based on driving 2,000 miles per month.

Fleets with a heavy concentration of diesel trucks were hardest hit since diesel costs increased more than gasoline. In 2007, use of ultra low sulfur diesel (ULSD), which costs more per gallon than regular diesel, was federally mandated.

The high cost of fuel has caused a domino effect with other fleet costs. For example, there have been multiple price increases for replacement tires due to the high cost of oil. Another example is towing and road service fees. Many tow providers and mobile glass repair services have not only increased fees, but have also added fuel surcharges. High fuel costs have also caused the cost of mobile fueling services to increase, impacting centrally garaged fleets.

Fleets have been experiencing fuel price volatility since 2002 and continue to in 2008. One reason for the ongoing fuel price volatility is the weakness in the nation’s fueling infrastructure. For instance, no new refineries have been built in the U.S. since the Garyville refinery in Louisiana went online in 1976, despite year-over-year increases in gasoline demand. This has resulted in limited refining capacity, especially for the production of reformulated gasoline, which increases the frequency of spot shortages.

Another key factor for higher fuel prices is increasing fuel demand from emerging markets such as China and India.

In January 2008, the Energy Information Administration (EIA) forecast said retail prices for petroleum products are expected to increase in 2008, pushed up by the higher average crude oil prices. Gasoline prices at year-end 2007 were 60 cents per gallon higher than year-end 2006.

Many fuel market analysts are forecasting that the national average could reach as high as $3.75 per gallon. That would be more than 50 cents per gallon higher than the record price set May 2007. Diesel prices have already reached that high. As of March, diesel prices, for the first time ever, exceeded $4 per gallon in several markets.

The contrarian viewpoint by some analysts is that prices could eventually see a large collapse. Year-on-year demand as reported by the Department of Energy is showing a decline. In the background is the wild card factor of ongoing geopolitical uncertainty in oil-producing regions of the world.

Fleet managers developing 2009 model-year selectors are under pressure to shift to more fuel-efficient vehicles. The goal is to increase overall fleet mpg. For instance, more fleets are re-evaluating use of SUVs or moving to smaller SUVs.

Fleets are also taking a multipronged approach to managing fuel spend. This includes spec’ing four-cylinder, instead of six-cylinder, engines. But, at some fleets, these considerations are encountering driver (and management) resistance.

Another approach, especially for truck fleets, is implementing anti-idling programs.

A growing number of fleets are conducting pilot programs to test hybrid vehicles. Several fleets, such as Secura and Toshiba Medical, have made the corporate decision to go to an all-hybrid fleet.

Another aspect of this multipronged approach is the adoption of telematic devices and GPS. Fleet managers are reinvigorating control of fuel costs at the driver level by setting tighter and more frequent exception reporting. They are implementing driver education awareness programs to encourage drivers to maintain proper tire pressure, drive less aggressively, and minimize idling.

One way to offset the higher cost of fuel is to increase personal use charges to recoup fuel costs.

Other fleets are tightening fleet vehicle eligibility requirements to minimize the number of vehicles in the corporate fleet.

[PAGEBREAK]

Over the past several years, safety has re-emerged as a hot issue for many fleet managers. Concern has increased about vehicle and driver safety and minimizing liability exposure.

Although the cost of fuel is cited as the number one fleet challenge, fleet safety is a close second. With some fleets, it is the primary challenge. One reason for the heightened interest in fleet safety is management pressure to minimize corporate liability exposure.

In addition, more cars are totaled today due to the high cost to repair vehicles.

A third reason for the increased interest in fleet safety is that driver distraction is causing an uptick in preventable accidents. The key reason for the uptick is that drivers are being asked to do more in the same allotted time, causing them to multitask behind the wheel.

In an effort to minimize driver distraction, fleets are tightening cell phone usage policies, and/or eliminating texting and electronic devices in company vehicles to keep employees focused on driving.

Safety concerns are exerting even greater influence on selector decisions. There is more involvement by risk management in influencing vehicle selection. For instance, some fleets are putting increased emphasis on National Highway Traffic Safety Administration (NHTSA) crash test ratings. Only vehicles with high safety ratings are allowed on some fleet selectors. Compounding this is some fleet managers’ reluctance to acquire vehicles not advised by the risk department out of concern if something should happen, it not be blamed on their recommendation.

For the first three quarters of 2007, inventory of used fleet vehicles was in balance with buyer demand in the wholesale market. Prices were stable and buyer demand was good.

However, fourth quarter 2007 saw wholesale market prices decline, on average, 8 percent compared to same time last year. And this softness has extended into first quarter 2008. Normal seasonal decline was part of the reason for the market slowdown. Also contributing to this decline was the tightening of credit for subprime buyers.

Most buyers of used fleet vehicles are subprime buyers, who are now finding it increasingly difficult to get funding. Also, home equity loans have dried up, eliminating a source of vehicle funding.

In addition, the housing and construction slowdown has decreased demand for work trucks and full-size vans.

Vehicles continue to sell at auction; however, they tend to be priced to current market demand.

Art Spinella of CNW Marketing predicts a soft resale market for used-vehicle sales due to increased inventory of retail off-lease vehicles. This volume will increase from 2008-2009.

In addition, the 2005 model-year was a higher than normal year for commercial fleet purchases, and these vehicles are entering the wholesale market in 2008.

A softening in retail demand for used vehicles is predicted because many potential retail buyers are “upside down” in their vehicles. Also, consumers are holding onto vehicles longer as quality has increased.

Resale values for intermediate sedans were stable for the first three quarters of 2007. However, since the fourth quarter 2007 and first quarter 2008, resale values for intermediate sedans were down compared to sales same time last year.

Resale prices for compact models continue to be strong, but most fleets do not include many of these vehicles. Compact cars with higher fuel economy are not as hard hit by higher fuel prices.

Resale values for passenger minivans continue to remain in the doldrums due to changing consumer preference to crossover-type vehicles. Minivan prices have been soft for the past six years, indicating a broader consumer preference change. Despite decreases in the number of minivan models, prices continue to remain soft. The minivan market must be viewed as two segments — extended wheelbase and short wheelbase models. Resales for extended wheelbase, seven-passenger models are doing better than short wheelbase models.

The cargo van market for most of 2007 was stable. Cargo vans continued to sell quickly, especially when equipped with a V-8 and painted white. However, slowdown in construction and housing markets decreased wholesale demand for cargo vans in the fourth quarter 2007 and first quarter 2008.

Resale values for cargo vans and work trucks remain uncertain because of soft demand from seasonal labor companies such as contractors and landscapers.

Pickup trucks have been perennially strong sellers in the wholesale market reflecting strong demand in the retail market. However, resale values are softening. Pickup truck sales were stable for most of 2007. However, prices have softened with the slowdown in the contractor market.

The pickup truck market is segmented into two categories: work trucks and trucks used to haul passengers, such as the better-equipped extended-cab models.

Resale for large SUVs continues soft as high gas prices impact resale prices.

SUV resale values for compact models are stronger than large SUVs. SUVs need to be well-equipped and appropriate to the region (i.e. no 2WD models in the Snow Belt, but okay for Texas and Florida).

[PAGEBREAK]

The high cost of fuel is beginning to influence new-vehicle acquisition decisions such as type and size of model acquired.

Lifecycle cost analyses are influenced by higher residuals for more fuel-efficient vehicles and lower cap costs for smaller vehicles.

Another factor that will influence future fleet purchases is that companies are adopting minimum mpg requirements in order to place vehicles on the corporate selector.

Fleet managers are engaging in a balancing act in providing high fuel economy vehicles, while still keeping drivers happy.

The factors influencing 2009 model-year selector decisions are:

Fuel efficiency considerations will be a greater issue in selector decisions. Many fleets are adopting minimum mpg requirements before vehicles are added to the selector.

Companies are looking to “right-size” cargo-carrying vehicles and large SUVs in reaction to higher fuel prices.

Companies are searching for van replacement vehicles as more OEMs exit this market segment.

Amount of CPA monies available from OEMs will influence volume and make of models acquired.

Corporate “green” initiatives are prompting placement of hybrids on selectors at more companies.

Push to reduce fleet carbon footprint is a real and growing corporate trend, especially among multinational companies.

Driver dissatisfaction is also an emerging issue. Demand is growing from drivers and department or division management for greater vehicle selection on the company selector. This is especially true with fleets that have sole-sourced for a number of years.

Another emerging issue is driver demands for more “green” vehicles. However, the bottom-line consideration always trumps driver dissatisfaction. Another expression of dissatisfaction is increased demand for exceptions to selector policy. More employees are asking for larger vehicles, citing a medical condition or physical stature.

Strategic sourcing continues to solidify its inroads into fleet procurement. There has been a long-standing trend for purchasing decisions to move away from the fleet manager to purchasing/procurement groups. Strategic sourcing of fleet services and vehicles will continue to grow in influence at Fortune 500 companies.

More and more fleet managers are finding themselves reporting to corporate procurement departments. As a consequence, some fleet managers now have diminished input in RFP development and supplier selection decisions.

Another factor influencing corporate procurement is pressure to extend fleet vehicle service life. There has been a trend to longer vehicle service life. However, length of service in 2007 was static compared to 2006. Improved vehicle quality allows extended replacement cycling. A caution: Almost 35 percent of a vehicle’s lifetime operating costs occurs in the 68,000 to 80,000 mile range.

The trend to longer service life has been particularly true with trucks. On average, medium-duty trucks are kept in service 70 to 80 months and approximately 160,000 miles. One positive aspect is that trucks have the lowest depreciation cost per month because fleets keep them in service longer than other vehicle types. Another factor favoring longer lifecycles is that medium-duty truck quality is at an all-time high.

The upcoming 2010 diesel emission standards will impact truck procurement. For instance, the cost of the new 2010 engine is predicted to increase by approximately $4,000. Many industry observers anticipate a pre-buy of 2009 models to avoid first-year 2010 engines. Or fleets will extend cycling parameters to avoid first-year 2010 engines. Another concern is that the urea injection system will take up additional space on a truck’s frame and constrict some upfits.

Many multinational corporations have adopted strategies to reduce greenhouse gas (GHG) emissions. Fleets are establishing emission baselines and developing selectors to achieve these goals. Examples are USG, PPG, Novo Nordisk, and Ecolab.

According to a PHH Arval survey, 40 percent of fleet managers said corporate interest in “green” initiatives has grown significantly. This concern extends to senior management. In 2007, 77 percent of fleet managers reported being asked by senior management about the environmental impact of fleet.

However, this overall corporate goal often contradicts with mandates to reduce fleet operating costs. Being a good corporate citizen sometimes overrules cost considerations.

Another initiative is to right-size fleet. Weyerhauser is shifting drivers away from SUVs to AWD Taurus and Fusion sedans.

Abbott became the first Fortune 500 company to commit to creating a “carbon neutral” fleet. Abbott discovered 12 percent of its corporate-wide GHG emissions were generated by its 6,500-vehicle fleet. The company has designed a fleet selector to decrease its carbon footprint. The 2009 selector will include hybrids and high-fuel economy vehicles. However, Abbott says its selector will be realistic to ensure that vehicle choices continue to satisfy its sales force. Xerox is another fleet focused on GHG reduction.

As part of these corporate green fleet initiatives, there has been a growth of hybrids in commercial fleets. Many companies want to portray an environmentally friendly corporate image. A number are running pilot programs using hybrids. From a lifecycle perspective, it is difficult to get hybrids to “pencil out.” Despite this, several fleets have made the corporate decision to go to all-hybrid. These include Toshiba Medical and Secura Insurance. Other fleets acquiring substantial volumes of hybrids include State Farm, Pepsico, DuPont, Cooper Tire & Rubber, and Cephalon.

However, the technician shortage will present a challenge in maintaining hybrid vehicles. Drivers will be required to return hybrids to a dealership for service until independent repair facilities become trained to properly service these vehicles. Quick turnaround servicing at dealerships of hybrids will be critical to their success in the fleet market. Hybrid components require specialized training such as the regenerative braking system to supply voltage, dual use transmission, electric motor, battery pack, etc.

However, PM requirements for hybrids are similar to those of traditionally powered vehicles.

Telematics is moving downstream to smaller GVW trucks and cars.

Since the late 1980s, telemetrics has been used by the over-the-road truck industry for delivery scheduling, route optimization, and driver communication. The widespread use of satellite tracking and communication technology in the Class 8 market is migrating to the Class 3 to 7 market. One factor driving this trend is the ability to provide real-time mileage reporting. Mileage reporting is a major challenge for fleet managers, so this feature is attractive.

Many observers predict the use of onboard technology will become the future norm in the fleet industry. They envision data from the engine automatically transmitted, providing real-time information on engine status, along with GPS positioning and other info such as vehicle idle time and speed.

Onboard sensors are already used to ensure emission compliance. In California, remote diagnostics can ensure drivers no longer need to have vehicles tested for emissions.

Major fleet management companies offer telematic services for commercial fleets. Early telematics adopters are ServiceMaster, GEICO, Ryder, Kindercare, Wal-Mart, UPS, Cox Enterprises, Truly Nolan, and long-haul trucking companies.

Currently there are 2.5 million telemetric units in service, managing vehicles, trailers, mobile workers, and other assets. C.J. Driscoll and Associates predicts the market will expand to 5.8 million units by 2009.

Companies can see a 2-10 times ROI on fleet telematics. (See the February 2008 issue of Automotive Fleet for real-world ROI on telematic investments by fleets.)

Telematic devices help control fuel expenditures by identifying excessive idling, under- and over-utilized vehicles, unauthorized vehicle usage, and route optimization. ValleyCrest Companies reports a 10-percent decrease in fuel spend following the implementation of a fleet GPS system.

Car maintenance expenses were flat for 2007 as a result of improved manufacturer quality. Also, more automotive components require less or no servicing. Under-the-hood components require less frequent servicing, such as coolants, spark plugs, transmissions, etc.

In fact, maintenance costs actually decreased, but savings were offset by higher labor rates and parts prices. There has been ongoing market pressure for increased labor rates in high cost-of-living areas. Cost of replacement parts has increased as the cost to transport them to market increases with the high cost of fuel.

Lower maintenance incidents have offset rising labor rates. In addition, extended powertrain warranties introduced by the Detroit 3 will put further downward pressure on maintenance costs. The majority of expenses — approximately 68 percent — continue to be in PM and wear item replacement (such as tires, brakes, etc.)

However, increased technology such as TPMS (tire pressure monitoring system), onboard navigation system, etc., will increase costs. Although fairly reliable, when failures occur, these systems are expensive to repair.

There is also a trend to extend PM intervals. Over the past five years, maintenance intervals have increased. For example, vehicle manufacturers have extended recommended service intervals using long-life spark plugs, transmission fluids, and coolant.

More fleets are extending oil change intervals as a cost-cutting measure, and more are relying on vehicle onboard oil monitoring systems to determine oil change intervals.

The cost of replacement tire expenses is creeping upward. Tire costs increased in 2006 and 2007 due to the higher cost of crude oil. In 2007, there was a 2- to 4-percent price increase for car replacement tires, representing a $3-$4 increase per tire.

Tire price hikes are continuing in 2008. All tire manufacturers have announced 2008 price increases of 4-6 percent.

In addition, the trend away from 16-inch tires to larger 17- and 18-inch wheel sizes is causing replacement tire costs to increase.

The 2007 diesel emission standards have contributed to higher truck operating expenses. The primary reason was the increased cost of 2007-compliant diesel engines and special motor oil requirement. For example, CJ-4 oil required for 2007 engines is 10-percent more expensive than regular oil.

The cost of fuel, in particular diesel, has impacted truck fleets. As a result, fleets are looking at more aerodynamic trucks and modifying specs to increase mpg.

Some fleets are installing telematic systems to monitor fuel usage and are employing geofencing products. Another tactic is that fleets are ordering trucks with idle cutoffs after 5-15 minutes.

However, the anticipated 3-percent decrease in fuel economy from 2007 diesel engines did not occur. But ultra low sulfur diesel does costs about 6 cents per gallon more than regular diesel.

Cost of replacement tires has also increased, but use of recaps has helped mitigate expense.

Emission standards increased the cost of diesel engines. Engines are more complex, which has caused concern about long-term reliability and longevity.

Not only have the new emission standards increased initial acquisition cost, they also increased maintenance requirements. Additional technician training is required to service these engines.

More fleets are seeking to lower acquisition costs by selecting lower GVW trucks. Fleets are spec’ing trucks with a lower than 26,000-lb. GVW to avoid having to hire drivers with a CDL. Due to the driver shortage, the number of CDL drivers is limited, and those with CDLs command higher salaries.

More Green Fleet

Turning Connected Vehicle Data Into Decisions That Matter

Fleet leaders have more data than ever, but turning that data into clear, actionable decisions remains a challenge. This white paper shows how leading organizations are using connected vehicle data to improve safety, reduce costs, and optimize fleet performance. Learn how to turn insight into action across your fleet.

Read More →Are You Tracking Your Fleet's True Total Cost of Ownership?

Bobit Business Media surveyed 190 fleet professionals and found that while most fleets are tracking costs, fragmented systems and data gaps are keeping true TCO visibility out of reach. With rising pressure to control spend in an increasingly volatile environment, the gap between what fleets think they know and what the data actually shows is wider than you might expect. See how your peers are managing costs today and where the industry still has room to improve.

Read More →

Hybrids: Electrification Without the Challenges

For fleet managers, fuel is one of the biggest line items in the budget — and it's one hybrids can shrink without changing how your people work. Download the eBook to see the numbers, understand the technology, and get a step-by-step guide to making the switch.

Read More →

Startup ZMD Motors Developing Electric Conversion for Ram 5500 Work Trucks

Detroit-based company says it has begun early development of a system to convert internal combustion Ram 5500 chassis-cab trucks to electric power.

Read More →

U.S. EV Adoption Is Climbing, but Commercial and Passenger Markets Diverge

New industry group data revealed that light-duty electric vehicle sales are hitting record market share and volumes, while commercial EV volume dipped. What’s driving the fluctuations?

Read More →

How To Upfit Electric Work Trucks and Vans

The biggest challenge lies in balancing additional equipment and accessories with EV battery capacity and range.

Read More →

How Fleets Can Adjust Approaches To EV Adoption

With the expiration of federal incentives, EV success now hinges less on government policy and more on discounts, battery tech progress, increased range, and broader infrastructure.

Read More →

Despite World Troubles, Forward Thinking Guides Fleets

Fleet operators shared their challenges during an annual conference that embraced the latest advances across all aspects of running private- and public-sector vehicles.

Read More →

GM Energy Details Partnerships and Targets for Public Charging Build-Out

EVgo, Pilot, ChargePoint and IONNA named; goal is 35k GM-invested DC stalls by 2030, with customer-experience upgrades at sites.

Read More →

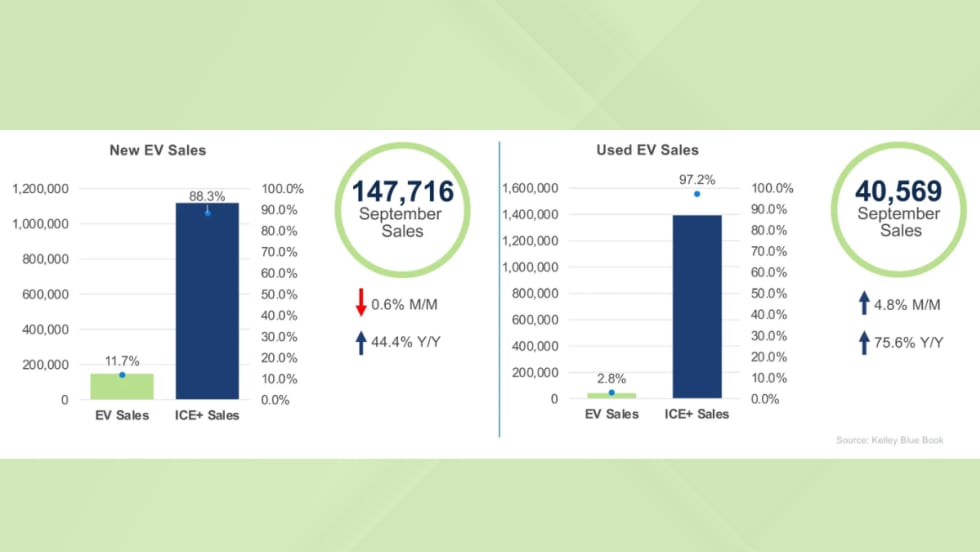

Q3 Electric Vehicles Sales Hit Record High

EV buyers took advantage of the final federal tax credit days, while average prices edged up for new EVs and continued to decline for used models.

Read More →